Yogurt - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Yogurt Market is Segmented by Product Type (Flavored Yogurt, Unflavored Yogurt), by Distribution Channel (Off-Trade, On-Trade) and by Region (Africa, Asia-Pacific, Europe, Middle East, North America, South America). Market Value in USD and Volume are Both Presented. Key Data Points Observed Include Per Capita Consumption; Population; and Dairy Production.

ヨーグルト市場は、製品タイプ(フレーバーヨーグルト、無香料ヨーグルト)、流通チャネル(オフトレード、オントレード)、地域(アフリカ、アジア太平洋、ヨーロッパ、中東、北米、南米)別にセグメント化されています。米ドル建ての市場価値と数量の両方が提示されています。主要なデータポイントには、一人当たり消費量、人口、乳製品生産量が含まれます。

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 365 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14091 |

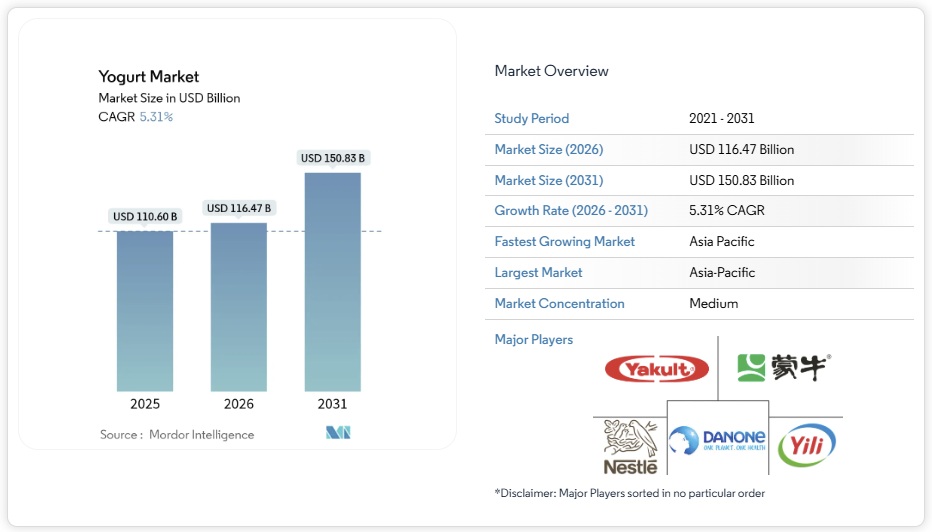

ヨーグルト市場規模は2026年には1,164.7億米ドルと推定され、2025年の1,106億米ドルから拡大し、2031年には1,508.3億米ドルに達すると予測されています。これは、2026年から2031年にかけて年平均成長率(CAGR)5.31%で成長する見込みです。ヨーグルト市場は、臨床的に検証されたプロバイオティクス株と測定可能な腸内環境の改善効果との関連性が実証されていることから、プレミアム化を促進し、カテゴリーの堅調な回復力を高めています。メーカーは、消化を通じて善玉菌を生存させる高度な発酵技術を採用しており、機能性食品としての位置付けを支え、消費者のアップグレード意欲を維持しています。新興国における可処分所得の堅調な伸びと免疫サポートへの関心の高まりが需要をさらに押し上げる一方で、デジタルコマースは商品の発見とサブスクリプションベースの補充を加速させています。特にカフェやコンビニエンスストアなどにおける食品サービスへの浸透の拡大により、利用機会が広がり、常温保存可能な包装における技術革新により、コールドチェーンインフラが整っていない市場へのリーチが拡大しています。

セグメント分析

- 2025年には、スプーンで食べるヨーグルトは、消費者の強い嗜好と、朝食、間食、デザートなど、様々な消費シーンに対応する汎用性に支えられ、67.42%という圧倒的な市場シェアを獲得する見込みです。この成功の大きな要因は、分量をコントロールできるという利点と、材料やトッピング、そして幅広いフレーバーでカスタマイズできるという点です。これらの要素は、製品の官能的な魅力と知覚価値の両方を高めています。一方、飲むヨーグルトは市場で最も高い成長率を記録しており、2031年までの年平均成長率(CAGR)は6.86%と予測されています。この成長は、現代の消費者の目まぐるしいライフスタイルに合致する、便利で持ち運びやすい栄養ソリューションへの需要の高まりが主な要因です。

