The Future of Electric Aircraft and eVTOLs - 2nd Edition

| 出版 | Berg Insight |

| 出版年月 | 2026年01月 |

| ページ数 | 170 |

| 図表数 | 82 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | EUR 1,500 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14198 |

「電動飛行機とeVTOLの今後 第2版」は航空業界の電動化に関する最新の動向を分析したBerg Insight社の市場調査レポートです。この戦略調査レポートは170ページにわたり、独自のビジネスインテリジェンスを提供し、25年間の業界予測、専門家の解説、そしてビジネス上の意思決定の根拠となる実例をカバーしています。またベンダー、技術開発、規制、市場に関する最新情報も掲載しています。

電動航空機とeVTOLの市場は、今後25年間でどのように進化するのでしょうか?Berg Insightは2021年から2050年のまでの期間で電動航空機とeVTOL(商用および自家用)の市場規模が1,000億~3,000億ユーロに達すると予測しています。

レポートのハイライト

- 市場をリードする企業幹部への多数のインタビューから得られた知見

- 電動航空機およびeVTOLのバリューチェーンと主要なユースケースの包括的な説明

- 必要な地上インフラと空域におけるeVTOLへの対応を分析

- 市場動向と主要開発動向の詳細な分析

- 電動航空機、eVTOL、電気推進システムメーカー42社の企業情報

- 認証プロセスと安全上の懸念事項への対応についての簡潔な解説

- 2050年までの市場予測とシナリオ分析

主な掲載内容

- 概説

- 電動航空機とeVTOL

- 電動航空機

- eVTOL

- eVTOLのリスク評価

- 技術概観

- 電池型電動

- 水素電動

- ハイブリッド電動

- 機体

- 通信技術と自律飛行

- エコシステムと法規制フレームワーク

- 地域エアモビリティとアーバンエアモビリティ

- 企業情報と戦略

- eVTOL

- 電動飛行機

- 電気推進システム

- 市場予測とシナリオ

- 市場分類

- 市場規模

- 市場価値

- ビジネスモデルとユースケース

- まとめ

Report Overview

The Future of Electric Aircraft and eVTOLs is a new report from Berg Insight analysing the latest developments on the electrification in aviation. This strategic research report from Berg Insight provides you with 170 pages of unique business intelligence, including 25-year industry forecasts, expert commentary and real-life case studies on which to base your business decisions.

How will the market for electric aircraft and eVTOLs evolve in the next 25 years? The total market value of electric aircraft and eVTOLs (commercial and private use) during the time period 2021–2050 is forecasted to reach in the range of € 100–300 billion. Get up to date with the latest information about vendors, technology developments, regulations and markets.

Highlights from the report:

- Insights from numerous executive interviews with market leading companies.

- Comprehensive description of the electric aircraft and eVTOL value chain and key use cases.

- Analysis of the ground infrastructure needed and how eVTOLs will be handled in the airspace.

- In-depth analysis of market trends and key developments.

- Profiles of 42 electric aircraft, eVTOL and electric propulsion system manufacturers.

- Summary of the certification process and handling of safety concerns.

- Market forecasts and scenario analysis lasting until 2050.

The electric aircraft and eVTOL market is set for long-term growth

There are many large-scale industrial projects worldwide aimed at developing electric aircraft and eVTOLs. At the same time, the electrification of the aviation industry represents a challenge as the industry is heavily regulated and strongly committed to safe operations and redundant systems. Electric aircraft and eVTOLs will enable new connectivity within large urban areas, between cities, from rural regions to cities and between rural areas. There are many suitable use cases ranging from passenger transportation to cargo transport, surveillance, healthcare and firefighting. Some electric aircraft and eVTOL projects have been paused or discontinued in recent years. Despite this, other actors are progressing towards certification and market entry.

