The Telecare Market in Europe and North America - 2nd Edition

| 出版 | Berg Insight |

| 出版年月 | 2026年02月 |

| ページ数 | 180 |

| 図表数 | 61 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | EUR 1,800 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-15015 |

Berg Insight(ベルグインサイト)「欧州と北米のテレケア市場 第2版 – The Telecare Market in Europe and North America – 2nd Edition」はテレケアソリューションの欧州・北米市場を調査・分析しています。

主な掲載内容

- 慢性疾患の課題

- メディカルアラートとテレケアソリューション

- フォームファクタ

- モニタリングサービス

- ユースケース

- 医療介護供給(ケアデリバリ―)の取り組み

- 欧州のテレケアシステム

- 市場概観

- ソリューション提供会社

- 北米のメディカルアラート

- 市場概観

- ソリューション提供会社

- 市場予測と結論

- 市場動向

- 市場予測

- 欧州

- 北米

- メディカルアラートとテレケアソリューション

Report Overview

The Telecare Market in Europe and North America is a new report from Berg Insight that gives first-hand insights into the adoption of telecare solutions also known as medical alert systems or PERS (personal emergency response systems). This strategic research report from Berg Insight provides you with 180 pages of unique business intelligence including 5-year industry forecasts and expert commentary on which to base your business decisions.

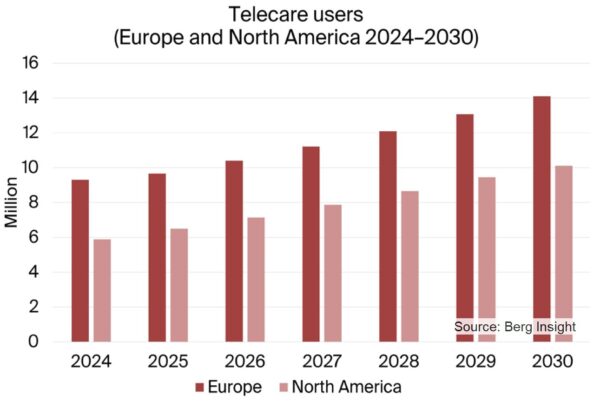

How should the mobile industry address the vast business opportunity in the telecare market? Berg Insight estimates that the user base of telecare (medical alert) systems in Europe and North America was 16.2 million at the end of 2025. The user base in the two regions is estimated to grow at a CAGR of 8.4 percent to reach more than 24.2 million users at the end of 2030. These solutions are available in both the stationary in-home form factor as well as mobile solutions for the use case when away from home. Learn more about how wireless technology can become seamlessly integrated with these devices in this 180-page in-depth report.

This report will allow you to:

- Profit from numerous executive interviews with market leading companies.

- Learn about the latest developments in telecare devices and services.

- Study the strategies of 69 key players in the telecare industry.

- Understand the market dynamics of the healthcare and social care systems in both regions.

- Evaluate the business opportunities in the fast-growing mobile telecare device segment.

- Benefit from expert market analysis including detailed market forecasts lasting until 2030.

- Predict future market and technology developments.

The number of telecare users in Europe and North America reached 16.2 million in 2025

In this digital era, artificial intelligence and generative technologies are transforming the tools and platforms for diagnosis, treatment and patient engagement. The rapid adoption and integration of digital technologies in healthcare have resulted in promising solutions to solve some of the challenges posed by the ageing population and strained healthcare systems. Berg Insight’s definition of telecare solutions, also known as medical alert systems or PERS (personal emergency response systems), is a service that enables elderly, disabled and vulnerable people to seek help from home in the event of an emergency. These solutions can trigger an alarm either when the user presses a button or when sensors detect activity that deviates from normal patterns. PERS systems provide continuous in-home or completely mobile monitoring services and can consist of a range of electronic devices such as personal alarm buttons, motion detectors, GPS monitors, fitness wearables, smartphones with built-in emergency features and radar-based technologies capable of detecting falls or unusual movements without requiring the user to wear a device. The market is evolving to include AI-driven capabilities that can automatically trigger an alarm in situations such as when a user leaves home at an unusual time or forgets to take his or her medication. AI-enabled systems can also detect unusual inactivity, recognise fall patterns using radar or motion sensors, identify distress through voice analysis or flag behavioural changes that indicate increased risk.

