| 出版社 | Mordor Intelligence |

| 出版年月 | 2025年7月 |

NA ICS – Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 – 2030)

北米の産業用制御システム市場レポートは、コンポーネント (ハードウェア、ソフトウェア、サービス)、システムのタイプ (監視制御およびデータ収集、分散制御システムなど)、通信プロトコル (フィールドバス、産業用イーサネット、ワイヤレス)、展開モード (オンプレミス、クラウド、ハイブリッド)、エンドユーザー業界、および地域別にセグメント化されています。

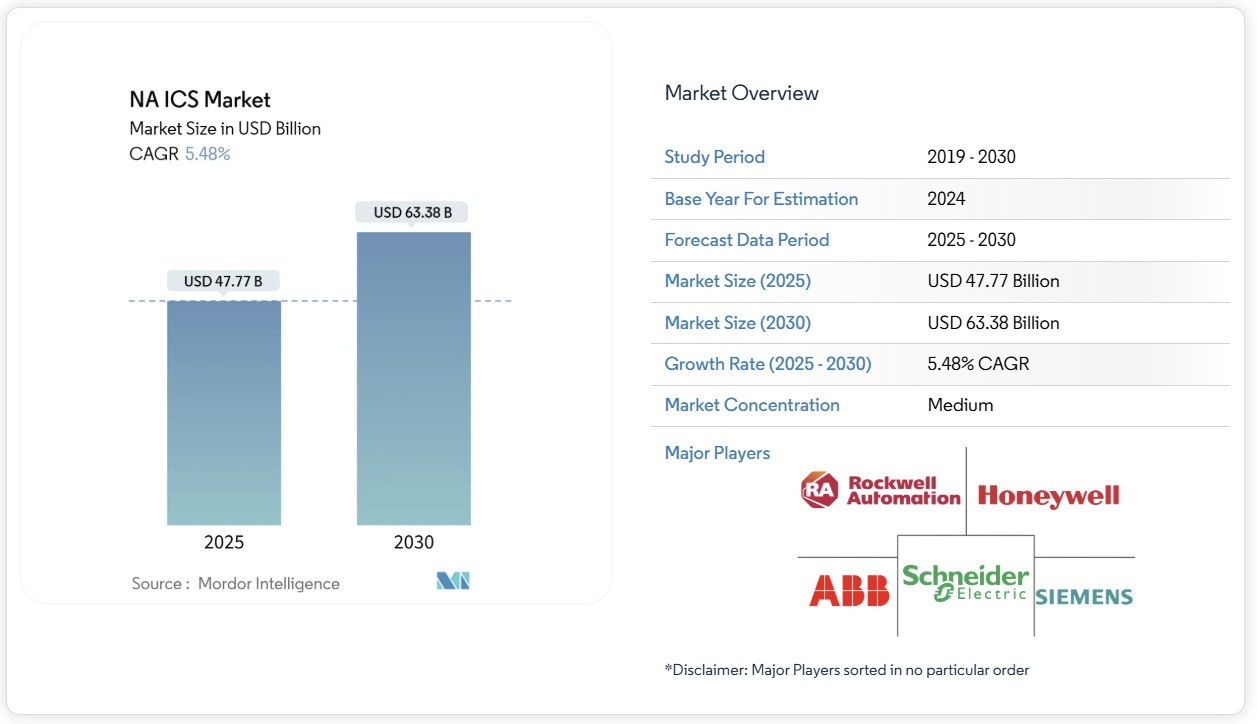

北米の産業用制御システム市場規模は、2025年に477億7,000万米ドルに達し、2030年には633億8,000万米ドルに達し、年平均成長率(CAGR)5.48%で成長すると予測されています。ハードウェアは、PLC、分散制御ハードウェア、I/Oモジュールへの着実な投資に支えられ、2024年も57.2%で最大の収益シェアを維持します。米国のCHIPS法によって4,500億米ドル規模の半導体生産能力投資が発表され、部品不足が緩和され、新たな自動化の展開が促進されたことで、需要が押し上げられています。産業用イーサネットは、2024年に設置された通信の48.9%を占め、工場が柔軟な接続を求める中で、無線プロトコルは10.4%のCAGRで成長しました。クラウド導入は9.31%のCAGRで拡大していますが、遅延の影響を受けやすい制御ループと厳格なセキュリティポリシーのため、81%の設置は依然としてオンプレミスのままです。自動車メーカーは需要の 18.6% を獲得しましたが、設計段階からの品質要求が強化されるにつれて、医薬品は 9.1% の CAGR で最も急速に成長しているエンドユーザーとなっています。

自動車メーカーは、柔軟性と稼働時間の向上を目指し、断片化された制御レイヤーを統合アーキテクチャに置き換えています。アウディの米国ボディショップは、プライベートクラウドに接続されたシーメンスSimatic S7-1500V仮想コントローラーを導入し、ITとOTのワークフローを統合し、段取り替え時間を短縮しました。米国工場のうち、機能を完全に自動化している工場はわずか31%にとどまっており、近代化の余地が大きいことが浮き彫りになっています。キンバリー・クラークの段階的なPLCからDCSへの移行は、その慎重なペースを示しています。ダウンタイムを最小限に抑えながら、サイバーセキュリティ対応プラットフォームを組み込むため、10年間で年間1ラインずつ移行を進めています。

