Collaborative Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Collaborative Robots Market Report is Segmented Into by Payload (Less Than 5Kg, 5-9 Kg, 10-20 Kg, More Than 20 KG), Component (Hardware and More), Application (Material Handling, Pick and Place and More), End-User Industry (Electronics, Automotive, and More), Programming Method (Hand-Guiding and More), and Geography.

協働ロボット市場レポートは、ペイロード(5kg未満、5〜9kg、10〜20kg、20kg以上)、コンポーネント(ハードウェアなど)、アプリケーション(マテリアルハンドリング、ピックアンドプレースなど)、エンドユーザー産業(エレクトロニクス、自動車など)、プログラミング方法(ハンドガイドなど)、および地域別にセグメント化されています。

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 190 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-13244 |

協働ロボット市場は2025年に19億米ドルと評価され、予測期間(2026~2031年)中に20.15%のCAGRで成長し、2026年の22億8,000万米ドルから2031年には57億2,000万米ドルに達すると推定されています。

改訂されたISO/TS 15066規格による安全要件の明確化、税制優遇措置による投資回収期間の短縮、そして労働力不足による柔軟な自動化の緊急性が高まるにつれ、需要は加速しています。製造業では、労働者の代替ではなく生産性向上を目的とした協働ロボットの導入がますます増加しており、成熟したソフトウェアと簡素化されたプログラミングによって導入サイクルが短縮されています。積載能力の増大、倉庫自動化のニーズ、そしてサービス部門におけるユースケースの拡大は、グローバルバリューチェーン全体における導入の勢いを強めています。

セグメント分析

- 2025年には、5kg未満のモデルが協働ロボット市場の52.40%を占め、主に精度が極めて重要となる電子機器や医療機器の組立においてそのシェアを占めました。一方、10~20kgクラスのモデルは年平均成長率22.95%で成長しており、パレタイジング、マシンテンディング、自動車部品組立への関心の高まりを示しています。中型モデルはリーチも長く、作業員を新たな安全区域に移動させることなくラインサイドでの作業を可能にします。重量級(20kg超)の協働ロボットは依然としてニッチ市場ですが、防爆認証が不可欠な塗装・化学薬品製造現場では高い価値を発揮しています。ロボットメーカーが動的トルクセンシングの精度向上を進めるにつれ、中型可搬重量の協働ロボット市場は2028年以降、軽量モデルを上回る規模に成長すると予測されています。

- 5~9kgの重量範囲では、ベンダーはビジョンとAIを組み合わせ、1秒未満のピックアンドプレースサイクルを実現し、半導体後工程のオペレーションに対応しています。この変化は、器用さと強度を兼ね備え、フリートの複雑さを軽減するユニットを求める顧客のニーズを反映しています。協働ロボット市場を活用するメーカーは、グリッパーとコントローラーをペイロードクラス間で標準化できるオプションを獲得し、スペアパーツの管理とオペレーターのトレーニングを簡素化できます。

- 2025年にはハードウェアが収益の71.35%を生み出しましたが、ユーザーが機械よりもインテリジェンスを重視するにつれて、ソフトウェアは年間27.15%の進歩を遂げています。ビジョンガイドによる経路計画、フリートオーケストレーション、予知保全モジュールは、ハードウェアの単発販売を継続的なライセンスへと転換し、ベンダーの利益プールをデジタルサービスへと移行させます。協働ロボットは現在、ROS互換のAPIとクラウドコネクタを搭載しており、迅速なアプリ統合が可能です。

- コンサルティングおよびライフサイクルサービスの成長は、中小企業が外部の専門知識に依存していることを反映しています。ベンダーは、安全性評価、プログラミング、オペレーターのスキルアップをサブスクリプションモデルに統合することで、協働ロボット市場をさらに拡大させています。時間の経過とともに、ソフトウェア定義のペイロードアップグレードによって交換サイクルが短縮され、工場管理者はフレームをより長く稼働させながら、ファームウェアの強化によってパフォーマンスを向上させることができます。