More than a thousand eVTOL design concepts have been introduced worldwide. Some companies focus on one or two-seat eVTOLs for private use, while others develop larger aircraft for commercial use cases such as air taxi services. Many of the commercial eVTOLs are large vehicles with wingspans of 10–15 metres, which need to be considered when developing ground infrastructure as well as working with city planning, passenger processing and safety issues. Some eVTOLs are also intended to fly autonomously without a pilot. Examples of commercial eVTOL vendors include Aerofugia, Archer, Beta Technologies, EHang, Eve Air Mobility, Joby Aviation, Volocopter, Vertical Aerospace and Wisk. Companies developing eVTOLs for personal mobility include AIR, Aridge, Jetson, LEO Flight, Pivotal and Skyfly.

There are also several companies working on electric and hybrid-electric aircraft. The market is characterised by having both established aviation companies developing vehicles and solutions as well as start-ups and tech companies doing the same thing. These companies address the challenge in different ways, leading to several possible solutions and design pathways. Examples of battery-electric aircraft vendors include Beta Technologies, Bye Aerospace, Cosmic Aerospace, Electron Aerospace, Elysian, MD Aircraft, Pipistrel and Vaeridion. Companies focusing on hybrid-electric aircraft include Electra, Heart Aerospace, Maeve Aerospace and VoltAero.

In addition, several companies develop powertrain solutions for battery-electric, hydrogen-electric and hybrid-electric aircraft and eVTOLs. Most actors in this segment produce a complete setup of electric propulsion systems comprising electric motors, energy storage solutions and related components. Electric propulsion systems can be used in both newly developed aircraft and retrofitted in existing aircraft. Examples of companies in this segment include Ampaire, Evolito, MagniX, Safran and ZeroAvia.

Before 2030 we will see some of the first piloted eVTOLs in commercial use. Between 2036–2040 the ecosystem and acceptance will develop and we might see around 7,500 vehicles being delivered globally. Fewer if costs are high and certification is taking longer than anticipated. In the high scenario we see that the total number of deliveries could reach approximately 45,000 vehicles between 2026–2050. The high scenario is based on a favourable regulatory environment where the long-term airspace management has been solved as well as the approval for autonomous flights.

The private eVTOL market can be potentially much larger than the commercial market in terms of the number of vehicles. The first eVTOLs for private use have already been delivered. Under favourable conditions in the high scenario, the total market might reach almost 100,000 vehicles delivered by 2050. Most of these will be small one or two-seaters and the majority of them will be delivered in the latter part of the forecast period. These vehicles will need advanced avionics, connectivity, and avoid and detect technology but at the same time need to be cost-efficient solutions.

Electric aircraft will vary considerably in size and performance and will be powered by either batteries, hydrogen or hybrid-electric propulsion. The forecast is based on three market segments: battery-electric aircraft with one to four passenger seats; aircraft with five to nine passenger seats powered by battery, hydrogen or hybrid-electric propulsion; and aircraft with ten or more passenger seats powered by battery, hydrogen or hybrid-electric propulsion. For all segments, we estimate total shipments of around 10,000 aircraft between 2026–2050 in the high scenario. The first battery-electric aircraft models with one to four passenger seats have been certified and shipped. Due to the complex certification pathway and the dependence of new ground and charging infrastructure, we forecast that only a few hundred aircraft will be delivered before 2030. Some of the addressable market for electric aircraft is based on the replacement of the current fleet of small-sized aircraft. This is however a comparatively small market. It is also a new market for regional air mobility which will take some time to develop. It will take time to build production capacity and solve ground infrastructure challenges, but with more efficient drivetrains the use case and economics look reasonably favourable in the longer term.