セグメント分析

- ハードウェアは、PLCラック、DCSノード、モータードライブの継続的な受注に牽引され、2024年の売上高の57.2%を占めました。ABBのプロセスオートメーション部門は、2024年の売上高が68億米ドルとなり、資本設備への需要が継続していることを示しています。OPC UAとMQTTを内蔵したHoneywellのControlEdge PLCなど、エッジアナリティクスをコントローラに統合することで、プレミアムSKUの販売が伸びています。

- サービスは、オーナーがライフサイクルサポートをアウトソーシングするにつれて、規模は小さいものの、年平均成長率8.9%で急速に拡大しています。Rockwell Automationのライフサイクルサービスの受注残は、2024年9月に17億米ドルに達しました。これは、可用性の向上に応じて料金が決まる成果主義の契約への需要を反映しています。スキル不足(2025年までに350万人のサイバーセキュリティ人材が不足すると予測)により、保守および遠隔監視契約が増加し、北米の産業用制御システム業界の経常収益が上昇しています。

- PLCは2024年に北米の産業用制御システム市場の31.4%を占め、決定論的制御と実証済みの信頼性が評価されました。RockwellのLogixコントローラファミリーは、この地域の自動車および食品ラインの基盤となっています。ベンダーは現在、ネイティブCIPセキュリティとTLS暗号化を備えたPLCを出荷しており、ゲートウェイへの依存度を低減しています。

- 製造業者がロットレベルの系図とオーダーからバッチへの同期を求める中、MESプラットフォームは年平均成長率7.6%で拡大しています。インダストリー4.0の展開により、2024年には世界の接続デバイス数がほぼ倍増し、170億台に達すると予想されています。これにより、MESが実用的な生産KPIに変換するデータセットが作成されます。自動車OEMは、ロボット塗装、バッテリー組立、最終検査の連携にMESを活用し、発売サイクルの短縮と企業資源計画(ERP)の連携を実現しています。

- 北米の産業用制御システム市場レポートは、コンポーネント(ハードウェア、ソフトウェア、サービス)、システムの種類(監視制御・データ収集システム、分散制御システムなど)、通信プロトコル(フィールドバス、産業用イーサネット、ワイヤレス)、導入形態(オンプレミス、クラウド、ハイブリッド)、エンドユーザー産業、および地域別にセグメント化されています。

NA ICS Market Analysis

The North American industrial control systems market size stands at USD 47.77 billion in 2025 and is projected to reach USD 63.38 billion by 2030, reflecting a 5.48% CAGR. Hardware retains the largest revenue share at 57.2% in 2024, underpinned by steady investment in PLCs, distributed control hardware, and I/O modules. Demand is reinforced by the U.S. CHIPS Act, which has mobilized USD 450 billion of announced semiconductor capacity investments, easing component shortages and spurring new automation roll-outs. Industrial Ethernet accounted for 48.9% of installed communications in 2024, while wireless protocols advanced at a 10.4% CAGR as plants sought flexible connectivity. Although cloud deployments are expanding at 9.31% CAGR, 81% of installations remain on-premise because of latency-sensitive control loops and strict security policies. Automotive producers captured 18.6% of demand, yet pharmaceuticals are the fastest-growing end user at 9.1% CAGR as quality-by-design mandates intensify.

NA ICS – Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 – 2030)

List of Companies Covered in this Report:

- ABB Ltd.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corp.

- Omron Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Yokogawa Electric Corp.

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Advantech Co. Ltd.

- Eaton Corp. plc

- BandR Industrial Automation GmbH

- Beckhoff Automation GmbH

- FANUC Corp.

- Delta Electronics Inc.

- Hitachi Ltd.

- IDEC Corp.

Segment Analysis

Hardware contributed 57.2% of 2024 revenue, led by sustained orders for PLC racks, DCS nodes, and motor drives. ABB’s Process Automation unit posted USD 6.8 billion of 2024 sales, showing continued appetite for capital equipment. Integration of edge analytics into controllers, such as Honeywell’s ControlEdge PLC with embedded OPC UA and MQTT, is boosting sell-through of premium SKUs.

Services, though smaller, are scaling rapidly at 8.9% CAGR as owners outsource lifecycle support. Rockwell Automation’s Lifecycle Services backlog reached USD 1.70 billion in September 2024, reflecting demand for outcome-based contracts that tie fees to availability gains. Skills shortages—3.5 million cybersecurity roles lacking by 2025—push maintenance and remote-monitoring agreements higher, elevating recurring revenue in the North American industrial control systems industry.

PLCs held 31.4% of the North American industrial control systems market size in 2024, valued for deterministic control and proven reliability. Rockwell’s Logix controller family anchors automotive and food lines across the region. Vendors now ship PLCs with native CIP-Security and TLS encryption, reducing gateway dependencies.

MES platforms are expanding at 7.6% CAGR as manufacturers seek lot-level genealogy and order-to-batch synchronisation. Industry 4.0 roll-outs nearly doubled connected devices to 17 billion globally in 2024, creating data sets that MES converts into actionable production KPIs. Automotive OEMs use MES to coordinate robotic paint, battery assembly, and final inspection, shortening launch cycles and connecting enterprise resource planning.

The North American Industrial Control Systems Market Report is Segmented by Component (Hardware, Software, Services), Type of System (Supervisory Control & Data Acquisition, Distributed Control Systems, and More), Communication Protocol (Fieldbus, Industrial Ethernet, Wireless), Deployment Mode (On-Premise, Cloud, Hybrid), End-User Industry, and Geography. The Market Forecasts are Provided in Terms of Value (USD).