4K Display Resolution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

4K ディスプレイ解像度市場レポートは、製品タイプ (スマート TV、モニター、スマートフォン、タブレットなど)、パネル技術 (LCD、OLED、ミニ LED、マイクロ LED)、画面サイズ (32 インチ未満、32 ~ 49 インチ、50 ~ 65 インチ、66 ~ 84 インチ、85 インチ以上)、エンドユーザー垂直 (民生用電子機器、ゲームおよび e スポーツ会場、ビジネスおよび教育など)、および地域別にセグメント化されています。

The 4K Display Resolution Market Report is Segmented by Product Type (Smart TV, Monitor, Smartphone, Tablet, and More), Panel Technology (LCD, OLED, Mini-LED, and Micro-LED), Screen Size (Sub 32 Inch, 32-49 Inch, 50-65 Inch, 66-84 Inch, and Above 85 Inch), End-User Vertical (Consumer Electronics, Gaming and Esports Venues, Business and Education, and More), and Geography.

| 出版 | Mordor Intelligence |

| 出版年月 | 2027年07月 |

| ページ数 | 120 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-12331 |

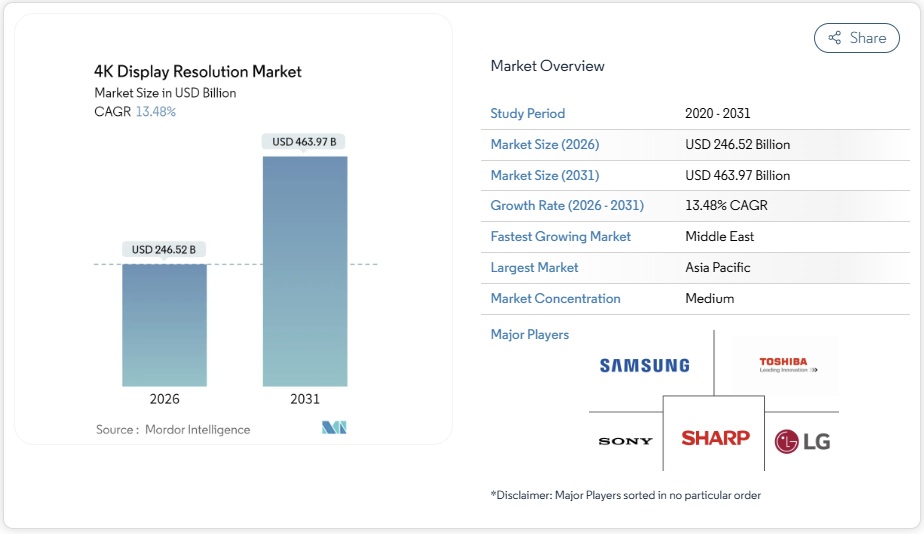

4Kディスプレイ解像度市場規模は、2025年には2,172.3億米ドルと推定され、2030年には4,125.7億米ドルに達し、年平均成長率(CAGR)13.69%で成長すると予測されています。パネルコストの急速な低下、ネイティブ4Kストリーミングコンテンツの充実、そして企業ユースケースの拡大により、この技術はプレミアム市場から一般普及へと移行しつつあります。アジア太平洋地域は製造規模の拡大により平均販売価格が低く抑えられている一方で、消費者は大画面を強く好みます。ハイブリッドワークの需要と没入型ゲームにより、買い替えサイクルがさらに短縮化しており、各ブランドはより特化したモデルを投入しています。同時に、チップセットをめぐるサプライチェーンリスクや欧州における省エネ規制の進化により、ベンダーは部品調達の多様化と低消費電力バックライトの研究開発の加速を迫られています。

セグメント分析

- ゲーミングモニターは、2025年から2030年にかけて年平均成長率(CAGR)14.1%と予測されており、4Kディスプレイ解像度市場の中で最も高い成長率となります。サムスンは2024年に世界シェア21.0%を維持し、OLEDサブセグメントにおける34.6%のシェアは、新興のQD-OLEDスタックにおける先行者利益を確定させました。このセグメントは、eスポーツのスポンサーシップによる認知度、頻繁なモデル更新、そして安定した4K/144Hzゲームプレイを可能にするNVIDIA GeForce RTX 4090などの強力なGPUとの相乗効果によって成長しています。モニターブランドは、プレミアムSKUを差別化するために、ピーク輝度の向上、タンデムOLEDレイヤー、DisplayPort 2.1入力などの仕様向上を図っています。熱心な購入者は応答速度、HDRコントラスト、色域を重視するため、収益性は主流のテレビよりも高いままです。

- スマートテレビは、幅広い4KストリーミングコンテンツライブラリとBOMコストの低下に支えられ、2024年も68%の収益シェアで市場を牽引しました。企業向けビデオウォールやデジタルサイネージは、ハイブリッドワークハブに広視野角と高画素密度が求められる中で、その重要性が高まりました。医療用ディスプレイは、ソニーのLMD-32M1MDなどの4K外科用モニターが手術室向けVESA HDR1000規格に準拠したことで、高利益率のニッチ市場を形成しました。ネイティブ4K対応のスマートフォンやタブレットは、消費電力がモバイルのメリットを相殺するため、クリエイター向けの用途に限定されています。全体として、より豊かなエンターテインメントと職場でのコラボレーションを求める消費者の需要が、4Kディスプレイ解像度市場における複数のセグメントで勢いを支えています。

- OLEDパネルは年平均成長率16.7%で成長すると予測されており、これは4Kディスプレイ解像度市場で最も速いペースです。Samsung Displayは2025年に143万枚のQD-OLEDモニターパネルを出荷する計画を発表しており、これはフラッグシップTV以外にも幅広い用途への普及を促進する生産能力の拡大を象徴しています。優れたコントラスト、ピクセルレベルの調光、そしてタンデムOLEDスタックの導入は、ゲーミングモニターにも採用され、平均販売価格(ASP)の上昇を促しています。LGが2025年に発表するG5 TVは、165Hzネイティブリフレッシュレートとマイクロレンズアレイ光学系を備えており、OLEDの研究開発が継続的に進んでいることを示しています。

- LCD技術は、豊富な設備投資、成熟したサプライチェーン、そしてミッドレンジ市場におけるコスト競争力により、2024年も71%のシェアを維持しました。ミニLEDバックライトは、ローカルディミングと高輝度を実現し、OLEDとの性能差を低コストで埋めます。ソニーのHDR1000対応手術用モニターは、ミニLEDが特殊用途分野に及ぼす影響力を示しています。マイクロLEDは、ハイセンスの136インチモニターに見られるように、製造歩留まりが改善するまでは超大型ディスプレイに限定されます。複数のパネルタイプが共存することで、拡大する4Kディスプレイ解像度市場において、ゲーム、サイネージ、ヘルスケアなど、あらゆるアプリケーションにおいて、コスト、輝度、寿命の最適なバランスが確保されます。

- 4Kディスプレイ解像度市場レポートは、製品タイプ(スマートテレビ、モニター、スマートフォン、タブレットなど)、パネル技術(LCD、OLED、ミニLED、マイクロLED)、画面サイズ(32インチ未満、32~49インチ、50~65インチ、66~84インチ、85インチ以上)、エンドユーザー分野(コンシューマーエレクトロニクス、ゲームおよびeスポーツ会場、ビジネスおよび教育など)、および地域別にセグメント化されています。市場予測は金額(米ドル)で提供されます。

4K Display Resolution Market Analysis

The 4K display resolution market size is estimated at USD 217.23 billion in 2025 and is forecast to reach USD 412.57 billion by 2030, advancing at a 13.69% CAGR. Fast-declining panel costs, a richer supply of native 4K streaming content, and expanding corporate use cases are allowing the technology to move from premium positioning into mass adoption. Asia Pacific’s manufacturing scale keeps average selling prices low while the region’s consumers display a marked preference for larger screens. Hybrid-work demand and immersive gaming are further tightening refresh cycles, encouraging brands to launch increasingly specialized models. At the same time, supply chain risks around chipsets and evolving energy-efficiency rules in Europe urge vendors to diversify component sourcing and accelerate R&D in low-power backlighting.

Global 4K Display Resolution Market Trends and Insights

Rapid OTT-led Uptake of 4K Streaming in North America

Streaming platforms delivered more than 60% of their new content in 4K during 2024, setting a stronger pull for compatible screens in household upgrades. Bandwidth gains from Wi-Fi 7, which supports data rates up to 46 Gbit/s, remove the previous bottlenecks that limited mainstream 4K adoption. Millimeter-wave rollouts, with Japan targeting 50,000 base stations by 2027, add further capacity that benefits cross-border content providers. The result is a steeper replacement cycle for television sets and monitors, with streaming services shaping feature roadmaps around HDR performance and wider color gamuts. Brands that synchronize panel launches with blockbuster content premieres are capturing early-adopter interest ahead of key sales quarters.

Panel Subsidies and Capacity Expansion in China and South Korea

Government incentives trimmed capital costs for new LCD and QD-OLED lines, enabling firms such as BOE Technology and Samsung Display to run plants at high utilization. Samsung Display plans to raise QD-OLED monitor panel shipments by 50% to 1.43 million units in 2025, giving OEM partners more scope to refresh premium catalogs. Economies of scale flowing from these investments support competitive pricing in the 50-65″ mainstream sweet spot, while yield-driven cost erosion in Mini-LED backlights widens adoption in mid-tier models. The subsidy-induced volume surge is already filtering through global supply chains, lowering bill-of-materials outlays for downstream assemblers.