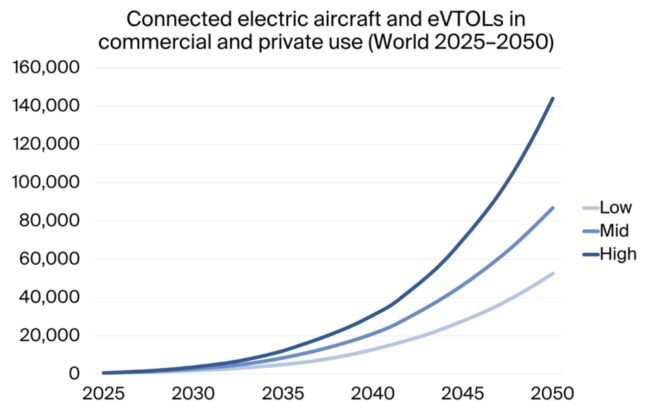

Electric aircraft and eVTOLs will need advanced connectivity. There is also a market for different kinds of autonomous vehicle technology solutions which will need to be incorporated in the vehicles. Cellular connectivity is one of the prominent technologies available to support the use cases in urban areas. Satellite systems can also complement the ground-based architectures, particularly the LEO (Low Earth Orbit) satellite constellations. The number of connected electric aircraft and eVTOLs will take off from 2035 and then increase steadily. We estimate around 10,000 connected vehicles for passenger use by 2035 and around 60,000–140,000 in 2050.

