| 出版社 | TECHCET |

| 出版年月 | 2025年6月 |

CVD, ALD Hi K & Metal Precursors 2025-2026

TECHCET「CVD、ALD High-K、金属プリカーサーのサプライチェーン市場分析 2025-2026年- CVD, ALD Hi K & Metal Precursors 2025-2026 」は半導体デバイス製造で使用されているプリカーサー(前駆体)の市況とサプライチェーンを調査・分析しています。主要サプライヤー、原料のサプライチェーンにおける課題と動向、サプライヤの市場シェア見込み、材料市場の予測など、半導体デバイス製造向けプリカーサーの市場の把握に欠かせない情報を提供します。

当レポートの特長

- 技術動向情報:CVD(化学気相成長法)法による有機前駆体と無機前駆体、High-K金属酸化物、バリア層、金属相互接続、キャッピング層を含むALD(原子層堆積法)の応用

- サプライチェーンマネージャー、プロセス統合、研究開発管理者に関する情報。事業開発と財政情報も含む

- 主要サプライヤ情報、材料のサプライチェーンにおける課題と動向、サプライヤの市場シェア、材料市場関連予測

主な掲載内容

- エグゼクティブサマリー

- 調査範囲、目的、調査手法

- 半導体産業の市場状況と展望

- プリカーサー市場動向

- プリカーサー市場動向

- ロジックデバイスの推移からみる市場成長促進要因

- DRAMデバイスの推移からみる市場成長促進要因

- 3D NANDデバイスの推移からみる市場成長促進要因

- 市場統計データ:金属&High-Kプリカーサーのセグメント別5年予測

- プリカーサーの生産能力拡大

- 金属プリカーサーの材料の供給と需要のバランス:総合評価

- 価格動向

- 技術動向/技術促進要因

- DRAM

- 3D NAND

- ロジック

- 金属プリカーサー技術の総合概観

- 2001年以来のCVDとALDの知的財産(IP)出願

- 地域別考察:CVDとALDにおける知的財産(IP)出願

- EHSと貿易/物流問題

- プリカーサー市場動向についてのアナリストの評価

- 供給サイドの市況

- 主要サプライヤ:活動と公表収益

- プリカーサー材料市場シェア

- 事業分離、M&A、提携関係

- 工場閉鎖

- 新規参入企業:報告なし

- 継続の危機にあるサプライヤーまたは部品/製品ライン:なし

- プリカーサーサプライヤに対するTECHCETのアナリストの評価

- サブティアのサプライチェーン:材料

- サブティアのサプライチェーン:原料と市場概観

- サブティアのサプライチェーン:プリカーサーの主要製造元

- ALD/CVD装置OEMサブティアのM&A

- 貴金属サプライヤの市場動向

- 産業用と半導体グレードの比較:ティア1とサブティアの品質比較

- サブティアのサプライチェーン:サブティアのプリカーサー市場ランキング

- 金属プリカーサー原料サプライチェーンにおける懸念

- サブティアサプライチェーン:ディスラプション

- サブティアサプライチェーンにおける現地投資へのシフト

- サブティアサプライチェーンのEHSと物流問題

- サブティアサプライチェーンにおける工場閉鎖:報告なし

- サブティアサプライチェーンの価格動向

- サブティアサプライチェーンに関するTECHCETアナリストの評価

- サプライヤ情報

Description

This report covers the market landscape and supply-chain for Precursors used in semiconductor device fabrication. It includes information about key suppliers, issues/trends in the material supply chain, estimates on supplier market share, and forecast for the material segments.

- Provides market and technical trend information on organic and inorganic precursors, addressing CVD, ALD applications including high κ metal-oxides, barrier layers, metal interconnects, and capping layers, among others.

- Provides focused information for supply-chain managers, process integration and R&D directors, as well as business development and financial analysts

- Covers information about key suppliers, issues/trends in the electronics material supply chain, estimates on supplier market share, and forecast for the electronics material segments

- Includes 3 Quarterly Updates, with updates on market trends and forecasts from the analyst

Analyst

Jonas Sundqvist, Ph.D.

