South Korea Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

韓国データセンター市場レポートは、データセンター規模(大規模、超大規模、中規模、メガ、小規模)、ティアタイプ(ティア1、ティア2、ティア3、ティア4)、データセンタータイプ(ハイパースケール/自社構築、エンタープライズ/エッジ、コロケーション)、エンドユーザー(BFSI、ITおよびITES、Eコマース、政府機関、製造業、メディアおよびエンターテインメントなど)、およびホットスポット別にセグメント化されています。市場予測はIT負荷容量(MW)に基づいて提供されます。

The South Korea Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 134 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14674 |

韓国のデータセンター市場は2025年に16億5,000万米ドル規模となり、予測期間(2026~2031年)中にCAGR20.38%で成長し、2026年の19億9,000万米ドルから2031年には50億2,000万米ドルに達するとMordor Intelligenceでは予測しています。

Mordor Intelligence(モードーインテリジェンス)「韓国のデータセンター市場シェア分析、業界動向と統計、成長予測 2026-2031年 – South Korea Data Center – Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 – 2031)」は韓国のデータセンタ市場を調査し、主要セグメント別に分析・予測を行っています。

調査対象セグメント

- データセンタ規模

- 大規模

- 巨大

- 中規模

- メガ

- 小規模

- ティア基準

- ティア1とティア2

- ティア3

- ティア4

- データセンタタイプ

- ハイバースケール/セルフビルド

- エンタープライズ/エッジ

- コロケーション

- ノンユーティライズド

- ユーティライズド

- 小売コロケーション

- 卸売コロケーション

- エンドユース産業

- BFSI

- IT&ITes

- eコマース

- 政府

- 製造業

- メディア&エンターテインメント

- 電気通信

- その他のエンドユーザ

- ホットスポット

- ソウル

- 釜山

- その他の韓国

IT負荷容量の面では、市場は2025年の1,960メガワットから2030年には6,320メガワットに成長し、予測期間(2025~2030年)中に26.29%のCAGRで成長すると予想されています。市場セグメントのシェアと推定値は、MW単位で計算および報告されています。北東アジアのAIインフラハブとしてのソウルの役割、政府による広範な税制優遇措置と直接PPA改革パッケージ、そして数十億ドル規模のハイパースケール計画の発表が相まって、容量展開を加速させています。事業者は、運用コストの抑制を目指し、高度な冷却、高密度電力供給、再生可能エネルギー調達に多額の投資を行っています。全国的な5Gカバレッジ、オープンバンキングの義務化、そして韓国の急成長するKコンテンツ輸出によって、需要はさらに拡大しています。これらの要因はいずれも、コンプライアンスに準拠し、レイテンシが最適化された施設へのワークロードの流入を促しています。そのため、韓国のデータセンター市場は、政策、資本、テクノロジーが融合し、デジタルインフラを戦略的ユーティリティとして扱うようになり、アジア太平洋地域の他の多くの国よりも急速に拡大しています。

セグメント分析

- 5~20MWの中規模施設は、低遅延接続への需要の高まりを捉え、2025年には大規模施設が韓国のデータセンター市場シェアの40.72%を維持するものの、年平均成長率(CAGR)26.95%で成長すると予測されています。インダストリー4.0、遠隔医療、ARアプリケーションを推進する企業は、規模よりも近接性を重視し、設備投資を地方キャンパスにシフトさせています。

- その結果、二層構造の供給戦略が生まれています。大規模キャンパスはAIトレーニングのためにソウル首都圏に集中し、中規模サイトは地域消費に対応するため釜山、京畿道、忠清北道に集中しています。政府の経済自由区域(FEEZ)による優遇措置と事前承認された土地区画により、建設スケジュールが加速しています。2031年までに、中規模施設は韓国のデータセンター市場規模の18.92%を占めると予想され、ハイパースケールコアを補完する不可欠なエッジレイヤーを提供します。

- 2025年には、Tier 3設計が韓国のデータセンター市場規模の52.15%を占め、年平均成長率(CAGR)27.15%で成長を牽引すると予想されます。金融規制当局、クラウドサービスプロバイダー、ゲームスタジオは、電源と冷却の両方においてN+1冗長性を求める傾向が高まっています。

- KBC-2018に基づく耐震性要件は、Tier 3のフォールトトレランス原則と自然に整合しており、新規構築においてはTier 3がデフォルトの仕様となっています。事業者は、Tier 2ではBFSIや医療ワークロードの要件を満たすためのリスク許容度が不足している一方で、Tier 4のプレミアムはほとんどのROIハードルを超えていることに気づいています。したがって、Tier 3の技術的な優位性は、韓国のデータセンター市場で期待される信頼性基準の基盤となっています。

- 韓国データセンター市場レポートは、データセンター規模(大規模、超大規模、中規模、メガ、小規模)、ティアタイプ(ティア1、ティア2、ティア3、ティア4)、データセンタータイプ(ハイパースケール/自社構築、エンタープライズ/エッジ、コロケーション)、エンドユーザー(BFSI、ITおよびITES、Eコマース、政府機関、製造業、メディアおよびエンターテインメントなど)、およびホットスポット別にセグメント化されています。市場予測はIT負荷容量(MW)に基づいて提供されます。

South Korea Data Center Market Analysis

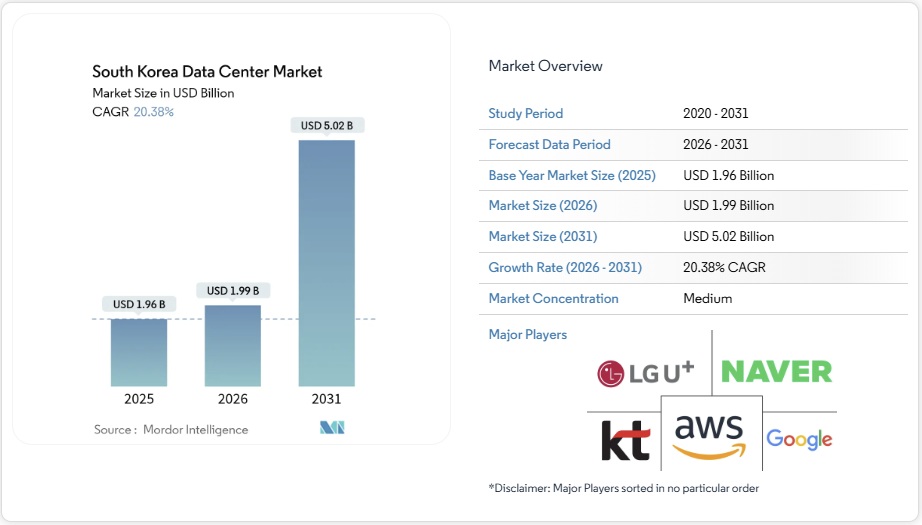

The South Korea Data Center Market was valued at USD 1.65 billion in 2025 and estimated to grow from USD 1.99 billion in 2026 to reach USD 5.02 billion by 2031, at a CAGR of 20.38% during the forecast period (2026-2031). In terms of IT load capacity, the market is expected to grow from 1.96 thousand megawatt in 2025 to 6.32 thousand megawatt by 2030, at a CAGR of 26.29% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Seoul’s role as Northeast Asia’s AI infrastructure hub, the government’s broad package of tax holidays and direct-PPA reforms, and multi-billion-dollar hyperscale announcements together accelerate capacity roll-outs. Operators are investing heavily in advanced cooling, high-density power delivery, and renewable-energy procurement to control operating expenditure. Demand is further amplified by nationwide 5G coverage, open-banking mandates, and Korea’s booming K-content exports, each of which pushes workloads toward compliant, latency-optimized facilities. The South Korea data center market is therefore expanding faster than most APAC peers as policy, capital, and technology converge to treat digital infrastructure as a strategic utility.

South Korea Data Center Market Trends and Insights

Surge in Hyperscale Cloud and AI Build-outs

Gigawatt-scale commitments from SK Telecom, Amazon Web Services, and Digital Realty are reshaping the South Korea data center market by favoring purpose-built AI campuses that can cool 70 kW racks and deliver triple-feed power resiliency. Capital allocations, such as a USD 35 billion pledge to deliver 3 GW of capacity, illustrate how AI is elevating data centers from commercial real-estate plays to core national infrastructure. Facilities outside Seoul, including Samsung SDS’s new GPU site in Gumi, signal an emerging distributed topology that reduces latency while bolstering national redundancy. Purpose-built AI halls increasingly incorporate liquid and rear-door immersion systems, which cut PUE targets below 1.2, aligning cost control with sustainability objectives. Collectively, these trends position the South Korea data center market as a key battleground in Asia’s AI compute race.

Government Tax Incentives and RE100 Road-map Support

Enhanced foreign-direct-investment rules provide cash grants of up to 75% and seven-year tax holidays to digital-infrastructure projects in designated zones. Simultaneously, 2022 amendments to the Electric Utility Act allow operators to sign direct renewable PPAs, bypassing KEPCO’s single-buyer model and locking in tariff predictability. The dual incentive of fiscal relief and green-energy access shortens payback periods on megawatt-scale builds. Multinationals view the framework as a credible hedge against the carbon-pricing trajectory that the national ETS is set to tighten after 2027. Combined, these measures are encouraging global hyperscalers to pre-commit capacity, accelerating the South Korea data center market’s supply pipeline.

High Electricity Tariffs and Carbon-Pricing Risks

Korea’s 63.6% fossil-fuel power mix exposed operators to KRW 22 trillion in additional costs during the 2022 LNG crisis. KEPCO’s debt load surpassing KRW 202 trillion restricts grid-upgrade budgets, delaying high-amp feeder deployments needed for 100 MW campuses. Carbon surcharges climbed from KRW 7.3/kWh in 2022 to KRW 9/kWh in 2023, and the third-phase ETS tightening in 2026 will lift them again. While PPAs cut exposure, current rules prevent operators from retaining RECs when using direct contracts, weakening Scope 2 reporting benefits. These dynamics shave 340 basis points off the forecast CAGR for the South Korea data center market unless reforms allow bundled REC transfers.

Other drivers and restraints analyzed in the detailed report include:

- 5G-Driven Data Traffic Explosion

- Accelerated Digital-Banking Roll-outs

- Scarcity of Suitable Land and Power in Seoul

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-scale sites of 5-20 MW captured rising demand for low-latency connectivity, growing at a forecast 26.95% CAGR even though large halls retained 40.72% of the South Korea data center market share in 2025. Enterprises pursuing Industry 4.0, telemedicine, and AR applications now prioritize proximity over sheer scale, shifting capex toward provincial campuses.

The result is a two-tier supply strategy: massive campuses stay concentrated in Seoul’s metro ring for AI training, while medium sites populate Busan, Gyeonggi, and North Chungcheong to serve regional consumption. Government Free Economic Zone incentives and pre-approved land parcels accelerate build schedules. By 2031, medium facilities are expected to comprise 18.92% of the South Korea data center market size, providing an indispensable edge layer that complements hyperscale cores.

Tier 3 designs delivered 52.15% of the South Korea data center market size in 2025 and will lead growth at a 27.15% CAGR. Financial regulators, cloud-service providers, and gaming studios increasingly demand N+1 redundancy for both power and cooling.

Seismic-resilience mandates under KBC-2018 naturally align with Tier 3 fault-tolerance principles, making Tier 3 the default specification for new builds. Operators find that Tier 2 lacks the risk envelope to win BFSI or healthcare workloads, whereas Tier 4 premiums exceed most ROI hurdles. Consequently, Tier 3’s technical sweet spot underpins the reliability standards expected in the South Korea data center market.

The South Korea Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- LG Uplus Corp

- KT Corporation

- Naver Corporation

- Amazon Web Services, Inc.

- Google LLC

- Oracle Corporation

- SK Broadband Co., Ltd.

- Digital Edge (Singapore) Holdings Pte Ltd

- Alibaba Cloud

- Microsoft Corporation

- LG CNS Co., Ltd.

- Kakao Corporation

- LOTTE INNOVATE Co., Ltd.

- KINX Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

South Korea Data Center Market Report Scope

Busan, Greater Seoul are covered as segments by Hotspot. Large, Massive, Medium, Mega, Small are covered as segments by Data Center Size. Tier 1 and 2, Tier 3, Tier 4 are covered as segments by Tier Type. Non-Utilized, Utilized are covered as segments by Absorption.

- By Data Center Size

- Large

- Massive

- Medium

- Mega

- Small

- By Tier Standard

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Hyperscale / Self-Built

- Enterprise / Edge

- Colocation Non-Utilized

- UtilizedRetail Colocation

- Wholesale Colocation

- By End User Industry

- BFSI

- IT and ITES

- E-Commerce

- Government

- Manufacturing

- Media and Entertainment

- Telecom

- Other End Users

- By Hotspot

- Seoul

- Busan

- Rest of South Korea

- By Data Center Size

- Large

- Massive

- Medium

- Mega

- Small

- By Tier Standard

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Hyperscale / Self-Built

- Enterprise / Edge

- Colocation

- Non-Utilized

- Utilized

- Retail Colocation

- Wholesale Colocation

- By End User Industry

- BFSI

- IT and ITES

- E-Commerce

- Government

- Manufacturing

- Media and Entertainment

- Telecom

- Other End Users

- By Hotspot

- Seoul

- Busan

- Rest of South Korea

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Surge in hyperscale cloud and AI build-outs

4.2.2 Government tax incentives and RE100 road-map support

4.2.3 5G-driven data traffic explosion

4.2.4 Accelerated digital-banking (open-banking) roll-outs

4.2.5 Renewable-energy PPAs lowering OPEX

4.2.6 K-content (K-POP, gaming, OTT) traffic spikes

4.3 Market Restraints

4.3.1 High electricity tariffs and carbon-pricing risks

4.3.2 Scarcity of suitable land/power in Seoul metro

4.3.3 Grid-renewables bottleneck delaying new permits

4.3.4 Stringent seismic/structural codes inflating CAPEX

4.4 Market Outlook

4.4.1 IT Load Capacity

4.4.2 Raised Floor Space

4.4.3 Colocation Revenue

4.4.4 Installed Racks

4.4.5 Rack Space Utilization

4.4.6 Submarine Cable

4.5 Key Industry Trends

4.5.1 Smartphone Users

4.5.2 Data Traffic Per Smartphone

4.5.3 Mobile Data Speed

4.5.4 Broadband Data Speed

4.5.5 Fiber Connectivity Network

4.5.6 Regulatory Framework

4.6 Value Chain and Distribution Channel Analysis

4.7 Porter’s Five Forces Analysis

4.7.1 Threat of New Entrants

4.7.2 Bargaining Power of Buyers

4.7.3 Bargaining Power of Suppliers

4.7.4 Threat of Substitutes

4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

5.1 By Data Center Size

5.1.1 Large

5.1.2 Massive

5.1.3 Medium

5.1.4 Mega

5.1.5 Small

5.2 By Tier Standard

5.2.1 Tier 1 and 2

5.2.2 Tier 3

5.2.3 Tier 4

5.3 By Data Center Type

5.3.1 Hyperscale / Self-Built

5.3.2 Enterprise / Edge

5.3.3 Colocation

5.3.3.1 Non-Utilized

5.3.3.2 Utilized

5.3.3.2.1 Retail Colocation

5.3.3.2.2 Wholesale Colocation

5.4 By End User Industry

5.4.1 BFSI

5.4.2 IT and ITES

5.4.3 E-Commerce

5.4.4 Government

5.4.5 Manufacturing

5.4.6 Media and Entertainment

5.4.7 Telecom

5.4.8 Other End Users

5.5 By Hotspot

5.5.1 Seoul

5.5.2 Busan

5.5.3 Rest of South Korea

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

6.4.1 LG Uplus Corp

6.4.2 KT Corporation

6.4.3 Naver Corporation

6.4.4 Amazon Web Services, Inc.

6.4.5 Google LLC

6.4.6 Oracle Corporation

6.4.7 SK Broadband Co., Ltd.

6.4.8 Digital Edge (Singapore) Holdings Pte Ltd

6.4.9 Alibaba Cloud

6.4.10 Microsoft Corporation

6.4.11 LG CNS Co., Ltd.

6.4.12 Kakao Corporation

6.4.13 LOTTE INNOVATE Co., Ltd.

6.4.14 KINX Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-space and Unmet-need Assessment