Berg Insight estimates that the user base of telecare solutions in the European market was around 9.7 million at the end of 2025. In Europe, the user base is estimated to grow at a CAGR of 7.8 percent to reach more than 14.1 million users at the end of 2030. The market value of telecare solutions reached € 3.9 billion in 2025. The market value is expected to grow at a CAGR of 7.6 percent in the next five years to reach € 5.6 billion at the end of the forecast period. Leading vendors active on the European telecare market include Tunstall, Legrand, TeleAlarm (Assa Abloy), Careium, and Chubb. Tunstall, Legrand and TeleAlarm have strong presence across the European region. Careium is a leading market player in the Nordic region and also has strong presence in the UK. Chubb Community Care has a strong footprint in the UK market.

Companies such as Assa Abloy, Ascom, Attentive (Solem), Beghelli, Chiptech, Climax Technology, Essence Group, MiniFinder, Navigil (Twig Com), Nobi and Telecom Design are key telecare equipment vendors. Enovation (Legrand Care), Skyresponse and Azur Soft are the leading providers of telecare monitoring software solutions. Additional vendors active across the European telecare ecosystem, covering platform software providers, service operators and connected device specialists include 2iC-Care, Access Group, Everon, Genus Care, Just Checking, Libify, Sensio, SmartLife Care, Tellu, Telegrafik, Urmet and Vivago.

The North American medical alert solution market is estimated to grow from 6.5 million users at the end of 2025 to 10.1 million users at the end of 2030. The penetration of medical alert services in the North American region now corresponds to 9.1 percent of the region’s population at the age of 65 years or older. The market value for medical alert solutions in North America reached € 3.4 billion (US$ 3.7 billion) in 2025. The market value is forecasted to grow to € 5.1 billion (US$ 5.6 billion) by 2030.

The North American medical alert market is served by a broad range of companies providing hardware devices, software platforms and monitoring services. Some companies offer integrated and platform-led solutions that combine hardware, software and monitoring capabilities into a unified offering. Key examples include Aloe Care Health, Becklar Personal Health & Safety, Connect America, Life Alert Emergency Response, Lively, LogicMark, Mytrex, Medical Guardian and QMedic. Another group consists of monitoring-led service providers that bundle monitoring subscriptions with branded or third-party medical alert equipment focusing on monitoring operations and service delivery. Examples are ADT, Alert1, Bay Alarm Medical and ModivCare. The market includes specialised equipment vendors that design and manufacture medical alert hardware and sensing technologies such as Climax Technology, Essence Group, Numera (Malar Company) and Vayyar Imaging.

The European and North American market for Personal Emergency Response Systems (PERS) is supported by several trends and developments that will have an impact on the competitive landscape during the forecast period. The silver generation is quickly becoming technologically savvy and open to adopting technology to help in everyday living needs. The deployment of telecare services enables proactive care that support timely interventions, reducing avoidable hospital admissions while maintaining independence for individuals in their own homes. Based on the solution, monitoring can be taken care of by family care providers, municipalities or professional 24/7 monitoring providers. AI-based solutions have an increasing role in the development of preventive and predictive care models. Solution providers have integrated AI and ML algorithms to analyse the monitoring data to learn about the patient’s routine, identify irregularities and expedite the needed assistance. Predictive analytics models support proactive care by assessing a user’s risk of falling based on historical data and health conditions. The industry is becoming more patient-centric which calls for integrated systems and improved interoperability of connected care solutions. Technology enabled care is a cost-effective solution for monitoring the health of elderly and the vulnerable population offering continuous monitoring. Finally, a convergence between medical alert and remote patient monitoring solutions can be observed as new, integrated and more holistic care solutions emerge.