Sr. Technology Analyst of TECHCET— covers Electronic Gases and ALD & CVD precursors and related technologies, and the co-chair of the Annual Critical Materials Council (CMC) Conference. His over 20 years of work experience includes Group Leader of the Thin-Film Technologies Group at The Fraunhofer Institute for Ceramic Technologies and Systems (IKTS) in Germany, Clean Room Operations Manager for Lund Nano Lab, Lund University in Sweden and Group Leader of the ALD & High-k devices group at Fraunhofer’s Center Nanoelectronic Technologies (CNT) in Germany, which included 28nm node work for GLOBALFOUNDRIES Fab1.

Previously, at Infineon Memory Development Centre (MDC), he developed high-k and metal nitride ALD processes, and at Qimonda, he was a materials manager focused on the ALD/CVD precursors supply-chain. He holds a Ph.D. and an M.S. in inorganic chemistry from Uppsala University, Sweden & Institute for Micromanufacturing, Louisiana Teche, USA, a B.S. in electrical and electronics engineering from Lars Kagg, and nine patents and 40 related scientific publications.

Jonas Sundqvist is on the Scientific Committee for AVS ALD and has co-chaired ALD2016 Dublin Ireland, and the annual EFDS ALD for Industry Workshop in Germany.

プレスリリース

※下記は2024年版のプレスリリースです。

(抄訳)半導体製造デバイス向けALD/CVDプリカーサー市場は先進的用途が促進要因

大きな成長の可能性を見せるモリブデン(Mo)、フッ化タングステン (WF6)、コバルト(Co)