- 革新的な包装技術は、プロバイオティクスの生存率を確保しながら保存期間を延長し、より広範な流通網の実現を可能にすることで、飲むヨーグルトの成長に重要な役割を果たしてきました。カフェやコンビニエンスストアが液体タイプを好む傾向が強まるにつれ、飲むヨーグルト市場は外食チャネルの拡大からも大きな恩恵を受けています。これらのタイプは既存の飲料事業に容易に統合でき、準備も最小限で済むため、企業にとって魅力的な選択肢となっています。さらに、FDAはスプーンで飲むタイプと飲むタイプの両方のヨーグルトの健康強調表示を支持していますが、飲むタイプは、特に糖分含有量と栄養成分表示に関して、より厳しい審査を受けています。こうした規制の厳格化は製品の配合戦略に影響を与え、メーカーは革新を促し、消費者と規制当局の変化する期待に応えようとしています。

- 2025年には、乳製品ベースのセグメントが、伝統的な製造技術と強固なサプライチェーンを背景に、53.95%という大きな市場シェアを獲得するでしょう。これらの強みにより、世界市場において一貫した品質と競争力のある価格が確保されます。消費者は乳製品とその天然の完全タンパク質に親しみ、健康志向を高め、栄養価の訴求力を高めています。一方、植物由来の代替品は目覚ましい成長を遂げており、2031年までの年平均成長率(CAGR)は7.78%と予測されています。この成長は、乳糖不耐症への意識の高まり、環境持続可能性への懸念の高まり、そして食生活の嗜好の変化に起因しており、これらが相まって、米国国立生物工学情報センター(NCBI)が指摘するように、対象市場全体の拡大につながっています。

- 植物性タンパク質の分離・発酵技術の進歩により、非乳製品ヨーグルトは従来の乳製品の食感と風味を再現しつつ、同様のプロバイオティクス効果を提供することが可能になりました。アーモンド、オート麦、ココナッツをベースにしたヨーグルトは、それぞれ異なる栄養プロファイルと風味特性を備え、多様な消費者層や利用シーンに訴求力を発揮します。しかしながら、植物由来ヨーグルトは、特にタンパク質含有量の表示やプロバイオティクス菌株の生存率に関して、規制上の課題に直面しています。これらの課題に対処するには、特殊な製造工程と厳格な品質管理が必要であり、小規模生産者にとって大きな参入障壁となっています。

- ヨーグルト市場は、製品タイプ(フレーバーヨーグルト、無香料ヨーグルト)、流通チャネル(オフトレード、オントレード)、地域(アフリカ、アジア太平洋、ヨーロッパ、中東、北米、南米)別にセグメント化されています。米ドル建ての市場価値と数量の両方が提示されています。主要なデータポイントには、一人当たり消費量、人口、乳製品生産量が含まれます。

Yogurt Market Analysis

Yogurt market size in 2026 is estimated at USD 116.47 billion, growing from 2025 value of USD 110.60 billion with 2031 projections showing USD 150.83 billion, growing at 5.31% CAGR over 2026-2031. The yogurt market continues to benefit from a proven link between clinically validated probiotic strains and measurable gut-health outcomes, encouraging premiumization and fostering steady category resilience. Manufacturers have adopted advanced fermentation technologies that keep beneficial bacteria alive through digestion, supporting functional-food positioning and sustaining consumer willingness to trade up. Strong disposable-income growth across emerging economies and rising interest in immune support further reinforce demand, while digital commerce accelerates product discovery and subscription-based replenishment. Expanding foodservice penetration—especially in cafés and convenience stores—broadens usage occasions, and technological breakthroughs in shelf-stable packaging extend reach into markets lacking cold-chain infrastructure.

Global Yogurt Market Trends and Insights

Growing Consumer Focus on Gut Health, Probiotics, and Immunity

Probiotic strains are redefining yogurt’s role from a simple indulgence to a therapeutic nutrition option. Clinical studies have confirmed the effectiveness of specific bacterial cultures, such as Lactobacillus acidophilus and Bifidobacterium lactis, in enhancing immune function and digestive health. Research indicates that these strains can reduce the duration of respiratory infections by up to two days and strengthen gut barrier function, as reported by the National Center for Biotechnology Information. With this scientific backing, manufacturers can justify premium pricing for probiotic-enriched products while building consumer trust through proven health benefits. As global healthcare expenses rise, functional yogurt is gaining traction as a preventive nutrition that offers tangible wellness outcomes. Additionally, regulatory bodies are increasingly approving health claims for specific probiotic strains, providing a competitive advantage to companies that prioritize clinical research and strain innovation.

Development of Functional and Fortified Yogurts with Added Nutrients

Yogurt is being redefined as a wellness product, with manufacturers adding protein isolates, omega-3 fatty acids, vitamins, and minerals to address specific nutritional deficiencies in consumer diets. Advanced microencapsulation technologies now protect sensitive nutrients during fermentation and storage, ensuring the stable delivery of heat-sensitive compounds like probiotics and vitamins, as acknowledged by the Food and Drug Administration. Leveraging these advancements, single-serve yogurt products now provide 20-25 grams of protein along with a complete vitamin profile, directly competing with traditional supplements. This strategy is particularly effective in regions with identified nutritional deficiencies, positioning fortified yogurt as an accessible source of essential nutrients. Regulatory approval processes for fortification claims create entry barriers that benefit established manufacturers with expertise in regulatory compliance and clinical validation.

Volatile Prices and Irregular Supply of Milk

Milk price volatility compresses margins and disrupts supply chains, compelling manufacturers to implement dynamic pricing strategies while addressing consumer price sensitivity in competitive retail markets. USDA forecasts indicate that milk prices will remain between USD 22-24 per hundredweight through 2025, reflecting 15-20% volatility that directly affects yogurt production costs. Weather-related supply disruptions, increasing feed costs, and dairy herd consolidation result in inconsistent milk availability, complicating production planning and inventory management. Smaller yogurt producers face greater challenges due to limited bargaining power with dairy suppliers and reduced capacity to mitigate commodity price risks through financial instruments. Additionally, the geographic concentration of dairy production in specific regions increases susceptibility to localized supply disruptions, impacting global yogurt manufacturing networks.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use in Cafes, QSRs, and Convenience Outlets

- Rising E-commerce Expansion

- Rising Prices of Raw Materials and Energy Increase Production

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, spoonable yogurt holds a commanding 67.42% market share, supported by strong consumer preferences and its versatility across various consumption occasions, including breakfast, snacking, and dessert. Its success is largely driven by the benefits of portion control and the ability to customize with mix-ins, toppings, and a wide range of flavors, which enhance both the sensory appeal and the perceived value of the product. On the other hand, drinkable yogurt is experiencing the fastest growth in the market, with a projected CAGR of 6.86% through 2031. This growth is primarily attributed to the increasing demand for convenient, on-the-go nutrition solutions that align with the fast-paced lifestyles of modern consumers.

Innovative packaging technologies have played a crucial role in the growth of drinkable yogurt by ensuring the viability of probiotics while extending shelf life, which facilitates broader distribution networks. The drinkable yogurt segment is also benefiting significantly from the expansion of foodservice channels, as cafes and convenience stores increasingly prefer liquid formats. These formats integrate effortlessly into existing beverage operations and require minimal preparation, making them an attractive option for businesses. Additionally, while the FDA supports health claims for both spoonable and drinkable yogurt formats, drinkable varieties face stricter scrutiny, particularly regarding sugar content and nutritional labeling. This regulatory focus is influencing product formulation strategies, pushing manufacturers to innovate and meet evolving consumer and regulatory expectations.

In 2025, the dairy-based segment holds a significant 53.95% market share, driven by its traditional manufacturing expertise and robust supply chains. These strengths ensure consistent quality and competitive pricing in global markets. Consumers’ familiarity with dairy products, along with their natural complete proteins, enhances health positioning and supports nutritional claims. On the other hand, plant-based alternatives are experiencing remarkable growth, with a projected CAGR of 7.78% through 2031. This growth is attributed to increasing awareness of lactose intolerance, heightened environmental sustainability concerns, and evolving dietary preferences, which collectively expand the total addressable market, as highlighted by the National Center for Biotechnology Information.

Advancements in plant protein isolation and fermentation technology have enabled non-dairy yogurts to replicate the texture and taste of traditional dairy products while offering similar probiotic benefits. Almond, oat, and coconut bases provide distinct nutritional profiles and flavor characteristics, appealing to diverse consumer segments and usage occasions. However, the plant-based segment faces regulatory challenges, particularly regarding protein content claims and probiotic strain viability. These issues require specialized manufacturing processes and rigorous quality control, posing significant entry barriers for smaller producers.

The Yogurt Market is Segmented by Product Type (Flavored Yogurt, Unflavored Yogurt), by Distribution Channel (Off-Trade, On-Trade) and by Region (Africa, Asia-Pacific, Europe, Middle East, North America, South America). Market Value in USD and Volume are Both Presented. Key Data Points Observed Include Per Capita Consumption; Population; and Dairy Production.

Geography Analysis

In 2025, Asia Pacific holds a dominant 55.78% market share and exhibits a leading growth rate of 11.9% projected through 2031. This growth stems from the region’s mix of traditional fermented food practices and the rapid adoption of Western-style yogurt across varying economic stages. Urbanization in China and India is driving higher disposable incomes and greater health awareness, fueling regional expansion. Meanwhile, established markets like Japan and South Korea focus on premium probiotic innovations and functional nutrition. The region’s dairy production capabilities, along with the rise of plant-based alternatives, address diverse dietary needs and the widespread prevalence of lactose intolerance. However, regulatory frameworks in Asia Pacific vary widely: some countries enforce strict probiotic strain requirements, while others adopt more flexible health claim standards, influencing product development strategies.

Europe, though a mature market, remains strategically important in the yogurt industry. Consumers in the region favor organic, premium, and artisanal yogurt products, which often command higher prices and drive innovation within the category. Europe’s well-established dairy infrastructure and rigorous food safety regulations provide local producers with competitive advantages while setting global quality benchmarks. Countries such as Germany, France, and the Netherlands lead in per capita consumption and maintain strong export capabilities. Additionally, European consumers increasingly prioritize sustainable packaging and environmentally friendly production methods, shaping supply chain decisions and brand strategies.

North America maintains a significant market presence, leading in innovations related to functional nutrition, high-protein options, and convenient packaging formats that cater to the region’s on-the-go consumption habits. The U.S. and Canada benefit from advanced retail and e-commerce infrastructures, enabling rapid product launches and consumer education efforts that support premium brand positioning. Regulatory support for health claims and probiotic benefits fosters the development of functional yogurt products. Established relationships with foodservice channels further drive demand, particularly in restaurants and convenience stores. The region’s focus on protein and fitness culture strongly supports the popularity of Greek and Icelandic yogurts, known for their enhanced nutritional profiles.

List of Companies Covered in this Report:

- China Mengniu Dairy Co Ltd

- Inner Mongolia Yili Industrial Group Co Ltd

- Nestlé SA

- Yakult Honsha Co Ltd

- General Mills Inc. (Yoplait)

- Chobani Global Holdings LLC

- Lactalis Group

- Fonterra Co-operative Group Ltd

- Arla Foods am-ba

- Saputo Inc.

- Gujarat Co-operative Milk Marketing Federation (Amul)

- Meiji Holdings Co Ltd

- Bright Dairy & Food Co Ltd

- Grupo Lala S.A.B. de C.V.

- Ultima Foods Inc.

- Valio Oy

- Lifeway Foods Inc.

- Morinaga Milk Industry Co Ltd

- The Hain Celestial Group Inc.

- Yoso Brands

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Growing consumer focus on gut health, probiotics, and immunity

4.2.2 Development of functional and fortified yogurts with added nutrients

4.2.3 Rising use in cafes, QSRs, and convenience outlets

4.2.4 Rising E-commerce expansion

4.2.5 Advanced fermentation techniques and shelf-stable packaging innovations

4.2.6 High-protein Greek & Icelandic lines broaden usage occasions

4.3 Market Restraints

4.3.1 Volatile prices and irregular supply of milk,

4.3.2 Compliance with regional food safety, labeling, and health claim regulations

4.3.3 Rising prices of raw materials and energy increase production

4.3.4 Competition from non-dairy alternatives like almond or oat milks

4.4 Regulatory Outlook

4.5 Porter’s Five Forces

4.5.1 Threat of New Entrants

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Bargaining Power of Suppliers

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

5.1 Type

5.1.1 Drinkable Yogurt

5.1.2 Spoonable Yogurt

5.2 Source

5.2.1 Dairy-based

5.2.2 Non-dairy based

5.3 Flavour

5.3.1 Flavoured

5.3.2 Un-flavoured

5.4 Distribution Channel

5.4.1 On-trade

5.4.2 Off-trade

5.4.2.1 Convenience Stores

5.4.2.2 Specialist Retailers

5.4.2.3 Supermarkets and Hypermarkets

5.4.2.4 On-line Retail

5.4.2.5 Others (Warehouse clubs, gas stations, etc.)

5.5 Geography

5.5.1 North America

5.5.1.1 United States

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.1.4 Rest of North America

5.5.2 Europe

5.5.2.1 Belgium

5.5.2.2 France

5.5.2.3 Germany

5.5.2.4 Italy

5.5.2.5 Netherlands

5.5.2.6 Russia

5.5.2.7 Spain

5.5.2.8 Turkey

5.5.2.9 United Kingdom

5.5.2.10 Rest of Europe

5.5.3 Asia Pacific

5.5.3.1 China

5.5.3.2 India

5.5.3.3 Japan

5.5.3.4 Australia

5.5.3.5 Indonesia

5.5.3.6 Thailand

5.5.3.7 Malaysia

5.5.3.8 South Korea

5.5.3.9 Rest of Asia Pacific

5.5.4 South America

5.5.4.1 Brazil

5.5.4.2 Argentina

5.5.4.3 Chile

5.5.4.4 Peru

5.5.4.5 Rest of South America

5.5.5 Middle East and Africa

5.5.5.1 United Arab Emirates

5.5.5.2 South Africa

5.5.5.3 Morocco

5.5.5.4 Nigeria

5.5.5.5 Egypt

5.5.5.6 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Ranking Analysis

6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

6.4.1 China Mengniu Dairy Co Ltd

6.4.2 Inner Mongolia Yili Industrial Group Co Ltd

6.4.3 Nestlé SA

6.4.4 Yakult Honsha Co Ltd

6.4.5 General Mills Inc. (Yoplait)

6.4.6 Chobani Global Holdings LLC

6.4.7 Lactalis Group

6.4.8 Fonterra Co-operative Group Ltd

6.4.9 Arla Foods am-ba

6.4.10 Saputo Inc.

6.4.11 Gujarat Co-operative Milk Marketing Federation (Amul)

6.4.12 Meiji Holdings Co Ltd

6.4.13 Bright Dairy & Food Co Ltd

6.4.14 Grupo Lala S.A.B. de C.V.

6.4.15 Ultima Foods Inc.

6.4.16 Valio Oy

6.4.17 Lifeway Foods Inc.

6.4.18 Morinaga Milk Industry Co Ltd

6.4.19 The Hain Celestial Group Inc.

6.4.20 Yoso Brands

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK