Data Center Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

データセンター用発電機市場は、製品タイプ(ディーゼル、天然ガス、水素およびHVO対応、その他の製品タイプ)、容量(1MW未満、1〜2MW、2MW超)、層タイプ(Tier IおよびII、Tier III、Tier IV)、データセンタータイプ(ハイパースケール、エンタープライズ、コロケーション)、および地域によってセグメント化されています。

Data Center Generator Market is Segmented by Product Type (Diesel, Natural Gas, Hydrogen and HVO-Ready, Other Product Types), Capacity (Less Than 1 MW, 1-2 MW, Greater Than 2 MW), Tier Type (Tier I and II, Tier III, Tier IV), Data Center Type (Hyperscale, Enterprise, Colocation), and Geography.

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 180 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14654 |

データセンター用発電機市場の規模は2026年には79.2億米ドルと推定され、2025年の75.7億米ドルから増加しています。2031年には98.9億米ドルに達すると予測されており、2026年から2031年にかけて4.56%のCAGRで成長します。この着実な成長は、ハイパースケール施設の急増と、ラック密度をメガワット範囲に押し上げ、バックアップ電源の設計を根本的に変えている人工知能クラスターの新しい波に根ざしています。ディーゼルユニットは依然としてほとんどの設備の基盤となっていますが、炭素削減政策、不安定な燃料価格、およびより厳格なTier 4規則により、天然ガス、水素、およびHVO対応プラットフォームへの関心が高まっています。大口径エンジンのサプライチェーン不足により納入サイクルが長期化しているため、事業者は複数年にわたるフレームワーク契約を締結するか、地域の組立拠点から出荷されるモジュラーブロックに方向転換することを余儀なくされています。一方、銅価格が記録的な高値に達したことでオルタネーターの製造コストが圧迫され、OEM各社は垂直統合の強化と、技術要件が許す範囲でのアルミ巻線の代替を進めています。そのため、競争圧力は単なる馬力重視から、燃料の柔軟性、排出ガス規制への適合、そして予知保全分析によって発電機の稼働状態を保証するデジタルサービス提供といった、より幅広い要素へと移行しつつあります。

セグメント分析

- ディーゼル発電は2025年の需要の81.25%を占める見込みですが、事業者が炭素排出削減義務を財務的に定量化する中で、その供給余地は限定的です。ディーゼル発電ソリューション向けデータセンター発電機市場は、より厳格な割当量が導入される2028年以降、わずかに拡大した後、横ばいになると予測されています。水素およびHVO対応プラットフォームは、小規模ながらも、即時のドロップイン互換性と政府の税額控除に後押しされ、驚異的な成長を見せています。欧州のガスグリッドで1%混合燃料が一般的になるにつれ、水素対応ユニットのデータセンター用発電機市場シェアは着実に増加すると予測されています。

- 規制上のインセンティブが市場の流れをさらに後押ししています。ドイツの494号財政支援策は、グリーンバックアップ電源の改修に5億5,000万ユーロを充当し、メタンと水素の混合燃料に自動調整するデュアル燃料エンジンへの注文を集中させています。同時に、ハイパースケーラーは再生可能ディーゼルのオフテイク契約を締結し、2030年までの価格見通しを確保しています。メーカーは、燃料特性の変化に応じて噴射マップを再調整する無線ファームウェアアップデートで対応し、エンジン寿命を延ばし、バイオディーゼルによる汚染から保証を保護しています。このように、ディーゼルはエネルギー密度と普遍的な入手可能性という点で依然として重要ですが、代替燃料がイノベーションの注目を集めています。

- 1MW未満のユニットは、数千もの小規模エッジサイトでローカルコンテンツ配信を保証する必要があるため、依然として主流です。しかし、ハイパースケール化の合理化により、2MWを超える単一ブロック定格の需要が加速しています。データセンター用発電機市場における2MW以上のセグメントは、年率13.78%の成長が見込まれ、2031年には長年リーダーであった1MW未満のセグメントとほぼ同等の成長率を達成すると予測されています。事業者は、エンジン数が少ないことで燃料物流が簡素化され、スペアパーツの在庫が減り、敷地面積が縮小されるため、これらの大型フレームを好みます。これは、沿岸光ファイバー着陸地点近くの高コストの土地では重要な考慮事項です。

