Chemical Mechanical Planarization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Chemical Mechanical Planarization Market Report is Segmented by Product Type (CMP Equipment, CMP Consumables), Application (Integrated Circuit, Compound Semiconductor, MEMS and NEMS, Advanced Packaging, Other Applications), End-User (Foundries, Idms, OSAT, R&D Institutes/Universities), and Geography (North America, Europe, Asia Pacific, Rest of World).

化学機械平坦化市場レポートは、製品タイプ (CMP 装置、CMP 消耗品)、アプリケーション (集積回路、複合半導体、MEMS および NEMS、高度なパッケージング、その他のアプリケーション)、エンドユーザー (ファウンドリ、IDMS、OSAT、R&D 機関/大学)、および地域 (北米、ヨーロッパ、アジア太平洋、その他の世界) 別にセグメント化されています。

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 120 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14875 |

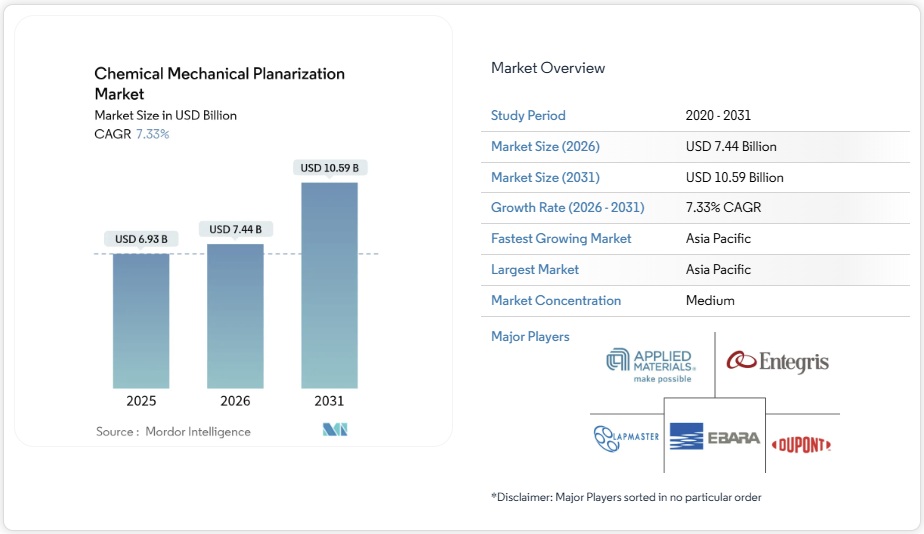

2026年の化学機械平坦化(CMP)市場規模は74億4,000万米ドルと推定され、2025年の69億3,000万米ドルから拡大しています。2031年には105億9,000万米ドルに達すると予測されており、2026年から2031年にかけて年平均成長率(CAGR)7.33%で成長します。成長の原動力は、FinFETからゲートオールアラウンド(GAA)トランジスタへの移行、3Dインテグレーション、そしてパワーデバイスにおける炭化ケイ素(SiC)と窒化ガリウム(GaN)の使用増加です。ファウンドリは大規模な生産能力増強を継続しており、米国と欧州連合の政府インセンティブは、現地のCMPサプライチェーンを奨励しています。ツールの入手が逼迫しているため生産の増加が抑制されている一方で、持続可能性への取り組みにより、低研磨性および研磨剤フリーのスラリーの需要が加速しています。地政学的な輸出規制は、装置の流れを再編し、欧米と中国のベンダー間の並行したイノベーションを促進しています。

セグメント分析

- 2025年の化学機械平坦化(CMP)市場規模において、装置は62.78%を占めました。支出は、ウェーハ面内不均一性を1nm未満に抑え、パッド表面の健全性を保つための閉ループコンディショニングを統合したシングルウェーハ装置に集中しています。ファブがGAAプロセスとワイドバンドギャップ基板に対応する新しいプラットフォームを導入するにつれて、このセグメントは2031年まで7.54%のCAGRで成長すると予測されています。7nmノード未満のナノスケール欠陥を除去するため、洗浄モジュールも同時にアップグレードされます。

- 消耗品は売上高の37.22%を占め、安定した需要を確保するリカーリングスラリーがその牽引役となっています。シリカベースの誘電体スラリーが主流を占める一方、ニッチなセリア配合はガラスやサファイアの研磨に利用されています。パッドサプライヤーは、パッド寿命を延長しながらも安定した研磨率を維持し、欠陥を最小限に抑える溝付きポリマーブレンドをリリースしています。サステナビリティ目標の達成により、低研磨性ケミカルへの移行が加速しており、性能と環境指標が融合した際に、消耗品ベンダーはプレミアム価格を実現できる立場にあります。

- 化学機械平坦化(CMP)市場レポートは、製品タイプ (CMP 装置、CMP 消耗品)、アプリケーション (集積回路、複合半導体、MEMS および NEMS、高度なパッケージング、その他のアプリケーション)、エンドユーザー (ファウンドリ、IDMS、OSAT、R&D 機関/大学)、および地域 (北米、ヨーロッパ、アジア太平洋、その他の世界) 別にセグメント化されています。

Chemical Mechanical Planarization Market Analysis

Chemical mechanical planarization market size in 2026 is estimated at USD 7.44 billion, growing from 2025 value of USD 6.93 billion with 2031 projections showing USD 10.59 billion, growing at 7.33% CAGR over 2026-2031. Growth is propelled by the transition from FinFET to gate-all-around (GAA) transistors, 3D-integration, and the rising use of silicon carbide (SiC) and gallium nitride (GaN) in power devices. Foundries continue large-scale capacity additions, and government incentives in the United States and European Union encourage local CMP supply chains. Tight tool availability constrains production ramps, while sustainability initiatives accelerate demand for low-abrasive and abrasive-free slurries. Geopolitical export controls reshape equipment flows and spur parallel innovation tracks between Western and Chinese vendors.

Global Chemical Mechanical Planarization Market Trends and Insights

Accelerating GAA and 3D-IC adoption

Gate-all-around transistors alter CMP chemistries by introducing new metal gate stacks that require highly selective removal rates and tighter defectivity thresholds. Leading foundries have scheduled volume production of GAA nodes below 3 nm, driving an equipment refresh cycle for 300 mm single-wafer polishers with advanced endpoint control. Complementary 3D-integration techniques, such as through-silicon vias, demand ultra-flat copper layers across multiple wafer surfaces. CMP platforms, therefore, integrate closed-loop pad conditioning and real-time slurry monitoring to sustain yields at ever-smaller tolerances .

Rapid growth in SiC/GaN power devices

Silicon carbide and gallium nitride wafers exhibit hardness and chemical inertness that multiply polish times and consumable costs. Dedicated slurries using alkaline chemistries and engineered abrasives now achieve removal rates near 1 µm/h while holding surface roughness below 0.05 nm. Automotive electrification accelerates demand for these materials, prompting tool makers to release pad designs resilient to abrasive wear and cross-contamination shielding between SiC and traditional silicon lines.

Escalating slurry input costs

Cerium oxide, hydrogen peroxide, and other high-purity inputs show price spikes when rare-earth supply tightens or chemical plants undergo maintenance. The U.S. Geological Survey notes China remains the main source of rare-earth imports, leaving global slurry vendors exposed to trade disputes . Vendors respond by reformulating slurries with lower abrasive loads and recycling spent solutions through filtration loops.

Other drivers and restraints analyzed in the detailed report include:

- AI datacenter capital expenditure

- U.S. and EU fab incentives

- Tight OEM capacity for 300 mm tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment represented 62.78% of the chemical mechanical planarization market size in 2025. Spending concentrates on single-wafer tools that deliver within-wafer non-uniformity below 1 nm and integrate closed-loop conditioning for pad surface health. The segment is forecast to rise at a 7.54% CAGR to 2031 as fabs install new platforms that support GAA processes and wide-bandgap substrates. Cleaning modules undergo concurrent upgrades to remove nanoscale defects at sub-7 nm nodes.

Consumables account for 37.22% of revenue, led by slurries whose recurring nature ensures stable demand. Silica-based dielectric slurries dominate, while niche ceria formulas address glass and sapphire polishing. Pad suppliers release grooved polymer blends that sustain consistent removal rates and minimize defectivity over extended pad life. Sustainability goals accelerate the shift to low-abrasive chemistries, positioning consumables vendors for premium pricing when performance and environmental metrics converge.

The Chemical Mechanical Planarization Market Report is Segmented by Product Type (CMP Equipment, CMP Consumables), Application (Integrated Circuit, Compound Semiconductor, MEMS and NEMS, Advanced Packaging, Other Applications), End-User (Foundries, Idms, OSAT, R&D Institutes/Universities), and Geography (North America, Europe, Asia Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 64.12% of 2025 revenue and is projected to record an 8.41% CAGR through 2031. Mainland China’s localization push prompts aggressive wafer-fab construction, while Taiwan retains leadership in cutting-edge logic and advanced packaging. South Korea invests in high-layer count 3D NAND and DRAM, boosting demand for dielectric and metal planarization capacity. Japanese suppliers leverage decades-long expertise in ultrapure chemicals and precision pads, reinforcing the region’s vertically integrated ecosystem.

North America ranks second by revenue. Federal incentives have unlocked new fab commitments, and domestic equipment leaders capture significant orders as customers prioritize secure supply chains. Advanced packaging initiatives in Arizona and New York stimulate regional demand for CMP consumables that comply with local content rules. Export controls limit high-end pad shipments to China, creating a bifurcated market and heightening strategic value for North American CMP vendors.

Europe pursues 20% global semiconductor output by 2030, emphasizing manufacturing sustainability. Regional materials firms expand electronics-grade hydrogen peroxide and specialty slurry capacity, while equipment makers in Germany and the Netherlands align CMP offerings with EU environmental directives. Government funding supports pilot lines for heterogeneous integration, driving incremental CMP tool installations across research hubs and specialty foundries.

List of Companies Covered in this Report:

- Applied Materials Inc.

- Entegris Inc.

- EBARA Corporation

- Lapmaster Wolters GmbH

- DuPont de Nemours, Inc.

- Fujimi Incorporated

- Revasum Inc.

- Resonac Holdings Corporation

- Okamoto Corporation

- FUJIFILM Corporation

- Tokyo Seimitsu Co., Ltd.

- Lam Research Corporation

- KLA Corporation

- Hitachi High-Tech Corporation

- Cabot Microelectronics Corporation

- 3M Company

- Saint-Gobain Surface Conditioning

- BASF SE

- Nagase ChemteX Corporation

- Ace Nanochem Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents