| 出版社 | Berg Insight |

| 出版年月 | 2025年11月 |

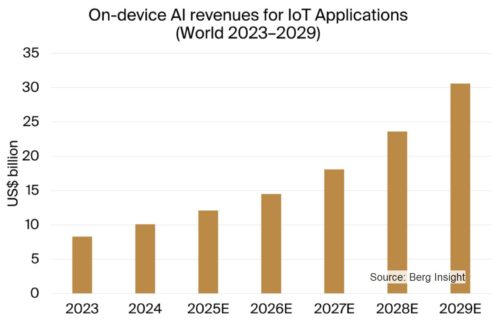

オンデバイスAIソリューションによる収益は2024年に101億ドルとなり、2029年までに306億ドルになるとBerg Insightは予測しています。

Berg Insight(ベルグインサイト)「IoT用途でのオンデバイスAI 第1版 – The On-device AI Market for IoT Applications – 1st Edition」はIoTで使用されるオンデバイスAI市場を分析・解説し、2029年までの予測結果を提供します。

当レポートの特長

- 市場の主要企業との多数のエグゼクティブインタビューからのインサイト

- オンデバイスAIのエコシステムの360度ビュー

- 2029年までのオンデバイスAIハードウェアとソフトウェアの市場価値予測

- オンデバイスAIハードウェアとソフトウェアプロバイダの主要40社の市場シェア

- オンデバイスAIハードウェアとソフトウェアプロバイダの主要31社の詳細な企業情報

- 最も重要な業種に関するユースケース情報

- 市場動向と重要動向に関する詳細な分析

主な掲載内容

- エグゼクティブサマリー

- 概説

- クラウドとオンデバイス処理の比較

- AIoT:AIとIoTのコンバージェンス

- 人工知能(AI)技術概要

- オンデバイスAIのエコシステム

- 市場分析

- オンデバイスAIの業界状況

- 市場規模と予測

- ソリューションプロバイダの市場シェア

- 業界での採用とユースケース

- 企業情報と戦略

Highlights from the report:

- Insights from numerous executive interviews with market leading companies.

- 360-degree overview of the on-device AI ecosystem.

- Market value forecast for on-device AI hardware and software until 2029.

- Market shares for 40 key on-device AI hardware and software providers.

- Detailed profiles of 31 key on-device AI hardware and software providers.

- Use case descriptions across the most important industry verticals.

- In-depth analysis of market trends and key developments.

The on-device AI market to reach US$ 30.6 billion in 2029

Internet of Things (IoT) is continually evolving and expanding into new domains. Among the most recent developments is the integration of artificial intelligence (AI) capabilities directly onto IoT devices to unlock a new generation of applications. Devices that integrate AI have numerous benefits over traditional rule-based or manually programmed methods, particularly for applications that require object detection, speech recognition, predictive maintenance, anomaly detection, dynamic resource optimisation and autonomous decision-making. Running AI algorithms directly on the device – known as edge AI or on-device AI – brings numerous advantages, such as real-time responsiveness, reduced data transfer, enhanced privacy and improved resilience. While cloud processing remains effective for many IoT use cases, a growing number of emerging use cases now demand the capabilities of on-device AI.

The market for on-device AI solutions is characterised by a high degree of heterogeneity in both technologies and applications, in contrast to cloud-based AI where the hardware is typically designed around predefined use cases and centralised infrastructure. Embedded AI processing can be architected in numerous ways depending on the end use case, and it can be integrated into an almost limitless range of devices across consumer, industrial and automotive domains. This leads to a differentiated market landscape, with unique design constraints, performance requirements and optimisation strategies. However, the overarching objective is typically the same for all vendors – to achieve the highest possible performance per watt for the intended use case.

Berg Insight has identified 40 key companies that shape the on-device AI landscape. The market can broadly be divided into two layers. The first encompasses hardware categories such as AI system-on-chips (SoCs) or system-on-modules (SoMs), AI accelerators and AI microcontroller units (MCUs), each optimised for different levels of performance, power efficiency and integration. AI SoCs typically integrate components such as general-purpose and specialised AI compute cores, on-chip memory and connectivity on a single chip, while SoMs extend this design by including external system memory, storage and interface components on a larger board, targeting more advanced use cases. AI accelerators are specialised chips or modules designed to enhance AI inference efficiency in existing systems, typically working alongside a separate host processor in embedded applications. AI MCUs serve lower-power devices by bringing neural network capabilities to sensors, wearables and IoT endpoints where energy efficiency and cost are most critical. The second layer consists of on-device AI platforms that combine hardware, software and developer tools to simplify model deployment and optimisation.

Over the past decade, the on-device AI market has been driven primarily by traditional machine learning use cases such as computer vision and anomaly detection, which have seen steady annual growth of around the 10 percent range. In recent years, the market has reached an inflexion point as emerging technologies and applications in generative AI, robotics and autonomous driving have opened up new dimensions of growth. These developments are expected to accelerate market growth and give rise to entirely new use cases and product categories. Berg Insight estimates that the revenue generated by on-device AI solutions reached US$ 10.1 billion in 2024, an increase of around 22 percent from 2023. This figure includes AI SoCs/SoMs, AI accelerators, AI MCUs and specialised on-device AI software and platforms, but excludes revenues generated by non-IoT applications such as smartphones, tablets and personal computers. The market is expected to grow to US$ 30.6 billion in 2029, representing a compound annual growth rate (CAGR) of 25 percent.