HDMI 2.1 Chipset Shortages 2024-25

Constrained wafer starts at leading foundries have a limited supply of HDMI 2.1 retimer and switch ICs, delaying volume shipments of flagship gaming monitors and high-end TVs. Himax Technologies reported that 82.9% of 2024 revenue came from display driver ICs, underscoring dependence on a narrow component pool. Vendors redirected scarce chipsets to models with higher gross margins, creating temporary stockouts in mid-tier SKUs. The scarcity also accelerated DisplayPort 2.1 adoption, as seen in MSI’s new QD-OLED monitor, signaling possible long-term interface diversification even after supply normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Esports Demand for 4K/144 Hz Gaming Monitors in Europe

- Adoption of 4K Surgical and Diagnostic Displays in U.S. and Japan

- EU Eco-design Rules Raising Compliance Costs for >65″ TVs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gaming monitors accounted for a 14.1% CAGR forecast between 2025 and 2030, the fastest trajectory within the 4K display resolution market. Samsung upheld a 21.0% global share in 2024, while its 34.6% slice of the OLED sub-segment confirmed a first-mover advantage in emerging QD-OLED stacks. The segment thrives on esports sponsorship visibility, frequent model refreshes, and the synergy with powerful GPUs such as NVIDIA GeForce RTX 4090 that unlocked stable 4K/144 Hz gameplay. Monitor brands elevate specifications with higher peak brightness, tandem OLED layers, and DisplayPort 2.1 input to differentiate premium SKUs. Profitability remains thicker than mainstream TVs because enthusiast buyers value response time, HDR contrast, and color coverage.

Smart TVs preserved leadership with a 68% revenue share in 2024, supported by wide 4K streaming content libraries and falling BOM costs. Corporate video walls and digital signage screens gained importance as hybrid-work hubs required wide viewing angles and high pixel density. Medical displays formed a high-margin niche, with 4K surgical monitors like Sony’s LMD-32M1MD achieving VESA HDR1000 compliance for operating theaters. Smartphones and tablets with native 4K remain limited to creator-focused uses because energy draw offsets mobile benefits. Overall, consumer appetite for richer entertainment and workplace collaboration sustains multi-segment momentum within the 4K display resolution market.

OLED panels are projected to expand at a 16.7% CAGR, the swiftest run in the 4K display resolution market. Samsung Display’s plan to ship 1.43 million QD-OLED monitor panels in 2025 exemplifies the capacity scaling that propels wider use beyond flagship TVs. Superior contrast, pixel-level dimming, and the introduction of tandem OLED stacks now reach gaming monitors, encouraging ASP premiums. LG’s 2025 G5 TV, with a 165 Hz native refresh and Micro Lens Array optics, underscores the continued pace of OLED R&D.

LCD technology retained 71% share in 2024 because of vast installed tooling, mature supply chains, and cost competitiveness for mid-range sets. Mini-LED backlighting adds local dimming and higher luminance, bridging performance gaps with OLED at a lower cost. Sony’s HDR1000-rated surgical monitor demonstrates Mini-LED influence in specialty verticals. Micro-LED remains confined to ultra-large formats, evidenced by Hisense’s 136-inch showpiece, until manufacturing yields improve. The coexistence of multiple panel types ensures that each application – gaming, signage, healthcare – receives an optimal balance of cost, brightness, and longevity within the expanding 4K display resolution market.

The 4K Display Resolution Market Report is Segmented by Product Type (Smart TV, Monitor, Smartphone, Tablet, and More), Panel Technology (LCD, OLED, Mini-LED, and Micro-LED), Screen Size (Sub 32 Inch, 32-49 Inch, 50-65 Inch, 66-84 Inch, and Above 85 Inch), End-User Vertical (Consumer Electronics, Gaming and Esports Venues, Business and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 46% of 2024 revenue, cementing its position as the largest territory in the 4K display resolution market. China’s subsidies enabled swift capacity ramps, while South Korea’s OLED leadership supplied high-margin panels globally. Japan’s goal of installing 50,000 millimeter-wave bases by 2027 reinforces the regional network backbone supporting 4K streaming uptake. India and Southeast Asia entered a new adoption phase as falling ASPs aligned with rising discretionary income, unlocking large untapped volumes.

The Middle East is forecast to post the highest CAGR at 13.6% between 2025 and 2030. GCC corporations rolled out 4K video walls to enhance hybrid collaboration, boosting demand for fine-pixel-pitch LED assemblies. Sony Middle East and Africa reported notable sales gains and aims to release the INZONE M9 4K monitor within 2025, reflecting the region’s appetite for premium displays. Online channels have already captured 20% of regional TV sales, prompting brands to fine-tune e-commerce logistics.

North America’s mature installed base still grew on the back of fast OTT content adoption and a robust gaming monitor upgrade cycle. Healthcare institutions expanded to 4K diagnostic suites, widening a lucrative sub-segment less exposed to price wars. Europe faced a dual narrative: tech-savvy consumers embraced larger OLED sets while stricter Eco-design norms raised compliance costs for panels over 65″, nudging suppliers toward energy-efficient Mini-LED designs. Latin America and Africa remained emergent frontiers; limited 4K broadcast spectrum in parts of Sub-Saharan Africa tempered growth, though rising broadband coverage signals future upside.

List of Companies Covered in this Report:

- Samsung Electronics Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- TCL Technology (CSOT)

- Sony Group Corporation

- Toshiba Corporation

- Panasonic Holdings Corporation

- Sharp Corporation

- Hisense Group

- Koninklijke Philips N.V.

- Innolux Corporation

- AU Optronics Corp.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Vizio Inc.

- Skyworth Group Ltd

- Barco NV

- Eizo Corporation

- ViewSonic Corporation

- BenQ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support