- 協働ロボット市場レポートは、ペイロード(5kg未満、5~9kg、10~20kg、20kg超)、コンポーネント(ハードウェアなど)、用途(マテリアルハンドリング、ピックアンドプレースなど)、エンドユーザー産業(エレクトロニクス、自動車など)、プログラミング手法(ハンドガイドなど)、および地域別にセグメント化されています。市場予測は金額(米ドル)で提供されます。

Collaborative Robot Market Analysis

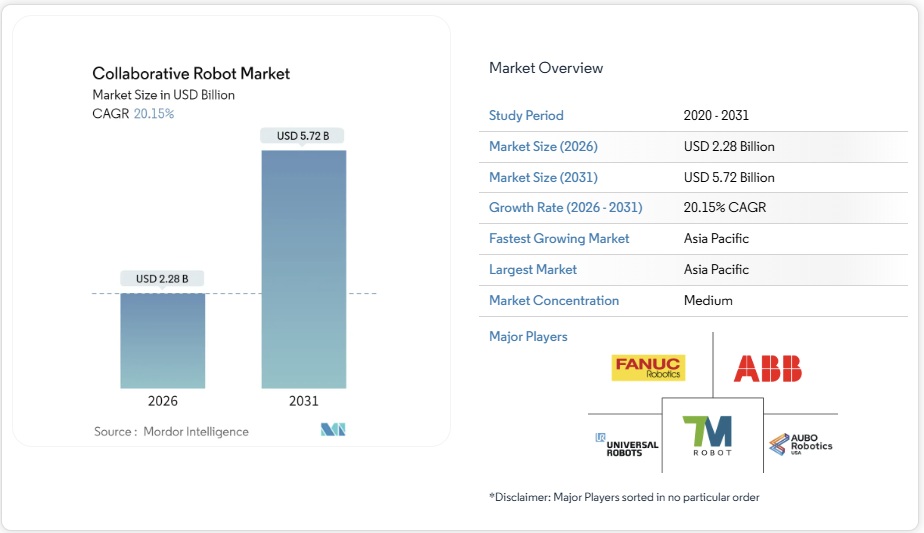

The Collaborative Robot Market was valued at USD 1.9 billion in 2025 and estimated to grow from USD 2.28 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 20.15% during the forecast period (2026-2031).

Demand accelerates as updated ISO/TS 15066 standards clarify safety requirements, tax incentives lower payback periods, and labor shortages raise the urgency of flexible automation. Manufacturers increasingly deploy cobots to lift productivity rather than replace workers, while maturing software and simplified programming shorten deployment cycles. Growing payload capacities, warehouse automation needs, and widening service-sector use cases strengthen adoption momentum across global value chains.

Global Collaborative Robot Market Trends and Insights

Cost-effective Redeployment in High-mix Manufacturing

European and North American factories now rotate cobots across assembly cells within a single shift, cutting changeover from weeks to hours This agility lets automotive suppliers accept smaller, high-margin orders while retaining automation gains.

OEM Push Toward Plug-and-Play Cobots for SMEs

New controllers, capped wiring, and pre-loaded task libraries allow small manufacturers to install cobots without specialist integrators. Universal Robots’ UR-series refresh shows how cycle-time gains and intuitive hand-guiding shrink total cost of ownership, opening the collaborative robot market to thousands of first-time users

Integration Bottlenecks with Brownfield PLC Architectures

Legacy PLCs often lack real-time Ethernet or safe-motion channels, forcing costly controller upgrades when cobots are added to decades-old lines . The expense pushes some automotive plants to defer adoption until full line overhauls.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-commerce Fulfilment Drives Warehouse Cobots

- ISO/TS 15066 Updates Easing Liability Concerns

- Payload-Speed Trade-offs Limiting Heavy-duty Tasks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sub-5 kg models controlled 52.40% of the collaborative robot market in 2025, largely in electronics and medical device assembly where precision is paramount. The 10-20 kg band, however, is pacing a 22.95% CAGR, signaling rising interest in palletizing, machine tending, and automotive sub-assembly. Mid-range units also integrate longer reaches, enabling line-side work without moving humans to new safety zones. Heavy-duty (>20 kg) cobots remain niche but prove valuable in paint and chemical environments where explosion-proof certification is essential. As robot makers refine dynamic torque sensing, the collaborative robot market size for mid-payloads is projected to outgrow light units after 2028.

Within 5-9 kg, vendors package vision and AI for pick-and-place cycles under one second, catering to semiconductor back-end operations. The shift reflects buyers’ search for units that bridge dexterity and strength, reducing fleet complexity. Manufacturers leveraging the collaborative robot market gain the option to standardize grippers and controllers across payload classes, simplifying spare-parts management and operator training.

Hardware generated 71.35% of revenue in 2025, yet software is advancing 27.15% annually as users emphasize intelligence over mechanics. Vision-guided path planning, fleet orchestration, and predictive maintenance modules convert one-time hardware sales into recurring licenses, moving vendor profit pools toward digital services. Cobots now ship with ROS-compatible APIs and cloud connectors, allowing quick app integrations.

Growth in consulting and lifecycle services reflects SME reliance on external expertise. Vendors bundle safety assessment, programming, and operator up-skilling into subscription models, further enlarging the collaborative robot market. Over time, software-defined payload upgrades may lower replacement cycles, letting plant managers keep frames in service longer while lifting performance through firmware enhancements.

Collaborative Robots Market Report is Segmented Into by Payload (Less Than 5Kg, 5-9 Kg, 10-20 Kg, More Than 20 KG), Component (Hardware and More), Application (Material Handling, Pick and Place and More), End-User Industry (Electronics, Automotive, and More), Programming Method (Hand-Guiding and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 40.55% of 2025 revenue, propelled by China’s 1-trillion-yuan robotics push under the 14th Five-Year Plan and Japan’s Society 5.0 roadmap that blends AI, IoT, and next-generation automation . Chinese electronics and battery plants install cobots for precision gluing and cell stacking, while Japanese hospitals test service robots for elder care. South Korea’s Fourth Intelligent Robot Basic Plan funds local SMEs to adopt collaborative solutions, reinforcing domestic supply chains.

North America ranks second. U.S. reshoring incentives combined with record labor scarcity elevate the market. Semiconductor fabs subsidized by the CHIPS Act integrate dual-arm cobots for wafer loading, shrinking transport contamination risk. Canadian auto parts suppliers adopt mid-payload units for die-casting part finishing, while Mexican maquiladoras deploy cobots to balance wage inflation with export competitiveness. Cross-border standardization allows integrators to reuse cell designs, accelerating rollout.

Europe shows robust uptake led by Germany’s Industrie 4.0 lighthouse projects linking MES data to cobot fleets. Horizon Europe grants finance human-machine interface research, spurring startups in Denmark and Italy that build AI motion-planning stacks. French aerospace plants choose cobots for carbon-fiber trimming, citing weight reduction and ergonomic gains. Rising energy costs push factories toward leaner layouts where cobots save floor space relative to fenced robots. Environmental regulations also favor cobots’ lower idle power draw compared with hydraulic presses, aiding the collaborative robot market size in sustainability-conscious regions.

List of Companies Covered in this Report:

- Universal Robots AS

- FANUC Corp.

- ABB Ltd.

- KUKA AG

- Yaskawa Electric Corp.

- Techman Robot Inc.

- Doosan Robotics Inc.

- AUBO Robotics

- Kawasaki Heavy Industries Ltd.

- Omron Corporation

- Epson Robots

- Precise Automation Inc.

- Stäubli International AG

- Hanwha Robotics

- Denso Wave Inc.

- Comau SpA

- Hyundai Robotics

- Festo SE and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Cost-effective Re-deployment in High-mix Manufacturing (Europe)

4.2.2 OEM Push Toward Plug-and-Play Cobots for SMEs (North America)

4.2.3 Rapid E-Commerce Fulfilment Drives Warehouse Cobots (Asia)

4.2.4 ISO/TS 15066 Updates Easing Liability Concerns (Global)

4.2.5 Tax Incentives for Reshoring Automation (United States)

4.3 Market Restraints

4.3.1 Integration Bottlenecks with Brownfield PLC Architectures

4.3.2 Payload-Speed Trade-offs Limiting Heavy-duty Tasks

4.3.3 Fragmented Component Ecosystem Inflates TCO for SMEs

4.3.4 Insurance Underwriting Gaps for HumanRobot Workcells

4.4 Value / Supply-Chain Analysis

4.5 Regulatory and Technological Outlook

4.6 Porters Five Forces

4.6.1 Bargaining Power of Suppliers

4.6.2 Bargaining Power of Buyers

4.6.3 Threat of New Entrants

4.6.4 Intensity of Competitive Rivalry

4.6.5 Threat of Substitute Products

4.7 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

5.1 By Payload

5.1.1 Less than 5 kg

5.1.2 5 – 9 kg

5.1.3 10 – 20 kg

5.1.4 More than 20 kg

5.2 By Component

5.2.1 Hardware

5.2.2 Software

5.2.3 Services

5.2.3.1 Consulting and Integration

5.2.3.2 Maintenance and Training

5.3 By Application

5.3.1 Material Handling

5.3.2 Pick and Place

5.3.3 Assembly

5.3.4 Palletizing and De-palletizing

5.3.5 Welding and Soldering

5.3.6 Quality Testing and Inspection

5.3.7 Packaging

5.3.8 Other Applications

5.4 By End-user Industry

5.4.1 Automotive

5.4.2 Electronics and Semiconductors

5.4.3 General Manufacturing

5.4.4 Food and Beverage

5.4.5 Chemicals and Pharmaceuticals

5.4.6 Logistics and E-commerce

5.4.7 Healthcare and Life Sciences

5.4.8 Metals and Machining

5.4.9 Other Industries

5.5 By Programming Method (qualitative only)

5.5.1 Hand-Guiding / Direct Teaching

5.5.2 Lead-through Teaching

5.5.3 Offline Programming and Simulation

5.6 By Geography

5.6.1 North America

5.6.1.1 United States

5.6.1.2 Canada

5.6.1.3 Mexico

5.6.2 Europe

5.6.2.1 Germany

5.6.2.2 United Kingdom

5.6.2.3 France

5.6.2.4 Italy

5.6.2.5 Nordics

5.6.3 Asia-Pacific

5.6.3.1 China

5.6.3.2 Japan

5.6.3.3 India

5.6.3.4 South Korea

5.6.3.5 Australia and New Zealand

5.6.4 South America

5.6.4.1 Brazil

5.6.4.2 Argentina

5.6.5 Middle East

5.6.5.1 United Arab Emirates

5.6.5.2 Saudi Arabia

5.6.5.3 Turkey

5.6.6 Africa

5.6.6.1 South Africa

5.6.6.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles

6.4.1 Universal Robots AS

6.4.2 FANUC Corp.

6.4.3 ABB Ltd.

6.4.4 KUKA AG

6.4.5 Yaskawa Electric Corp.

6.4.6 Techman Robot Inc.

6.4.7 Doosan Robotics Inc.

6.4.8 AUBO Robotics

6.4.9 Kawasaki Heavy Industries Ltd.

6.4.10 Omron Corporation

6.4.11 Epson Robots

6.4.12 Precise Automation Inc.

6.4.13 Stäubli International AG

6.4.14 Hanwha Robotics

6.4.15 Denso Wave Inc.

6.4.16 Comau SpA

6.4.17 Hyundai Robotics

6.4.18 Festo SE and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-Space and Unmet-Need Assessment