Wearable Motion Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Wearable Motion Sensor Market Report is Segmented by Type (Accelerometers, Gyroscopes, Magnetometers, and More), Application (Fitness Bands, Activity Monitors, Smart Clothing, and More ), End-User (Healthcare, Consumer Electronics, Industrial, Military, An More), Power Consumption (Ultra-Low Power (less Than 1mW), Standard Power (10-50mW), and More), and Geography.

ウェアラブルモーションセンサー市場レポートは、タイプ(加速度計、ジャイロスコープ、磁力計など)、アプリケーション(フィットネスバンド、アクティビティモニター、スマート衣料など)、エンドユーザー(ヘルスケア、民生用電子機器、産業、軍事など)、消費電力(超低電力(1mW未満)、標準電力(10〜50mW)など)、および地域別にセグメント化されています。

| 出版 | Mordor Intelligence |

| 出版年月 | 2025年07月 |

| ページ数 | 120 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-1229512295 |

ウェアラブルモーションセンサーの市場規模は、2025年に25億米ドルと評価され、2030年には46億米ドルに達し、この期間に12.97%のCAGRを記録すると予測されています。ヘルスケア、民生用電子機器、産業安全および防衛における採用の拡大がこの軌道を維持する一方で、小型化とデバイス上の信号処理のブレークスルーにより、かつては個別部品だったものがコネクテッドプロダクトに不可欠な要素へと変化しています。遠隔患者モニタリングに対する規制当局のサポート、健康志向の消費者行動の高まり、そして正確なリアルタイムモーションデータに依存するシームレスなヒューマンマシンインターフェースへの移行によって、需要は押し上げられています。市場リーダーは、差別化を図るためにセンサーフュージョン、超低電力設計、エッジAIを重視していますが、新興プレーヤーはスマートテキスタイルや兵士の近代化といったニッチな機会を狙っています。MEMS製造における供給側の制約と、データ主権に関連するコンプライアンスコストの増大は、依然としてタイムリーな生産能力充足に対する最も顕著なボトルネックとなっています。

Wearable Motion Sensors Market Analysis

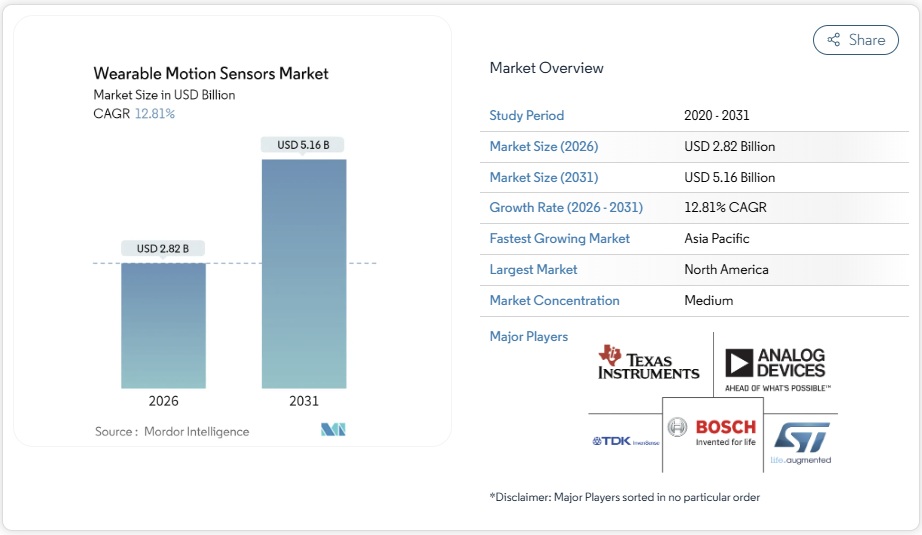

The wearable motion sensors market size is valued at USD 2.5 billion in 2025 and is forecast to reach USD 4.6 billion by 2030, registering a 12.97% CAGR over the period. Expanding adoption across healthcare, consumer electronics, industrial safety and defense sustains this trajectory, while breakthroughs in miniaturization and on-device signal processing convert once-discrete components into indispensable enablers of connected products. Demand is reinforced by regulatory support for remote patient monitoring, rising health-conscious consumer behavior, and the shift toward seamless human–machine interfaces that rely on precise real-time motion data. Market leaders emphasize sensor fusion, ultra-low-power design and edge AI to differentiate, whereas emerging players target niche opportunities such as smart textiles and soldier modernisation. Supply-side constraints in MEMS manufacturing and growing compliance costs tied to data sovereignty remain the most visible bottlenecks for timely capacity fulfilment.

Global Wearable Motion Sensors Market Trends and Insights

AI-enabled Sensor Fusion Driving Medical-Grade Wearables

Integrating on-sensor AI with multi-axis inertial data is converting consumer devices into clinical-grade monitors, enabling reliable detection of subtle gait or tremor changes linked to Parkinson’s and other neuro-motor disorders. Studies report 84% accuracy in differentiating early Parkinson’s tremor from essential tremor, an achievement that expands home-based, continuous care models and reduces reliance on episodic clinical evaluations. Growing payer acceptance of algorithm-supported diagnostics accelerates hospital adoption, while consumer brands add medical features to retain users within ecosystem subscriptions.

Sub-milliwatt MEMS for Eldercare in Japan & Korea

Sensors consuming below 1 mW allow multi-week operation without charging, a prerequisite for elderly users who may forget to maintain devices. Japan’s national long-term care system saw 23% fewer hospitalisations when such sensors enabled automatic fall alerts and daily activity profiling. Korean public-private pilots demonstrate similar savings, encouraging scale-up across community health networks and driving regional demand spillover into China’s ageing-at-home initiatives.

Algorithmic Limits on Tremor Differentiation

Current unsupervised models reach only 57.1% accuracy in multi-class tremor severity classification, well below clinical thresholds, limiting reimbursement for neurological wearables. Small, diverse data sets and noisy real-world environments hinder progress, slowing hospital uptake despite promising research prototypes.

Other drivers and restraints analyzed in the detailed report include:

- U.S. RPM Reimbursement Boost

- EU Digital Product Passport-Linked Usage Analytics

- MEMS Foundry Capacity Crunch

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The wearable motion sensors market saw accelerometers retain 32.4% share in 2024, underpinning activity trackers, gesture interfaces and basic fall detection. That dominance reflects mature cost curves and micro-amp sleep currents. In contrast, MEMS combo sensors post a 14.66% CAGR by fusing accelerometer, gyroscope and magnetometer functions within a single ASIC that off-loads board-level integration. STMicroelectronics’ LSM6DSV16BX, for instance, embeds a 6-axis IMU plus an audio accelerometer for bone-conduction-based commands in hearables. Combo adoption narrows the performance gap with discrete IMUs while lowering power draw, ideal for tiny rings and medical patches.

Gyroscopes support sub-degree orientation fidelity in AR/VR headsets and advanced biomechanics analysis yet carry higher milliwatt budgets, so vendors pair duty-cycled modes with predictive algorithms to stretch per-charge runtime. Magnetometers deliver absolute heading, essential for outdoor sports watches navigating GPS multipath. Pressure sensors, a smaller but vital niche, calibrate altitude change for stair-climb counting and swimming lap depth. Forward-looking roadmaps integrate bio-potential or chemical channels alongside motion axes, signalling a future where inertial and physiological data converge inside unified sensor nodes, further strengthening the wearable motion sensors market.

Fitness bands led 24% of application revenues in 2024, benefiting from established brand ecosystems, low entry price and cross-selling of subscription analytics. However, textile-embedded sensor threads shift monitoring from gadget to garment, supporting a 14.91% CAGR through 2030. Conductive yarns and printed stretch sensors enable shirts that track joint kinematics, posture and respiratory rates during daily routines, freeing users from dedicated devices.

AR/VR headsets remain a high-growth enclave, demanding sub-millisecond latency orientation updates for immersive simulation. Ear-wear integrates head-gesture sensing for hands-free calls, while smart rings deliver sleep staging in tiny form factors. The convergence of motion and electrochemical sensing within fabrics widens health dashboards to hydration, electrolyte loss and thermal stress parameters, underscoring how seamless experiences keep the wearable motion sensors market expanding beyond novelty phases.

The Wearable Motion Sensor Market Report is Segmented by Type (Accelerometers, Gyroscopes, Magnetometers, and More), Application (Fitness Bands, Activity Monitors, Smart Clothing, and More ), End-User (Healthcare, Consumer Electronics, Industrial, Military, An More), Power Consumption (Ultra-Low Power (less Than 1mW), Standard Power (10-50mW), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.7% of 2024 revenue, anchored by Medicare reimbursement reform that locks remote motion monitoring into mainstream care pathways. The region’s venture ecosystem funnels capital into edge-AI silicon, while privacy statutes push vendors toward on-device inference, preserving user trust. Supply constraints are mitigated by near-shoring policies and Defense Production Act incentives that favour domestic MEMS lines.

Asia Pacific registers the fastest 16.91% CAGR through 2030, reflecting China’s tier-2 fabs embracing energy-harvesting architectures and Korea’s smart-city pilots embedding motion tags in elder apartments. Government grants offset initial higher BOM costs, while consumer appetite for feature-rich wearables remains unabated. Japan’s insurers reimburse smart-shirt-based risk scoring for seniors, spurring textile sensor investment.

Europe maintains methodical expansion, its Digital Product Passport mandate pushing life-cycle transparency and fostering premium after-sales analytics. GDPR compliance elevates spend on secure edge firmware and sovereign cloud bridges. Latin America and the Middle East & Africa trail in volumes yet notch double-digit growth where urban private hospitals adopt fall-detection watches. Cross-border e-commerce and multinational OEM assembly lines stitch regions into a globally interdependent wearable motion sensors market.

List of Companies Covered in this Report:

- Bosch Sensortec GmbH

- TDK InvenSense

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Panasonic Industry Co., Ltd.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH (Sensors)

- TE Connectivity

- Qualcomm Technologies Inc.

- Sensirion AG

- Xsens (Movella)

- Valencell Inc.

- OMRON Corporation

- Garmin Ltd.

- Polar Electro Oy

- Fitbit LLC (Google)

- Apple Inc.

- Oura Health Oy

- Xiaomi Corporation

- Goertek Inc.

- Huami (Zepp Health)

- Withings SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 AI-enabled Sensor Fusion Driving Medical-Grade Wearables

4.2.2 Sub-milliwatt MEMS for Eldercare in Japan and Korea

4.2.3 U.S. RPM Reimbursement Boost

4.2.4 EU Digital Product Passport-Linked Usage Analytics

4.2.5 Micro Energy-Harvesting Modules in China

4.2.6 NATO Soldier Modernisation Demand

4.3 Market Restraints

4.3.1 Algorithmic Limits on Tremor Differentiation

4.3.2 MEMS Foundry Capacity Crunch

4.3.3 Data-Sovereignty Compliance Costs

4.3.4 Smart-Textile Interconnect Failures

4.4 Value / Supply-Chain Analysis

4.5 Regulatory and Technological Outlook

4.6 Porter’s Five Forces Analysis

4.6.1 Bargaining Power of Suppliers

4.6.2 Bargaining Power of Consumers

4.6.3 Threat of New Entrants

4.6.4 Threat of Substitutes

4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

5.1 By Type

5.1.1 Accelerometers

5.1.2 Gyroscopes

5.1.3 Magnetometers

5.1.4 Inertial Measurement Units (IMUs)

5.1.5 MEMS Combo Sensors

5.1.6 Pressure Sensors

5.2 By Application

5.2.1 Fitness Bands

5.2.2 Activity Monitors

5.2.3 Smart Clothing

5.2.4 AR/VR Headsets

5.2.5 Smart Rings and Jewelry

5.2.6 Ear-wear and Hearing Aids

5.3 By End-user Industry

5.3.1 Healthcare and Medical Devices

5.3.2 Consumer Electronics and Lifestyle

5.3.3 Industrial and Enterprise Safety

5.3.4 Military and Defense

5.3.5 Government and Public Utilities

5.4 By Power Consumption

5.4.1 Ultra-Low Power (Less than1mW)

5.4.2 Low Power (1-10mW)

5.4.3 Standard Power (10-50mW)

5.4.4 High Power (Greater than 50mW)

5.5 By Geography

5.5.1 North America

5.5.1.1 United States

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.2 Europe

5.5.2.1 United Kingdom

5.5.2.2 Germany

5.5.2.3 France

5.5.2.4 Italy

5.5.2.5 Rest of Europe

5.5.3 Asia-Pacific

5.5.3.1 China

5.5.3.2 Japan

5.5.3.3 India

5.5.3.4 South Korea

5.5.3.5 Rest of Asia-Pacific

5.5.4 Middle East

5.5.4.1 Israel

5.5.4.2 Saudi Arabia

5.5.4.3 United Arab Emirates

5.5.4.4 Turkey

5.5.4.5 Rest of Middle East

5.5.5 Africa

5.5.5.1 South Africa

5.5.5.2 Egypt

5.5.5.3 Rest of Africa

5.5.6 South America

5.5.6.1 Brazil

5.5.6.2 Argentina

5.5.6.3 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

6.4.1 Bosch Sensortec GmbH

6.4.2 TDK InvenSense

6.4.3 STMicroelectronics N.V.

6.4.4 Analog Devices, Inc.

6.4.5 Texas Instruments Incorporated

6.4.6 Panasonic Industry Co., Ltd.

6.4.7 Infineon Technologies AG

6.4.8 NXP Semiconductors N.V.

6.4.9 Samsung Electronics Co. Ltd.

6.4.10 Robert Bosch GmbH (Sensors)

6.4.11 TE Connectivity

6.4.12 Qualcomm Technologies Inc.

6.4.13 Sensirion AG

6.4.14 Xsens (Movella)

6.4.15 Valencell Inc.

6.4.16 OMRON Corporation

6.4.17 Garmin Ltd.

6.4.18 Polar Electro Oy

6.4.19 Fitbit LLC (Google)

6.4.20 Apple Inc.

6.4.21 Oura Health Oy

6.4.22 Xiaomi Corporation

6.4.23 Goertek Inc.

6.4.24 Huami (Zepp Health)

6.4.25 Withings SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-space and Unmet-Need Assessment