Semiconductor Memory For Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

自動車向け半導体メモリ市場レポートは、テクノロジの役割 (コード ストレージ、ワーキング メモリなど)、メモリの種類 (DRAM、NAND フラッシュなど)、アプリケーション (ADAS および自動運転、デジタル コックピットなど)、車両の種類 (乗用車、小型商用車など)、メモリ密度 (128 Mb 未満など)、および地域別にセグメント化されています。

The Semiconductor Memory Market for Automotive Report is Segmented by Technology Role (Code Storage, Working Memory, and More), Memory Type (DRAM, NAND Flash, and More), Application (ADAS and Automated Driving, Digital Cockpit, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Memory Density (Below 128 Mb and More) and Geography.

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 127 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14518 |

自動車向け半導体メモリ市場は、2025年の137億米ドルから2026年には162億9,000万米ドルに成長し、2031年には387億7,000万米ドルに達すると予測されています。これは、2026年から2031年にかけて年平均成長率(CAGR)18.94%で推移する見込みです。この急成長は、数十もの電子機能を集中コンピューティング領域に統合するソフトウェア定義車両(SDA)への移行によって加速しており、車両1台あたりのメモリ密度と帯域幅の要件が急増しています。中国、米国、欧州連合におけるレベル2+運転支援システム(DAV)の規制強化により、機能安全基準を満たすギガバイト規模のワーキングメモリの需要が加速しています。一方、コスト最適化された3D NANDと今後登場するMRAMの選択肢により、対応可能なアプリケーション範囲が拡大し、自動車メーカーは性能と部品コストのプレッシャーをより効果的にバランスさせることができます。米国と欧州におけるサプライチェーンのローカライゼーションの進展は、調達戦略を複数調達による車載用メモリへと導き、特定地域への過度な依存を減らしています。さらに、高級車向けプログラムは、フラッシュ容量要件の増大と次世代モジュールの耐久性の高い交換サイクルの構築を可能にする、OTA(Over The Air)ソフトウェア戦略の先駆者となっています。

セグメント分析

- ADAS(先進運転支援システム)やインフォテインメント機器におけるリアルタイム処理負荷の高さから、ワーキングメモリは半導体メモリ市場を牽引し、2025年には38.72%のシェアを占めました。高級EVは現在、集中型コンピューティングクラスタ向けに最大32GBのLPDDR5メモリを搭載しており、量販モデルは2027年までに16GBへと移行すると予想されています。ファームウェアのフットプリントが8~16GB程度で推移する中、コードストレージは安定的に推移しています。一方、データストレージは、車両がエッジ分析のためにテラバイト単位のセンサーデータを収集する中で、年平均成長率20.02%で急成長しています。半導体メモリ市場規模はデータストレージと連動しており、大容量3D NANDデバイスに対する長期的な需要を支えています。

- ワーキングメモリの見通しは、安全、コックピット、パワートレインの各ドメインで共有されるメモリプールを標準化するゾーンアーキテクチャの登場によってさらに明るくなっています。この統合により、モジュールあたりの性能向上が求められ、幅広いI/Oインターフェースと内蔵ECCエンジンへの転換が促進されます。デュアルパーパスDRAM-NANDの組み合わせを提供するサプライヤーは、認定パイプラインの合理化を目指すOEMの間で、市場シェアを拡大する態勢が整っています。評価中のHBM-Liteコンセプトは、熱問題の解決が図られれば、2028年以降に実現する可能性があり、半導体メモリ市場に新たな収益源が生まれる可能性があります。

- DRAMは2025年の売上高の31.85%を占め、センサーフュージョンや車両ダイナミクスといったレイテンシ重視のワークロードにおいて依然としてトップの地位を維持しています。同時に、3D NANDはビット単価の低下とAEC-Q100規格の適用範囲拡大に牽引され、19.25%の成長ペースで成長しています。4,200MB/秒の読み取り速度を誇る車載グレードのUFS 4.1ドライブは、データレコーダーやOTA(Over-The-Air)ファームウェアリポジトリのデフォルトストレージソリューションとして台頭しています。

- NORフラッシュは引き続きブートおよびリカバリタスクを遂行していますが、密度の制約により年間成長率は制限されています。MRAMをはじめとする新興のNVMは、フェイルセーフ・ログ機能や瞬時に起動するダッシュボードといったニッチな領域で確固たる地位を築いています。全体的な動向は明らかです。DRAMは演算負荷の高いAIブロックに電力を供給し、3D NANDは高まる永続ストレージへの需要を支え、半導体メモリ市場の中心で補完的な役割を果たしています。

- 自動車向け半導体メモリ市場レポートは、技術的役割(コードストレージ、ワーキングメモリなど)、メモリタイプ(DRAM、NANDフラッシュなど)、アプリケーション(ADASおよび自動運転、デジタルコックピットなど)、車種(乗用車、小型商用車など)、地域(北米、南米、欧州など)別にセグメント化されています。市場予測は金額(米ドル)で提供されています。

Analysis of Semiconductor Memory Market For Automotive

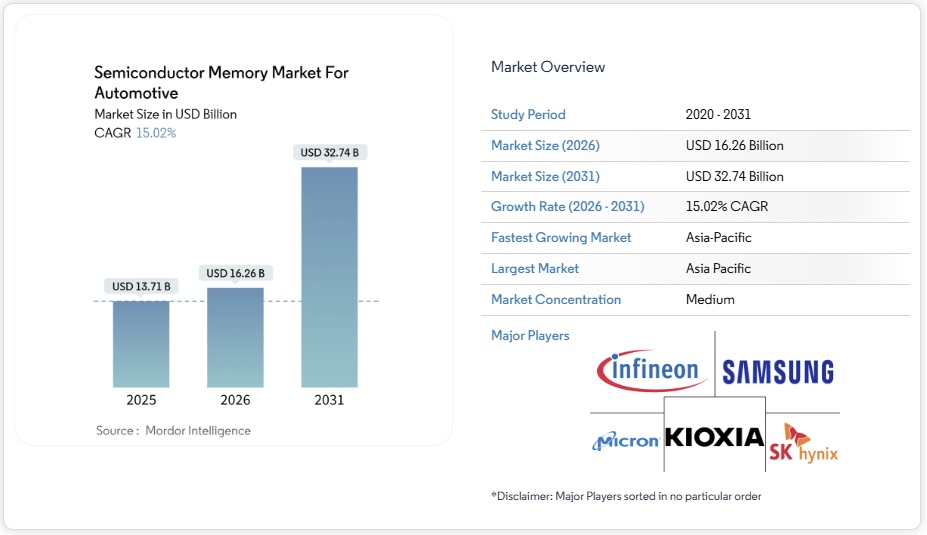

The semiconductor memory market for automotive is expected to grow from USD 13.7 billion in 2025 to USD 16.29 billion in 2026 and is forecast to reach USD 38.77 billion by 2031 at 18.94% CAGR over 2026-2031. The surge is fueled by the shift toward software-defined vehicles, which bundle dozens of electronic functions into centralized compute domains, sharply increasing memory density and bandwidth requirements per car. Regulatory momentum behind Level 2+ driver assistance in China, the United States, and the European Union is accelerating demand for gigabyte-scale working memory that can meet functional-safety standards. Meanwhile, cost-optimized 3D NAND and upcoming MRAM options are expanding the addressable base of applications, letting automakers balance performance and bill-of-materials pressures more effectively. Intensifying supply-chain localization in the United States and Europe is also steering procurement strategies toward multi-sourced, automotive-qualified memory, reducing overreliance on any single region. Finally, premium vehicle programs are pioneering over-the-air software strategies that multiply flash capacity requirements and build a durable replacement cycle for next-generation modules.

Insights and Trends of Semiconductor Memory Market For Automotive

Software-Defined Vehicle Adoption

Automakers are transforming cars into rolling data centers that rely on continuous software updates and feature deployment. Tesla’s Hardware 4.0 showcases a significant leap in memory intensity by integrating multiple LPDDR5 stacks, which stream 12 camera feeds and radar inputs in real-time. Centralized designs slash the traditional network of more than 100 ECUs to a handful of high-performance domain controllers, raising installed DRAM from megabyte ranges to multi-gigabyte footprints. Luxury trims are already equipped with 32 GB of total memory, and mainstream models are expected to trend toward similar capacities by 2027. The upgrade path aligns with longer software maintenance cycles, ensuring recurring demand for high-bandwidth, AEC-Q100 Grade 1 modules.

Centralized/Zonal E-E Architecture

BMW’s forthcoming iDrive generation demonstrates how zonal designs allocate memory resources efficiently, rather than assigning discrete modules to each subsystem. Consolidation eliminates duplication, reducing part counts by up to 30%. However, each surviving module must deliver higher throughput and withstand heavier thermal loads. The net effect is a shift in demand toward 64-bit-wide DRAM interfaces and faster access speeds, approaching 6 Gb/s, particularly in the infotainment and ADAS domains. Tier-1 suppliers are adapting by co-packaging memory and processors on high-density substrates, a trend that favors vendors with advanced capabilities at the 10 nm node and below. The architecture is rolling out first in premium nameplates but is expected to penetrate mass-market segments within four years.

Supply-Chain Volatility

The 2024 Taiwan earthquake exposed the fragility of geographically concentrated fabs, disrupting controller output and inflating lead times for Grade-1 memory by 20 weeks. Automotive lines, which account for under 10% of total wafer demand, often drop in supplier priority when shortages occur. OEMs are therefore dual-sourcing between South Korea and the United States, but qualification cycles extend this mitigation effort to at least 2026. Divergent export-control regimes and geopolitical uncertainty could shave 100–150 basis points off near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Domain-Specific AI Accelerators in MCUs

- Growing Memory Content per Level-2+ ADAS ECU

- High Automotive Selling Price (ASP) Premium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Working memory dominated the semiconductor memory market, accounting for a 38.72% share in 2025, due to the high real-time processing loads in ADAS and infotainment units. Luxury EVs now integrate up to 32 GB of LPDDR5 for centralized compute clusters, while mass-market models are expected to trend toward 16 GB by 2027. Code storage remains stable as firmware footprints plateau around 8–16 GB, while data storage rockets at a 20.02% CAGR as vehicles harvest terabytes of sensor data for edge analytics. The semiconductor memory market size is tied to data storage, reinforcing long-term demand for high-capacity 3D NAND devices.

The outlook for working memory is further buoyed by the arrival of zonal architectures that standardize memory pools shared across safety, cockpit, and powertrain domains. This consolidation demands higher per-module performance, driving a pivot toward wide-I/O interfaces and built-in ECC engines. Suppliers offering dual-purpose DRAM-NAND combinations are poised to capture incremental market share among OEMs seeking to streamline their qualification pipelines. HBM-Lite concepts under evaluation could emerge after 2028 if thermal hurdles are resolved, potentially opening an adjacent revenue stream within the semiconductor memory market.

DRAM delivered 31.85% of 2025 revenue, maintaining its leading position in latency-critical workloads, such as sensor fusion and vehicle dynamics. Simultaneously, 3D NAND is advancing at a 19.25% growth pace, driven by declining cost-per-bit and broader AEC-Q100 coverage. Automotive-grade UFS 4.1 drives, which offer 4,200 MB/s read speeds, are emerging as the default storage solutions for data recorders and over-the-air firmware repositories.

NOR flash continues to fulfill boot and recovery tasks, but density limitations restrict its annual expansion. MRAM and other emerging NVMs are carving niche footholds in fail-safe logging and instant-on dashboards. The overarching dynamic is clear: DRAM feeds compute-intensive AI blocks, while 3D NAND underpins the escalating appetite for persistent storage, forming a complementary duo at the heart of the semiconductor memory market.

The Semiconductor Memory Market for Automotive Report is Segmented by Technology Role (Code Storage, Working Memory, and More), Memory Type (DRAM, NAND Flash, and More), Application (ADAS and Automated Driving, Digital Cockpit, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 37.95% semiconductor memory market share in 2025 and is expected to broaden its lead at a 19.88% CAGR, buoyed by China’s aggressive EV penetration targets and South Korea’s manufacturing depth. China alone represents a significant share of regional volume but faces continuing headwinds from export-control measures on advanced nodes. South Korea leverages its vertically integrated champions, Samsung and SK Hynix, to secure long-term contracts with global Tier-1s, while Japan’s close collaboration between memory fabs and automotive suppliers compresses qualification lead times.

North America ranks second, backed by USD 52 billion CHIPS Act subsidies aimed at reshoring semiconductor output, including dedicated automotive lines in Texas, Arizona, and Indiana. Tesla’s vertically integrated model and Detroit’s Ultium BEV platform are major off-takers, pushing domestic demand for Grade-1 LPDDR5-X and high-cycle SSDs. Canada and Mexico complement the region through battery-module assembly and cost-efficient electronics integration, respectively, fostering trilateral supply resiliency.

Europe is carving strategic autonomy via the EUR 43 billion European Chips Act, with consortia forming around German OEMs and memory makers to localize parts of the supply chain. The regulatory emphasis on ISO 26262 and ISO/SAE 21434 has elevated the demand for certified memory solutions. Meanwhile, the Middle East and Africa trail in absolute volume but are gaining traction through EV manufacturing incentives in the United Arab Emirates and South Africa, signaling an emerging frontier for the semiconductor memory market by the end of the decade.

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Micron Technology, Inc.

- SK hynix Inc.

- Kioxia Holdings Corporation

- Infineon Technologies AG

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Winbond Electronics Corporation

- Macronix International Co., Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution, Inc. (ISSI)

- Everspin Technologies, Inc.

- Powerchip Technology Corporation

- Transcend Information, Inc.

- Kingston Technology Corporation

- Swissbit AG

- Virtium LLC

- Alliance Memory, Inc.

- AP Memory Technology Corp.

- Semiconductor Manufacturing International Corp. (SMIC)

- Tower Semiconductor Ltd.

- Yangtze Memory Technologies Co. (YMTC)

- Western Digital Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Software-Defined Vehicle (SDV) adoption

4.2.2 Centralized/Zonal E-E Architecture

4.2.3 Domain-specific AI accelerators inside MCUs

4.2.4 Growing memory content per Level-2+ ADAS ECU

4.2.5 Wider OEM use of over-the-air (OTA) update cycles

4.2.6 Automotive-qualified 3D NAND cost decline

4.3 Market Restraints

4.3.1 Volatility in automotive silicon supply chain

4.3.2 High ASP gap vs. consumer-grade memory

4.3.3 Functional-safety certification lead-times

4.3.4 Thermal-management limits in high-density modules

4.4 Impact of Macroeconomic Factors on the Market

4.5 Industry Value Chain Analysis

4.6 Regulatory Landscape

4.7 Technological Outlook

4.8 Porter’s Five Forces Analysis

4.8.1 Threat of New Entrants

4.8.2 Bargaining Power of Buyers

4.8.3 Bargaining Power of Suppliers

4.8.4 Threat of Substitute Products

4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

5.1 By Technology Role

5.1.1 Code Storage

5.1.2 Working Memory

5.1.3 Data Storage

5.1.4 Other Roles (e.g., Boot, Logs)

5.2 By Memory Type

5.2.1 DRAM

5.2.2 NAND Flash

5.2.3 NOR Flash

5.2.4 MRAM and Emerging NVM

5.3 By Application

5.3.1 ADAS and Automated Driving

5.3.2 Digital Cockpit

5.3.3 Powertrain

5.3.4 Chassis and Safety

5.3.5 Body and Comfort

5.4 By Vehicle Type

5.4.1 Passenger Cars

5.4.2 Light Commercial Vehicles

5.4.3 Heavy Commercial Vehicles

5.5 By Geography

5.5.1 North America

5.5.1.1 United States

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.2 South America

5.5.2.1 Brazil

5.5.2.2 Argentina

5.5.2.3 Rest of South America

5.5.3 Europe

5.5.3.1 Germany

5.5.3.2 United Kingdom

5.5.3.3 France

5.5.3.4 Italy

5.5.3.5 Spain

5.5.3.6 Rest of Europe

5.5.4 Asia-Pacific

5.5.4.1 China

5.5.4.2 Japan

5.5.4.3 India

5.5.4.4 South Korea

5.5.4.5 South-East Asia

5.5.4.6 Rest of Asia-Pacific

5.5.5 Middle East and Africa

5.5.5.1 Middle East

5.5.5.1.1 Saudi Arabia

5.5.5.1.2 United Arab Emirates

5.5.5.1.3 Rest of Middle East

5.5.5.2 Africa

5.5.5.2.1 South Africa

5.5.5.2.2 Egypt

5.5.5.2.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

6.4.1 Samsung Electronics Co., Ltd.

6.4.2 Micron Technology, Inc.

6.4.3 SK hynix Inc.

6.4.4 Kioxia Holdings Corporation

6.4.5 Infineon Technologies AG

6.4.6 Renesas Electronics Corporation

6.4.7 NXP Semiconductors N.V.

6.4.8 Winbond Electronics Corporation

6.4.9 Macronix International Co., Ltd.

6.4.10 GigaDevice Semiconductor Inc.

6.4.11 Integrated Silicon Solution, Inc. (ISSI)

6.4.12 Everspin Technologies, Inc.

6.4.13 Powerchip Technology Corporation

6.4.14 Transcend Information, Inc.

6.4.15 Kingston Technology Corporation

6.4.16 Swissbit AG

6.4.17 Virtium LLC

6.4.18 Alliance Memory, Inc.

6.4.19 AP Memory Technology Corp.

6.4.20 Semiconductor Manufacturing International Corp. (SMIC)

6.4.21 Tower Semiconductor Ltd.

6.4.22 Yangtze Memory Technologies Co. (YMTC)

6.4.23 Western Digital Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-space and Unmet-need Assessment