- OEMは、スイッチギアとコントローラーを事前に配線するモジュール式の工場受入試験ブースを導入することで、サプライチェーンの混雑に対処し、現場での試運転を10日以内に完了させます。レンタルフリートプロバイダーは、納入ギャップを埋めるために1~2MWのポートフォリオを同時に拡大しています。契約には、固定機器の出荷後に購入オプションが含まれることがよくあります。このようなフレックス モデルにより、資本予算を予測可能に保ち、事前設定された日付までにラックの準備が整うことを約束するコロケーション契約における遅延ペナルティを回避できます。

- データセンター発電機市場は、製品タイプ(ディーゼル、天然ガス、水素およびHVO対応、その他の製品タイプ)、容量(1MW未満、1~2MW、2MW超)、ティアタイプ(ティアIおよびII、ティアIII、ティアIV)、データセンタータイプ(ハイパースケール、エンタープライズ、コロケーション)、および地域別にセグメント化されています。市場予測は金額(米ドル)で提供されます。

Data Center Generator Market Analysis

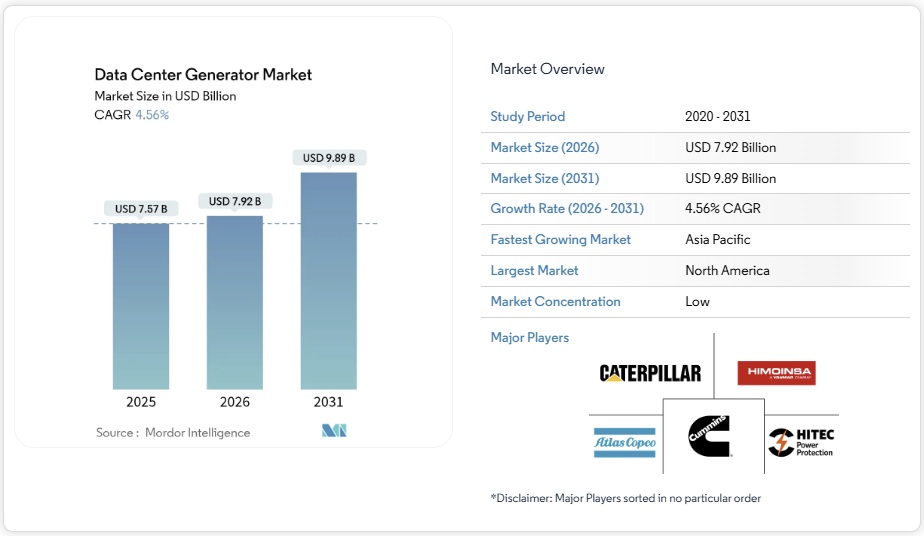

The data center generator market size in 2026 is estimated at USD 7.92 billion, growing from 2025 value of USD 7.57 billion with 2031 projections showing USD 9.89 billion, growing at 4.56% CAGR over 2026-2031. This steady climb is rooted in the surge of hyperscale facilities and the new wave of artificial-intelligence clusters that now push rack densities into the megawatt range, fundamentally transforming backup-power design. Diesel units still anchor most installations, but carbon-reduction policies, volatile fuel prices, and stricter Tier 4 rules accelerate interest in natural-gas, hydrogen, and HVO-ready platforms. Supply-chain shortages for large-bore engines lengthen delivery cycles, prompting operators to lock in multi-year framework agreements or pivot toward modular blocks shipped from regional assembly hubs. Meanwhile, copper prices at record highs squeeze alternator manufacturing costs, driving OEMs to intensify vertical-integration moves and to substitute aluminum windings where technical requirements allow. Competitive pressure is therefore shifting from pure horsepower to a broader mix of fuel flexibility, emissions compliance, and digital service offerings that guarantee a generator’s readiness with predictive maintenance analytics.

Global Data Center Generator Market Trends and Insights

Surging Hyperscale and Colocation Build-out

Hyperscale projects now regularly exceed 100 MW, forcing operators to aggregate dozens of 2.5 MW units into N+2 rings that guarantee uptime during grid loss. In 2024, Google earmarked USD 5 billion to lift Singapore capacity by 35%, translating into more than 150 MW of incremental standby generation Colocation specialists mirror that scale, exemplified by a 150 MW campus under Princeton Digital Group in Malaysia designed with parallel switchgear lineups to streamline load-shed sequencing. Contract structures increasingly bundle genset supply, commissioning, and long-term service to curb lead-time risk and price volatility. As hyperscale pipelines swell, OEMs strengthen local assembly bases in Southeast Asia and the U.S. Midwest to reduce logistics bottlenecks and to align with domestic-content incentives.