Table of Contents

Executive Summary

1 Introduction

1.1 The aviation market

1.2 The concept of electric aviation

1.3 Drivers behind the electrification of aircraft and eVTOLs

1.3.1 Reduced costs

1.3.2 Regional travel market

1.3.3 Emissions reductions

1.3.4 Noise reductions

1.3.5 Increased accessibility

1.3.6 Economic development

2 Electric Aircraft and eVTOLs

2.1 Electric aircraft

2.1.1 Retrofit

2.1.2 Traditional design

2.1.3 New design

2.1.4 Size versus range

2.1.5 Battery-electric, hydrogen-electric versus hybrid-electric aircraft

2.2 eVTOLs

2.2.1 Wingless multicopter

2.2.2 Lift-and-cruise (fixed wing)

2.2.3 Tilted wing and/or propellers

2.3 Risk assessment regarding eVTOLs

2.3.1 Certification

2.3.2 Infrastructure

2.3.3 Technology

2.3.4 Operations

2.3.5 Public awareness

3 Technology Overview

3.1 Battery-electric

3.2 Hydrogen-electric

3.3 Hybrid-electric

3.4 Airframes

3.5 Communications technology and autonomous flight

3.5.1 Navigation and communications systems

3.5.2 IoT connectivity

3.5.3 A possible pathway to autonomous flights

4 Ecosystem and Regulatory Framework

4.1 Ecosystem

4.1.1 Charging

4.1.2 Battery power challenges

4.1.3 Hydrogen power challenges

4.1.4 Take-off and landing infrastructure – vertiports

4.1.5 Airport infrastructure

4.1.6 MRO

4.2 Regulatory framework

4.2.1 Certification and standardisation

4.2.2 Safety

4.2.3 Airspace management

4.2.4 Sustainability

5 Regional and Urban Air Mobility

5.1 Regional Air Mobility – possible market development and use cases

5.1.1 How will the RAM market evolve – different scenarios

5.1.2 User experience

5.2 Urban Air Mobility – possible market development and use cases

5.2.1 How will the UAM market evolve – different scenarios

5.2.2 User experience

5.3 Implications for regional and city planning

5.3.1 Education

5.3.2 Permits

5.3.3 Short-term city planning

5.3.4 Long-term city planning

5.3.5 Regional planning

5.3.6 Transport planning and integration

6 Company Profiles and Strategies

6.1 eVTOLs

6.1.1 Aerofugia

6.1.2 AIR

6.1.3 Archer

6.1.4 Aridge (XPeng AeroHT)

6.1.5 AutoFlight

6.1.6 CityAirbus NextGen

6.1.7 EHang

6.1.8 Eve Air Mobility

6.1.9 Horizon Aircraft

6.1.10 Jetson

6.1.11 Joby Aviation

6.1.12 LEO Flight

6.1.13 Lilium

6.1.14 Pivotal

6.1.15 Sambo Motors

6.1.16 SkyDrive

6.1.17 Skyfly

6.1.18 Supernal

6.1.19 V-Space

6.1.20 Vertical Aerospace

6.1.21 Volocopter

6.1.22 Wisk

6.2 Electric aircraft

6.2.1 Beta Technologies

6.2.2 Bye Aerospace

6.2.3 Cosmic Aerospace

6.2.4 Electra

6.2.5 Electron Aerospace

6.2.6 Elysian

6.2.7 Eviation Aircraft

6.2.8 Heart Aerospace

6.2.9 Maeve Aerospace

6.2.10 MD Aircraft

6.2.11 Pipistrel

6.2.12 Vaeridion

6.2.13 VoltAero

6.3 Electric propulsion systems

6.3.1 Ampaire

6.3.2 Evolito

6.3.3 H55

6.3.4 MagniX

6.3.5 Safran

6.3.6 Wright Electric

6.3.7 ZeroAvia

7 Market Forecasts and Scenarios

7.1 Market segmentation

7.2 Market size

7.2.1 Commercial eVTOLs

7.2.2 Privately owned eVTOLs

7.2.3 Battery-electric aircraft with 1–4 passenger seats

7.2.4 Battery, hydrogen and hybrid-electric aircraft with 5–9 passenger seats

7.2.5 Battery, hydrogen and hybrid-electric aircraft with 10 or more passenger seats

7.2.6 The current non-binding and firm order stock of electric aircraft and eVTOLs

7.2.7 IoT connectivity

7.3 Market value

7.3.1 Market value of eVTOLs

7.3.2 Market value of electric aircraft

7.4 Business models and use cases

7.5 Concluding remarks

Glossary

List of Figures

Figure 1.1: IATA strategy towards net zero ………….. 7

Figure 2.1: Example of a retrofit design ………….. 14

Figure 2.2: Example of a traditional design ………….. 14

Figure 2.3: Example of a new design …………… 15

Figure 2.4: Linear and nodal transportation networks …………. 19

Figure 2.5: Example of wingless multicopter design ………… 20

Figure 2.6: Example of lift-and-cruise design ………….. 21

Figure 2.7: Example of tilted propeller design …………. 21

Figure 3.1: Schematic of the main propulsion technologies ………… 27

Figure 3.2: Schematic of energy efficiency for electric and fuel cell propulsion …… 28

Figure 4.1: The ecosystem of advanced air mobility ………… 43

Figure 4.2: Examples of vertiport designs ……………. 49

Figure 4.3: Commercial certification of electric aircraft (forecast) ………. 56

Figure 4.4: Commercial certification of piloted eVTOLs (forecast) ……… 58

Figure 4.5: Sensor technologies to be used for eVTOLs ………… 62

Figure 4.6: eVTOL control centre ……………… 68

Figure 5.1: Potential market for different aircraft types ………… 73

Figure 5.2: Commercial implementation steps ………… 78

Figure 5.3: Examples of potential eVTOL use cases ………… 80

Figure 6.1: The number of global eVTOL concepts ………….. 87

Figure 6.2: Aerofugia – AE200-100 specifications …………. 89

Figure 6.3: AIR – AIR One for personal use specifications ………… 90

Figure 6.4: A prototype of AIR’s two-seat eVTOL for personal use …….. 91

Figure 6.5: Archer – Midnight specifications ……………. 92

Figure 6.6: Aridge’s Land Aircraft Carrier comprising a land vehicle and an eVTOL ….. 94

Figure 6.7: AutoFlight – V2000EM Prosperity specifications ………… 95

Figure 6.8: EHang – EH216-S and VT35 specifications ……….. 98

Figure 6.9: Eve Air Mobility – Eve-100 specifications ………… 100

Figure 6.10: Horizon Aircraft – Cavorite X7 specifications ……….. 102

Figure 6.11: Horizon Aircraft’s hybrid-electric VTOL with a fan-in-wing design…… 103