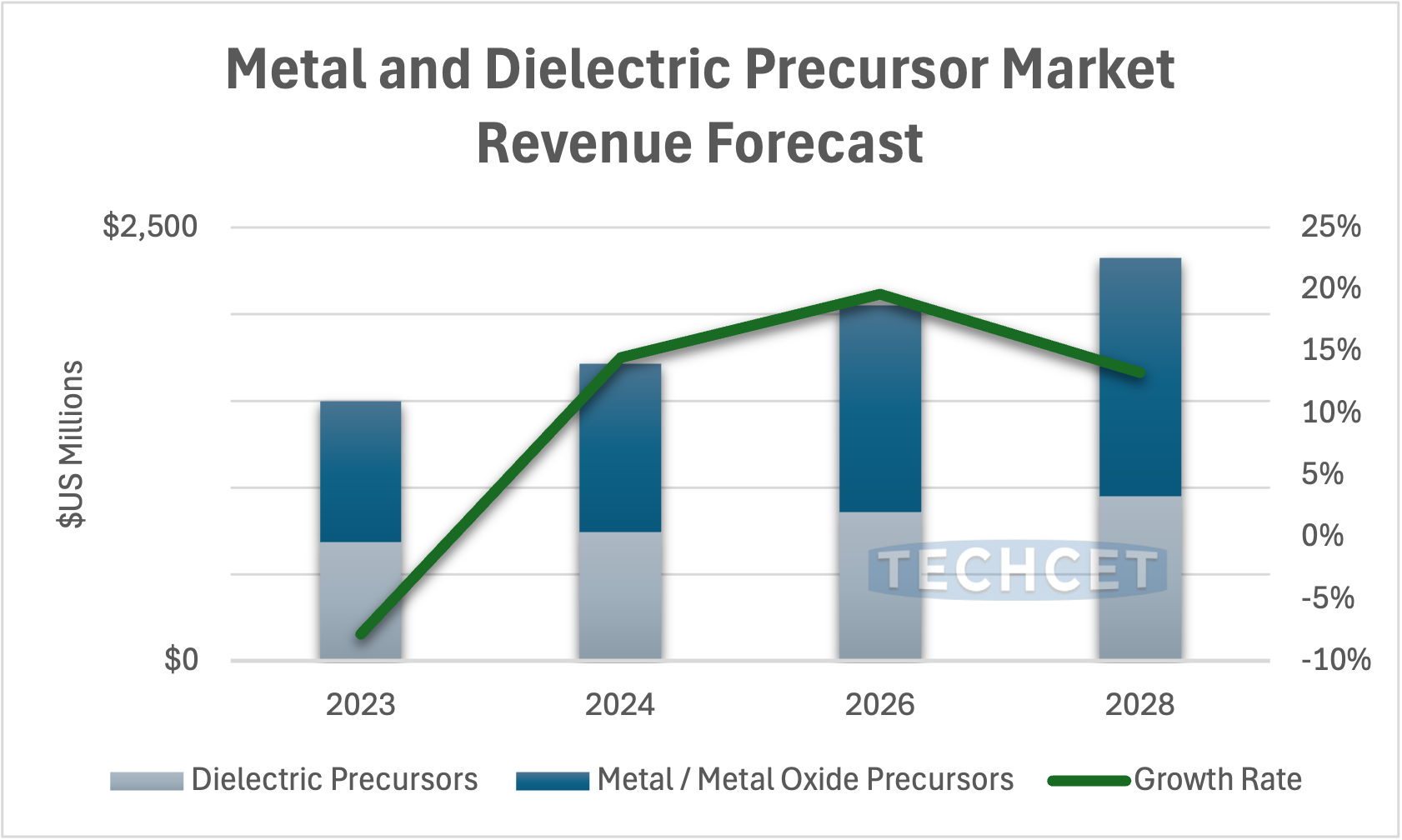

2024年8月1日、カリフォルニアサンディエゴ:TECHCET – 半導体サプライチェーンのレジリエンスに関する材料市場情報を提供するアドバイザリー会社・TECHCETは半導体用金属および酸化物前駆体の収益が2024年に17億ドルに達し、2023年より15%増加すると予測しています。これはすべてのフロントプロセス材料セグメントの中で最も高い成長率となります。金属/金属酸化物前駆体は市場の大部分を占め、予想収益は9億7,200万ドルです。一方、誘電体前駆体は合計7億4,200万ドルになると予想されています。前駆体市場は2023年から2028年にかけてCAGR9%で成長すると予測されています。

Semiconductor ALD/CVD Precursors Driven by Advanced Applications

San Diego, CA, August 1, 2024: TECHCET — the advisory firm providing materials market information for semiconductor supply chain resilience — is forecasting semiconductor metal and oxide precursors to reach US$1.7 B in revenues in 2024, rising 15% over 2023. This is the highest growth rate among all front process materials segments. Metal/Metal-oxide precursors occupy the majority of the market with expected revenues at $972 M, while Dielectric Precursors are expected to total US$742 M. The precursor market is forecasted to increase at a 9% CAGR from 2023-2028. More information on market forecasting and trends is included in TECHCET’s new Critical Materials Reports™ on ALD/CVD Precursors.

Significant investments are being made in advanced process technologies such as GAA FETs, EUV lithography, and high-k/metal gate transistors, all of which are crucial for next-generation Logic, DRAM, and 3D NAND devices. Recovery of precursor revenue growth is being driven by AI and advanced technology applications. Additionally, metallization for backside power delivery at 2nm logic nodes and beyond is also pushing up growth for metal precursors.

Molybdenum (Mo) precursors, specifically MoO2Cl2, are projected to experience high growth due to their favorable electrical properties and application in next-generation devices. Other precursors strongly tied to advanced device nodes include Cobalt precursors (CoCOCp and CCTBA) and Tungsten Hexafluoride (WF6).

The shift towards more sustainable and efficient production methods is influencing the development of new precursors, with a focus on reducing environmental impact and improving manufacturing efficiency.

Major industry players are expanding their production capacities in order to meet growing demand. Companies such as Air Liquide, Merck, and Gelest/Mitsubishi Chemical Group are making significant investments in production facilities in key regions like Taiwan, South Korea, and the US.

The newly released TECHCET Critical Materials Reports™ on ALD/CVD Precursors contains details on market and technology trends and supplier profiles.