Table of Contents

Executive Summary

1 The Challenge of Chronic Diseases

1.1 Introduction

1.1.1 The ageing population

1.1.2 Transformation in healthcare

1.2 Neurological disorders, mental disorders and physical disabilities

1.2.1 Autism spectrum disorders

1.2.2 Dementia

1.2.3 Epilepsy

1.2.4 Other disorders and disabilities

1.3 Healthcare systems

1.3.1 Healthcare in Europe

1.3.2 Healthcare in North America

1.4 Long-term social care systems

1.4.1 Social care in Europe

1.4.2 Social care in North America

1.5 The regulatory environment

1.5.1 Regulatory environment in Europe

1.5.2 Regulatory environment in North America

1.5.3 Medical data regulations

1.5.4 Standardisation

2 Medical Alert and Telecare Solutions

2.1 Form factors

2.1.1 In-home telecare or PERS solutions

2.1.2 Mobile telecare or mPERS solutions

2.2 Monitoring services

2.2.1 Alarm Receiving Centres (ARCs) and monitoring centres

2.2.2 Private caregivers

2.3 Use cases

2.3.1 Activity monitoring solutions

2.3.2 Fall detection

2.3.3 Sleep monitoring

2.3.4 Wandering detection

2.4 Care delivery approaches

2.4.1 Reactive care

2.4.2 Proactive care

2.4.3 Personalised care

2.4.4 Predictive care

3 Telecare Systems in Europe

3.1 Market overview

3.1.1 Value chain

3.1.2 Competitive landscape

3.2 Solution providers

3.2.1 2iC-Care

3.2.2 Althea Group

3.2.3 Amparo Technologies

3.2.4 Appello

3.2.5 Assa Abloy

3.2.6 Attentive (Solem)

3.2.7 Azur Soft

3.2.8 Beghelli (Group Gewiss)

3.2.9 Buddi (Big Technologies)

3.2.10 Careium

3.2.11 Caru

3.2.12 Chiptech

3.2.13 Chubb Community Care (APi Group)

3.2.14 Enovation (Legrand Care)

3.2.15 Essence Group

3.2.16 Eurocross Assistance

3.2.17 Everon Group

3.2.18 Genus Care

3.2.19 Hobacare

3.2.20 James TeleCare (iLogs Healthcare)

3.2.21 Just Checking

3.2.22 Legrand Care

3.2.23 Libify Technologies

3.2.24 Limmex

3.2.25 MiniFinder

3.2.26 Navigil (Twig Com)

3.2.27 Nobi

3.2.28 Posifon

3.2.29 Sensio

3.2.30 Sensorem

3.2.31 Skyresponse

3.2.32 SmartLife Care

3.2.33 TeleAlarm Group (Assa Abloy)

3.2.34 Telecom Design

3.2.35 Telegrafik

3.2.36 Tellu

3.2.37 The Access Group

3.2.38 Tunstall Healthcare Group

3.2.39 Urmet ATE

3.2.40 Vitakt Hausnotruf

3.2.41 Vivago

3.2.42 VIVAI Software

3.2.43 Zembro

4 Medical Alert Systems in North America

4.1 Market overview

4.1.1 Value chain

4.1.2 Competitive landscape

4.2 Solution providers

4.2.1 ADT Corporation

4.2.2 Alert1

4.2.3 Aloe Care Health

4.2.4 Bay Alarm Medical

4.2.5 Becklar Personal Health & Safety

4.2.6 Cherish Health

4.2.7 Climax Technology

4.2.8 Connect America

4.2.9 HandsFree Health (Quarvis Health)

4.2.10 Laipac Technology

4.2.11 Life Alert Emergency Response

4.2.12 LifeStation

4.2.13 Lively (Best Buy Health)

4.2.14 LogicMark

4.2.15 Medical Guardian

4.2.16 MetAlert (GTX Corp)

4.2.17 MobileHelp (Medical Guardian)

4.2.18 ModivCare

4.2.19 Mytrex

4.2.20 NtelCare

4.2.21 Numera (Malar Group)

4.2.22 Pontosense

4.2.23 QMedic

4.2.24 SecuraTrac

4.2.25 UnaliWear

4.2.26 Vayyar Imaging

5 Market Forecasts and Conclusions

5.1 Market trends

5.1.1 Staffing shortages driving the need for digital transformation

5.1.2 A growing market and new entrants lead to a changing market landscape

5.1.3 Changing demographics to drive the adoption of telecare solutions

5.1.4 Technology enabled care enables elderly to age at home for longer

5.1.5 Digital transformation is supported by increased connectivity

5.1.6 Evolving consumer behaviour and interest

5.1.7 PSTN Switch off continues to drive the transition towards IP-based telecare

5.1.8 The sunsets of 2G/3G cellular networks have driven launches of 4G devices

5.1.9 The digital shift enables new services and use cases

5.1.10 Convergence between telecare, telehealth and remote patient monitoring

5.1.11 The use of mobile telecare solutions is growing

5.1.12 A slow awakening consumer market for telecare in Europe

5.1.13 The beginning of AI integration marks a shift towards smarter healthcare

5.1.14 Advancing hybrid care models with digital tools and data-driven solutions

5.2 Market forecasts

5.2.1 Europe

5.2.2 North America

5.3 Revenue forecasts

5.3.1 Europe

5.3.2 North America

Glossary

List of Figures

Figure 1.1: Population by age group and region ……………….. 5

Figure 1.2: Share of the population covered by private health insurance (2024) ……. 10

Figure 1.3: Total health expenditure per capita by country (2024) ………… 12

Figure 1.4: Total and per capita healthcare expenditure by country (2023) ……… 15

Figure 1.5: Total and per capita healthcare expenditure by country (North America 2024) … 15

Figure 1.6: Healthcare spending by type of service and product (Canada 2024) …… 16

Figure 1.7: Health insurance coverage by type of insurance (US 2024) ……… 18

Figure 1.8: Healthcare spending by type of service and product (US 2023) ……….. 19

Figure 1.9: Long-term care as share of total healthcare spending (Europe 2022) …… 20

Figure 1.10: Gross expenditure on long term care by support setting (England 2023–2024) … 22

Figure 2.1: Vayyar care monitoring sensor ………………… 34

Figure 2.2: Tunstall Lifeline Smart Hub telecare device…………….. 35

Figure 2.3: Examples of mobile telecare devices ……………….. 36

Figure 2.4: Care@Home activity monitoring solution ……………….. 38

Figure 3.1: Number of telecare systems by form factor (EU 27+3 2025) ………. 43

Figure 3.2: Adoption of telecare services per country (EU 27+3 2025) ………. 44

Figure 3.3: Leading providers of telecare services in France (2025) ………… 47

Figure 3.4: The telecare value chain ……………………. 49

Figure 3.5: Leading providers of telecare equipment (EU 27+3 2025) ……….. 51

Figure 3.6: Leading telecare solution providers per country (EU 27+3 2025) ……… 52

Figure 3.7: Overview of telecare solution providers (EU 27+3 2025) …………. 53

Figure 3.8: Andi by 2iC-Care ………………………. 55

Figure 3.9: Vita Hub solution ………………………. 58

Figure 3.10: Attentive LUNA ……………………….. 64

Figure 3.11: Eliza smart care hub and Abby …………………. 68

Figure 3.12: Hobacare mPERS+ system ………………….. 82

Figure 3.13: James emergency watches ………………… 83

Figure 3.14: Legrand Care Novo Go and Dock ……………….. 86

Figure 3.15: Limmex Emergency Watch …………………. 88

Figure 3.16: MiniFinder Nano and MiniFinder Pico ……………….. 89

Figure 3.17: The Navigil 580 wristwatch …………………. 91

Figure 3.18: The Nobi lights ……………………….. 93

Figure 3.19: SmartLife Care’s telecare alarm system ……………… 101

Figure 3.20: TeleAlarm TA74 Carephone …………………. 103

Figure 3.21: Telecom Design Vibby Home …………………. 105

Figure 3.22: Vivago Care 8001 watch …………………… 116

Figure 3.23: VIVAI Home Hub ……………………… 118

Figure 3.24: Zembro’s Essentials Comfort, Essentials Mini and Wander Alert …… 119

Figure 4.1: Adoption of medical alert systems by country (North America 2025) …….. 122

Figure 4.2: Number of medical alert systems by form factor (North America 2025) ……. 122

Figure 4.3: The medical alert system value chain ……………… 123

Figure 4.4: Leading vendors of medical alert systems by shipments (North America 2025) … 124

Figure 4.5: Leading providers of medical alert services by users (North America 2025) … 125

Figure 4.6: Overview of medical alert system providers …………….. 126

Figure 4.7: Freeus Belle W, Belle S and Belle X devices ……………. 132

Figure 4.8: Cherish Serenity Enterprise Hub …………………. 133

Figure 4.9: The LooK watch I from Laipac Technology …………… 139

Figure 4.10: Lively Jitterbug Smart 4 and Lively Mobile2 All-in-one medical alert device ….. 141

Figure 4.11: LogicMark Freedom Alert Mini and Freedom Alert Max ………… 143

Figure 4.12: GPS SmartSole by MetAlert …………………. 147

Figure 4.13: The MXD-LTE from Mytrex ………………… 151

Figure 4.14: QMedic’s in-home medical alert system……………… 156

Figure 4.15: Vayyar Care monitoring sensor …………………. 159

Figure 5.1: Elderly population (65+) as a percentage of total population, (Global 2025) …. 166

Figure 5.2: Elderly fall-related deaths (USA 2018–2023) ……………. 168

Figure 5.3: Telecare users by region (Europe and North America 2024–2030) …….. 177

Figure 5.4: Telecare system users by segment (EU 27+3 2024–2030) ……….. 178

Figure 5.5: Medical alert system users by segment (North America 2024–2030) …….. 179

Figure 5.6: Telecare system revenues (Europe and North America 2024–2030) …… 180

Figure 5.7: Telecare market value by segment (Europe 2024–2030) ………… 180

Figure 5.8: Medical alert system market value by segment (North America 2024–2030) ….. 181