Rising Rack-Power Densities from AI Workloads

GPU-rich racks that consume up to 1 MW each compress the safety margin of legacy generator fleets, prompting capacity re-rating or wholesale replacement. Cummins posted a 19% jump in Power Systems revenue in Q1-2025, attributing the rise to AI-driven data center orders . Operators now specify tighter voltage-regulation bands and dynamic-response times below 10 seconds to protect thousands of interconnected accelerators that cannot tolerate brownouts. Generator skids therefore integrate larger alternators, active harmonic filters, and liquid-cooling circuits that dissipate elevated stator heat. Firmware upgrades also enable real-time synchronization with flywheel UPS buffers, ensuring seamless transition when grid events occur.

Carbon-Emission Regulations Targeting Diesel Gensets

California’s Air Resources Board limits non-emergency runtime and enforces real-time monitoring, compelling operators to fit costly SCR and particulate-filter stacks. In the European Union, the Industrial Emissions Directive intensifies permitting scrutiny, delaying approvals by up to 14 months for diesel-heavy campuses. Compliance lifts lifecycle ownership costs as exhaust-after-treatment parts must be replaced every 15,000 engine hours. Some campuses respond by relocating backup yards to less-regulated jurisdictions, yet that strategy collides with latency-sensitive user demands, keeping pressure on OEMs to innovate cleaner combustion or hybrid solutions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Edge Data Centers in Emerging Markets

- Transition to Natural-Gas and HVO Gensets for Sustainability

- Shift Toward Battery and Fuel-Cell Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diesel sets anchored 81.25% of 2025 demand, yet their headroom is capped as operators quantify carbon liabilities in financial terms. The data center generator market size for diesel solutions is projected to expand marginally before plateauing post-2028 once stricter quotas lock in. Hydrogen and HVO-ready platforms, though starting from a small base, exhibit outlier growth, propelled by immediate drop-in compatibility and government tax credits. The data center generator market share for hydrogen-ready units is forecast to climb steadily as 1% blends become commonplace in European gas grids.

Regulatory incentives further tilt momentum. Germany’s funding line 494 directs EUR 550 million toward green backup power retrofits, funneling orders toward dual-fuel engines that self-calibrate to methane-hydrogen blends. Simultaneously, hyperscalers sign offtake agreements for renewable diesel to lock price visibility through 2030. Manufacturers respond with over-the-air firmware updates that retune injection maps when fuel properties shift, prolonging engine life and protecting warranties against biodiesel contamination. Diesel therefore remains critical for its energy density and universal availability, but alternative fuels capture the innovation spotlight.

Less than 1 MW units retain dominance because thousands of small edge sites must guarantee local content delivery. However, hyperscale rationalization accelerates demand for single-block ratings beyond 2 MW. Greater than 2 MW slice of the data center generator market is forecast to compound at 13.78% annually, and by 2031 it will nearly equal the long-time less than 1 MW leader. Operators favor these larger frames because fewer engines simplify fuel logistics, reduce spares inventory, and shrink the real-estate footprint—an important consideration on high-cost plots near coastal fiber landings.

OEMs tackle supply-chain congestions with modular factory-acceptance testing booths that pre-wire switchgear and controllers so that field commissioning falls below 10 days. Rental-fleet providers simultaneously grow their 1-2 MW portfolio to bridge delivery gaps; contracts often include a purchase option once permanent gear ships. Such flex models keep capital budgets predictable and guard against late penalties in colocation contracts that promise rack readiness by preset dates.

Data Center Generator Market is Segmented by Product Type (Diesel, Natural Gas, Hydrogen and HVO-Ready, Other Product Types), Capacity (Less Than 1 MW, 1-2 MW, Greater Than 2 MW), Tier Type (Tier I and II, Tier III, Tier IV), Data Center Type (Hyperscale, Enterprise, Colocation), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America claimed 40.55% of 2025 revenue on the strength of dense data center corridors in Northern Virginia, Dallas, and Phoenix. Investment now centers on power-density upgrades rather than new land acquisition; operators swap aging 2 MW diesels for 3.5 MW Tier 4-Final models to unlock white-space without expanding walls. Federal production tax credits for hydrogen and biogas further sweeten the switch to low-carbon gensets.