Figure 6.12: Jetson – Jetson ONE specifications ………… 104

Figure 6.13: Joby – S4 specifications …………… 105

Figure 6.14: LEO Flight – JetBike specifications ………….. 107

Figure 6.15: Pivotal – Helix specifications …………… 109

Figure 6.16: Pivotal’s Helix one-seat eVTOL for personal use …….. 110

Figure 6.17: Sambo Motors – B-33x specifications ………… 111

Figure 6.18: SkyDrive – SD-05 specifications ………… 112

Figure 6.19: Skyfly – Axe specifications …………… 113

Figure 6.20: Supernal – S-A2 specifications ………….. 115

Figure 6.21: V-Space – VS-210, VS-300 and VS-500 specifications …….. 116

Figure 6.22: Vertical Aerospace – Valo specifications ……….. 117

Figure 6.23: Vertical Aerospace’s Valo eVTOL with four passenger seats ……. 118

Figure 6.24: Volocopter – VoloCity and VoloXPro specifications ……… 119

Figure 6.25: Wisk – Generation 6 specifications ………….. 121

Figure 6.26: Beta Technologies – Alia CX300 CTOL specifications …….. 123

Figure 6.27: Beta Technologies – Alia A250 VTOL specifications …….. 123

Figure 6.28: Beta Technologies – H500A and V600A electric engine specifications … 124

Figure 6.29: Beta Technologies’ A250 VTOL in the front and two AX300 CTOLs in the back . 125

Figure 6.30: Bye Aerospace – eFlyer 2 specifications ……….. 126

Figure 6.31: Bye Aerospace’s two-seat electric aircraft ………… 127

Figure 6.32: Electra – EL9 specifications ……………. 129

Figure 6.33: Electra’s EL9 hybrid-electric aircraft with nine passenger seats ….. 130

Figure 6.34: Electron Aerospace – Electron 5 specifications ……… 131

Figure 6.35: Eviation Aircraft – Alice specifications…………. 133

Figure 6.36: Heart Aerospace – ES-30 specifications ………… 134

Figure 6.37: Maeve Aerospace – MJ500 specifications ………… 136

Figure 6.38: Maeve Aerospace’s MJ500 hybrid-electric regional aircraft …… 136

Figure 6.39: MD Aircraft – MDA1 eViator specifications ……….. 137

Figure 6.40: Pipistrel – Velis Electro specifications …………. 139

Figure 6.41: Pipistrel’s Velis Electro aircraft with two seats ………… 140

Figure 6.42: Vaeridion – Microliner specifications ………….. 141

Figure 6.43: VoltAero – Cassio 330 specifications ………….. 143

Figure 6.44: Evolito – Electric motor specifications ………… 145

Figure 6.45: MagniX – EPUs and battery specifications ……….. 147

Figure 6.46: Safran – Electric engine specifications ……….. 149

Figure 6.47: ZeroAvia – Hydrogen-electric powertrain specifications …….. 151

Figure 7.1: Electric passenger aircraft timeline …………. 156

Figure 7.2: Passenger eVTOL timeline ………….. 157

Figure 7.3: Shipments of commercial eVTOLs (2021–2050) ………. 159

Figure 7.4: Shipments of privately owned eVTOLs (2021–2050) ………. 160

Figure 7.5: Shipments of electric aircraft with 1–4 passenger seats (2021–2050) …. 161

Figure 7.6: Shipments of electric aircraft with 5–9 passenger seats (2021–2050) …. 162

Figure 7.7: Shipments of electric aircraft with 10 or more passenger seats (2021–2050) …. 163

Figure 7.8: Connected vehicles in commercial and private use (World 2025–2050) … 165

Figure 7.9: Commercial eVTOL market value (2021–2050) ………… 166

Figure 7.10: Private eVTOL market value (2021–2050) ………… 167

Figure 7.11: Market value of electric aircraft with 1–4 passenger seats (2021–2050) ….. 168

Figure 7.12: Market value of electric aircraft with 5–9 passenger seats (2021–2050) ….. 168

Figure 7.13: Market value of electric aircraft with 10 or more passenger seats (2021–2050) .. 169

Figure 7.14: Use case: eVTOL vertiport in a small city ………. 170

Figure 7.15: Use case: eVTOL vertiport in a dense urban area ……… 170

Figure 7.16: Use case: Regional airport/airfield – an initial scenario ……. 171