Asia-Pacific showcases the strongest momentum with a 10.42% CAGR through 2031. Singapore lifts its moratorium on data center permits in return for efficiency pledges, unlocking a pipeline of 300 MW across five projects. India’s Digital Personal Data Protection Act fuels domestic cloud builds, with Mumbai alone planning 700 MW of fresh IT load. In Japan, SoftBank’s 300 MW Hokkaido campus integrates hydro-backed grids but still specifies dual-fuel backup to counter seismic-related outages. Meanwhile, Malaysia and Indonesia emerge as cost-competitive hubs by offering land concessions and renewable-energy certificates tailored to hyperscalers. Europe ranks third in absolute value but leads in sustainability mandates. Amsterdam’s municipality now caps diesel runtime and levies CO₂ fees above 500 t/year, nudging operators toward gas engines and battery hybrids. Dublin’s grid-capacity crunch pushes developers to Spain and Portugal, thereby redistributing generator demand southward. The Middle East leverages abundant natural gas and solar resources; Dubai’s Digital Park installs gas-fired gensets with absorption chillers that recycle waste heat into district-cooling loops. Africa remains early-stage yet promising, with Nairobi and Lagos deploying micro-modular data centers backed by 400 kVA diesels to overcome unreliable grids.

List of Companies Covered in this Report:

- Caterpillar Inc.

- Cummins Inc.

- Generac Power Systems Inc.

- Rolls-Royce plc (mtu Solutions)

- Kohler Co.

- Mitsubishi Heavy Industries Group

- Atlas Copco AB

- Himoinsa SL

- Aksa Power Generation

- HITEC Power Protection BV

- INNIO Group (Jenbacher/Waukesha)

- Aggreko Ltd.

- Wartsila Corp.

- ABB Ltd.

- Doosan Enerbility Co., Ltd.

- FG Wilson

- Yanmar Holdings Co., Ltd.

- Perkins Engines Co. Ltd.

- Briggs & Stratton LLC

- Baudouin (Weichai)

- HIPOWER SYSTEMS

- GE Vernova

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Surging hyperscale and colocation build-out

4.2.2 Rising rack-power densities from AI workloads

4.2.3 Expansion of edge data centers in emerging markets

4.2.4 Transition to natural-gas and HVO gensets for sustainability

4.2.5 Deployment of trailer-mounted temporary generation fleets

4.2.6 Adoption of modular micro-grid-ready generator blocks

4.3 Market Restraints

4.3.1 Carbon-emission regulations targeting diesel gensets

4.3.2 Shift toward battery and fuel-cell alternatives

4.3.3 High-horsepower engine supply-chain bottlenecks

4.3.4 Urban permitting hurdles on noise and air quality

4.4 Value / Supply-Chain Analysis

4.5 Regulatory Landscape

4.6 Technological Outlook

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

5.1 By Product Type

5.1.1 Diesel

5.1.2 Natural Gas

5.1.3 Hydrogen and HVO-Ready

5.1.4 Other Product Types

5.2 By Capacity

5.2.1 Less than 1 MW

5.2.2 1 – 2 MW

5.2.3 Greater than 2 MW

5.3 By Tier Type

5.3.1 Tier I and II

5.3.2 Tier III

5.3.3 Tier IV

5.4 By Data Center Type

5.4.1 Hyperscale (Owned and Leased)

5.4.2 Enterprise (On-premise)

5.4.3 Colocation

5.5 By Geography

5.5.1 North America

5.5.2 South America

5.5.3 Europe

5.5.4 Asia-Pacific

5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Share Analysis

6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

6.2.1 Caterpillar Inc.

6.2.2 Cummins Inc.

6.2.3 Generac Power Systems Inc.

6.2.4 Rolls-Royce plc (mtu Solutions)

6.2.5 Kohler Co.

6.2.6 Mitsubishi Heavy Industries Group

6.2.7 Atlas Copco AB

6.2.8 Himoinsa SL

6.2.9 Aksa Power Generation

6.2.10 HITEC Power Protection BV

6.2.11 INNIO Group (Jenbacher/Waukesha)

6.2.12 Aggreko Ltd.

6.2.13 Wartsila Corp.

6.2.14 ABB Ltd.

6.2.15 Doosan Enerbility Co., Ltd.

6.2.16 FG Wilson

6.2.17 Yanmar Holdings Co., Ltd.

6.2.18 Perkins Engines Co. Ltd.

6.2.19 Briggs & Stratton LLC

6.2.20 Baudouin (Weichai)

6.2.21 HIPOWER SYSTEMS

6.2.22 GE Vernova

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-space and Unmet-Need Assessment