データセンター建設市場レポート : 建設タイプ(電気工事、機械工事)、データセンタータイプ(中規模データセンター、エンタープライズデータセンター、大規模データセンター)、ティア標準(ティアIおよびII、ティアIII、ティアIV)、垂直(公共部門、石油・エネルギー、メディア・エンターテイメント、IT・通信、銀行、金融サービス・保険(BFSI)、ヘルスケア、小売、その他)、および地域 2026-2034年

Data Center Construction Market Report by Construction Type (Electrical Construction, Mechanical Construction), Data Center Type (Mid-Size Data Centers, Enterprise Data Centers, Large Data Centers), Tier Standards (Tier I & II, Tier III, Tier IV), Vertical (Public Sector, Oil and Energy, Media and Entertainment, IT and Telecommunication, Banking, Financial Services and Insurance (BFSI), Healthcare, Retail, and Others), and Region 2026-2034

| 出版 | IMARC Group |

| 出版年月 | 2026年02月 |

| ページ数 | 148 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 3,999 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-14698 |

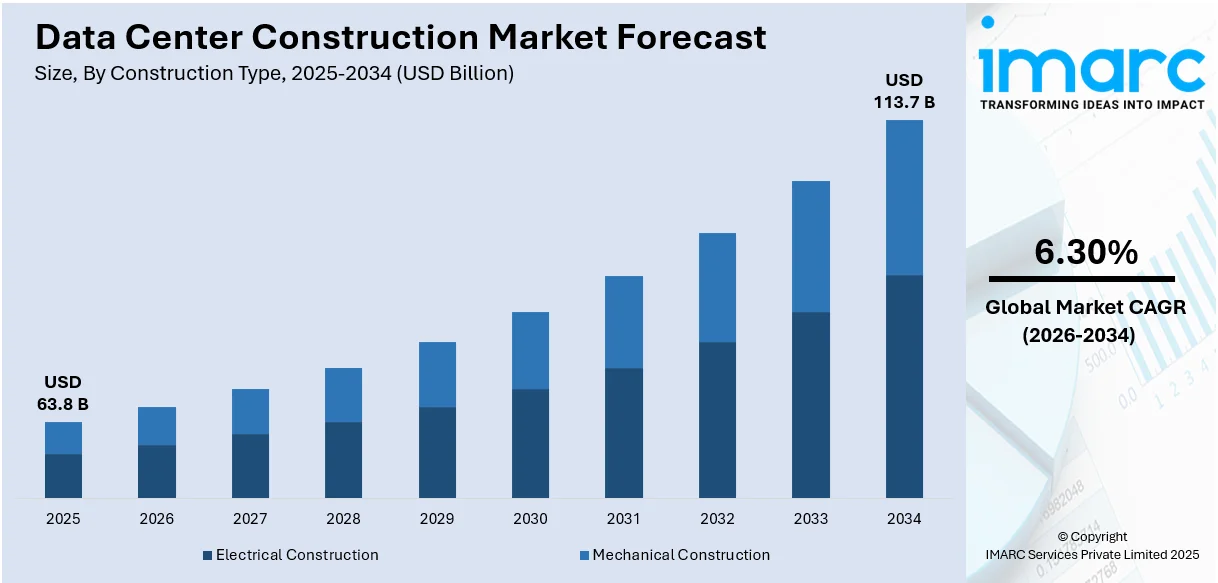

世界のデータセンター建設市場規模は、2025年に638億米ドルに達しました。IMARCグループは、今後、市場規模が2034年までに1,137億米ドルに達し、2026年から2034年にかけて6.30%の成長率(CAGR)を示すと予測しています。堅牢なデジタルインフラに対する需要の高まりと、様々な地域における効率性、信頼性、持続可能性の向上を目的とした電気・機械設備への投資増加は、市場の成長を牽引する要因の一つです。

データセンター建設市場分析:

- 主要な市場牽引要因:データストレージとクラウドベースのサービスに対する需要の高まりにより、市場は緩やかな成長を遂げています。さらに、5G、人工知能(AI)、モノのインターネット(IoT)といった技術革新により、より大規模で高度なデータセンターへの需要が高まっています。

- 主要な市場動向:多くの企業が環境に配慮した建設手法やエネルギー効率の高い設計を優先するなど、持続可能性への関心が高まっており、市場見通しは良好です。これには、環境への影響を軽減するための最先端の冷却システムの導入や再生可能エネルギー源への切り替えが含まれます。

- 地域動向:テクノロジー企業の集中化とクラウドサービスの早期導入により、北米が市場を牽引しています。

- 競争環境:データセンター建設業界の主要企業には、AECOM、Clark Construction Group, LLC、Collen Construction、Corgan、DPR Construction、Holder Construction Group, LLC、ISG、Jacobs Solutions Inc.、Linesight、Mercury Engineering、PCL Constructors Inc、Turner Construction Companyなど、数多くあります。

- 課題と機会:最先端のデータセンターの建設と維持に伴う高コストは、データセンター建設市場の収益に影響を与えています。しかしながら、従来のデータセンターと比較して迅速かつ低コストで設置可能なモジュラー型データセンターを専門とする企業には、市場の成長を支える機会があります。

Report Overview

The global data center construction market size reached USD 63.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 113.7 Billion by 2034, exhibiting a growth rate (CAGR) of 6.30% during 2026-2034. The escalating demand for robust digital infrastructure and rising investments in electrical and mechanical construction to enhance efficiency, reliability, and sustainability across various regions are some of the factors impelling the market growth.

data-center-construction-market-size

Data Center Construction Market Analysis:

- Major Market Drivers: The market is experiencing moderate growth because of the rising demand for data storage and cloud-based services. Furthermore, the demand for larger and more advanced data centers is being driven by technological breakthroughs like 5G, artificial intelligence (AI), and the Internet of Things (IoT).

- Key Market Trends: The growing focus on sustainability, as many companies prioritize green construction practices and energy-efficient designs, is offering a favorable market outlook. This involves using cutting-edge cooling systems and switching to renewable energy sources in order to lessen the impact on the environment.

- Geographical Trends: North America dominates the market attributed to the increasing concentration of technology companies and early adoption of cloud services in the region.

- Competitive Landscape: Some of the major market players in the data center construction industry include AECOM, Clark Construction Group, LLC, Collen Construction, Corgan, DPR Construction, Holder Construction Group, LLC, ISG, Jacobs Solutions Inc., Linesight, Mercury Engineering, PCL Constructors Inc, Turner Construction Company, among many others.

- Challenges and Opportunities: The high costs associated with constructing and maintaining state-of-the-art data centers are influencing the data center construction market revenue. Nevertheless, opportunities for companies specializing in modular data centers, which can be set up more quickly and at a reduced expense in comparison to conventional data centers, is supporting the market growth.

Data Center Construction Market Trends:

Sustainability Initiatives and Regulatory Compliance

Efforts to promote sustainability and stringent regulatory demands play a key role in shaping the data center construction market. There is a noticeable shift towards green data centers, utilizing renewable energy and efficient cooling to reduce carbon footprints, as environmental issues become more prominent. Laws concerning energy efficiency and environmental effects are becoming more stringent, leading businesses to focus on sustainable construction methods and technologies. This trend not only lowers operational expenses of companies but also improves their reputation for corporate social responsibility (CSR). In November 2023, Vertiv Group Corporation introduced TimberMod, a modular data center made mostly of wood to lower carbon footprints and meet sustainability goals. Despite initial skepticism, timber data centers have been proven to be resilient and able to withstand fires, aligning with the industry’s sustainability objectives. Furthermore, Fujitsu is at the forefront of creating energy-efficient CPUs and photonics smart NIC for future green data centers as part of Japan’s NEDO program in February 2022. The goal of the project is to make substantial energy reductions in data centers by 2030, helping create an eco-friendly digital infrastructure.

Technological Advancements and Infrastructure Demand

The use of fiber optics and faster networking technologies requires data centers to be redesigned and built to accommodate higher data traffic and offer high-speed connectivity. The increasing dependence of businesses on AI, machine learning (ML), and blockchain technology is driving the demand for advanced data centers that can handle intensive computational tasks and offer extensive storage capacities. For instance, in February 2024, Eaton Corporation Inc. introduced its SmartRack modular data center, offering quick deployment in days, catering to the rising demand for edge computing and AI. Created for different buildings, it can handle a load of up to 150kW of equipment and incorporates cooling systems, in line with Eaton’s complete power management solutions. Moreover, attempts to vary the sites of data centers to uphold data sovereignty and reduce latency are leading to an increase in construction projects across various locations. These elements ensure a continual demand for cutting-edge data center solutions that can support future technological advancements.

Increasing Cybersecurity Concerns

Growing concerns about cybersecurity are encouraging businesses to increase their investment in secure and strong data center infrastructures. The Identity Theft Resource Center report in 2023 claimed that 343,338,964 people were the victims of 2,365 cyberattacks in 2023. Data breaches and cyber-attacks are on a rise, causing companies to focus on building data centers with enhanced security features. This consists of improvements in physical security such as biometric access controls and defenses in cyberspace like firewalls and intrusion detection systems. Industries such as finance, healthcare, and government have a high need for highly secure data storage and processing facilities to safeguard sensitive information.

Data Center Construction Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Construction Types Covered | Electrical Construction, Mechanical Construction |

| Data Center Types Covered | Mid-Size Data Centers, Enterprise Data Centers, Large Data Centers |

| Tier Standards Covered | Tier I & II, Tier III, Tier IV |

| Verticals Covered | Public Sector, Oil and Energy, Media and Entertainment, IT and Telecommunication, Banking, Financial Services and Insurance (BFSI), Healthcare, Retail, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Turkey, Saudi Arabia |

| Companies Covered | AECOM, Clark Construction Group, LLC, Collen Construction, Corgan, DPR Construction, Holder Construction Group, LLC, ISG, Jacobs Solutions Inc., Linesight, Mercury Engineering, PCL Constructors Inc, Turner Construction Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Data Center Construction Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional and country levels for 2026-2034. Our report has categorized the market based on construction type, data center type, tier standards and vertical.

Breakup by Construction Type:

- Electrical Construction

- Mechanical Construction

Electrical construction represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the construction type. This includes electrical construction and mechanical construction. According to the report, electrical construction represented the largest segment.

Electrical construction is the largest sector due to the increased need for reliable power distribution systems, backup generators, and connectivity solutions in data centers. This part is crucial for ensuring a steady power supply and managing the high electricity demands of modern data centers that house large server arrays and cooling systems. As data centers increase in size and complexity, the electrical infrastructure must advance to prevent interruptions and maintain operational consistency. Advancements in energy-efficient power solutions, modular power units, and smart grid technology are important factors propelling the data center construction demand in this sector, demonstrating the industry’s commitment to lowering energy usage and promoting sustainability. The worldwide smart grid market size was valued at US$ 63.0 billion in 2023. The IMARC Group projects the market will reach US$ 253.5 billion by 2032. Furthermore, increasing technological advancements and rising investments in data center operations are enhancing the dominant position of the electrical construction industry, underscoring the crucial need for achieving optimal energy efficiency and dependability.

Breakup by Data Center Type:

- Mid-Size Data Centers

- Enterprise Data Centers

- Large Data Centers

Large data centers exhibit a clear dominance in the market

A detailed breakup and analysis of the market based on the data center type has also been provided in the report. This includes mid-size data centers, enterprise data centers, and large data centers. According to the report, large data centers accounted for the largest market share.

Large data centers take up the significant portion, mainly serving big corporations, cloud providers, and big internet companies. These facilities are built to manage large amounts of data, providing significant computational power and storage capabilities that surpass those of smaller installations. The expansion of this sector is driven by the growing dependence on advanced data analysis and large-scale cloud services that demand strong, flexible infrastructure. Large data centers are frequently at the forefront of embracing new technologies like advanced cooling mechanisms, energy efficiency solutions, and automation powered by AI to improve efficiency and sustainability. Their large size also helps achieve notable cost savings, resulting in more efficient information technology (IT) resource management in the long run, ultimately enhancing the data center construction market value.

Breakup by Tier Standards:

- Tier I & II

- Tier III

- Tier IV

Tier III dominates the market

The report has provided a detailed breakup and analysis of the market based on the tier standards. This includes tier I and II, tier III, and tier IV. According to the report, tier III represented the largest segment.

Tier III data centers are the top players within the tier standards in the market. This is mainly due to their ability to find a perfect equilibrium between affordability and dependability, rendering them extremely appropriate for various businesses. These data centers provide a high level of redundancy and fault tolerance, guaranteeing at least N+1 availability so that any part can be shut down for maintenance without affecting IT functions. Furthermore, tier III data centers are designed with durability and availability as top priorities and are commonly used by big corporations and companies. Additionally, they achieve equilibrium between dependability and affordability, which makes them an appealing option for businesses seeking a budget-friendly solution that does not sacrifice uptime. In addition, these data centers provide various power and cooling distribution paths, like one active and one passive, to facilitate maintenance without interrupting operations. They include a variety of redundant components, such as uninterruptible power supply (UPS) systems, backup generators, and advanced cooling mechanisms. In 2023, the market for uninterrupted power supply (UPS) systems was valued at US$ 8.1 billion. The IMARC Group projects that the market would grow to US$ 12.3 billion by 2032.

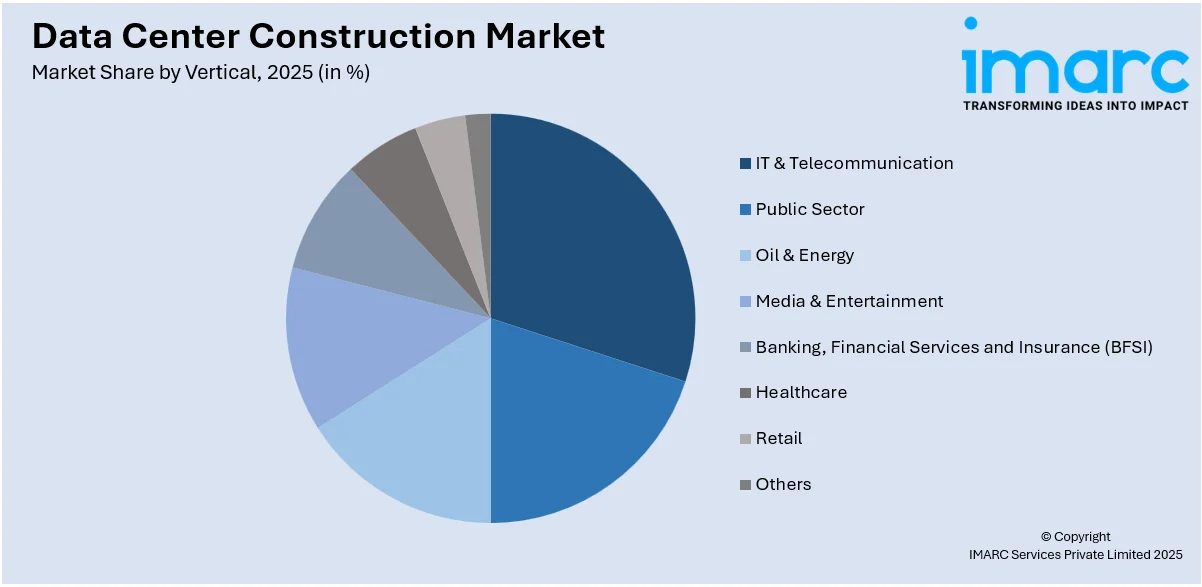

Breakup by Vertical:

- Public Sector

- Oil & Energy

- Media & Entertainment

- IT & Telecommunication

- Banking, Financial Services and Insurance (BFSI)

- Healthcare

- Retail

- Others

IT and telecommunication are the predominant market segment

A detailed breakup and analysis of the market based on the vertical has also been provided in the report. This includes public sector, oil and energy, media and entertainment, IT and telecommunication, banking, financial services and insurance (BFSI), healthcare, retail, and others. According to the report, IT and telecommunication accounted for the largest market share.

IT and telecommunication are the largest segment, driven by the relentless expansion of data communication and storage needs within these industries. As telecommunications companies and IT service providers grapple with the massive influx of data from increased internet usage, cloud computing, and mobile services, they are heavily investing in building robust data center infrastructures. This segment is characterized by a high demand for cutting-edge data center solutions that ensure high-speed connectivity, maximum uptime, and stringent security measures. The shift towards digital transformation, necessitating substantial data processing and storage capabilities to support new technologies like 5G, IoT, and smart technology solutions is supporting the data center construction market growth. In 2023, the size of the global IoT market was estimated to be US$ 887.6 billion. The IMARC Group projects that the market would expand at a compound annual growth rate (CAGR) of 15.21% from 2024 to 2032, reaching US$ 3,174.2 billion in 2032.

Breakup by Region:

- North America

o United States

o Canada

- Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

o Indonesia

o Others

- Europe

o Germany

o France

o United Kingdom

o Italy

o Spain

o Russia

o Others

- Latin America

o Brazil

o Mexico

o Others

- Middle East and Africa

o Turkey

o Saudi Arabia

o Others

North America leads the market, accounting for the largest data center construction market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa (Turkey, Saudi Arabia, Others). According to the report, North America represents the largest regional market for data center construction.

North America, particularly the United States and Canada, represents the largest segment as per the data center construction market overview, owing largely to the early and extensive adoption of cloud technologies and the presence of major tech giants. The region benefits from advanced infrastructure, high technology penetration, and robust regulatory frameworks that support large-scale data operations. Growing investments in upgrading and expanding existing data centers, coupled with a focus on sustainability and energy efficiency, are further supporting the growth in this region. According to the IMARC Group, the data center construction market in the United States is expected to increase at a compound annual growth rate (CAGR) of 5.94% between 2024 and 2032. This innovative solution enhances efficiency and saves labor, catering to the growing demand for faster and more adaptable data center construction in the USA. Besides this, the rising adoption of digital financial services is catalyzing the demand for secure and efficient data centers to handle the rising volume of financial transactions and data in the region.

Competitive Landscape:

Key players are intensively focusing on integrating advanced technologies, such as AI machine learning (ML), and IoT to enhance the efficiency and sustainability of data centers. These major companies are investing in research and development (R&D) to pioneer energy-efficient construction methods, including the use of renewable energy sources and advanced cooling systems to reduce carbon footprints. Additionally, they are expanding their geographical presence through strategic alliances and acquisitions to capitalize on emerging growth potential of markets. In December 2023, Vertiv Group Corporation acquired CoolTera, a UK-based liquid cooling business specializing in coolant distribution units (CDUs) and secondary fluid networks (SFN). This acquisition strengthened expertise of Vertiv in high-density cooling solutions and positioned the company to better serve global data center users, particularly in supporting AI deployment at scale. Moreover, the competitive landscape is also seeing a rise in the provision of modular data centers, which offer scalability and rapid deployment benefits.

The report provides a comprehensive analysis of the competitive landscape in the global data center construction market with detailed profiles of all major companies, including:

- AECOM

- Clark Construction Group, LLC

- Collen Construction

- Corgan

- DPR Construction

- Holder Construction Group, LLC

- ISG

- Jacobs Solutions Inc.

- Linesight

- Mercury Engineering

- PCL Constructors Inc

- Turner Construction Company

Key Questions Answered in This Report

1.What was the size of the global data center construction market in 2025?

2.What is the expected growth rate of the global data center construction market during 2026-2034?

3.What are the key factors driving the global data center construction market?

4.What has been the impact of COVID-19 on the global data center construction market?

5.What is the breakup of the global data center construction market based on the construction type?

6.What is the breakup of the global data center construction market based on the data center type?

7.What is the breakup of the global data center construction market based on the tier standards?

8.What is the breakup of the global data center construction market based on the vertical?

9.What are the key regions in the global data center construction market?

10.Who are the key players/companies in the global data center construction market?

Table of Contents

1 Preface

2 Scope and Methodology

2.1 Objectives of the Study

2.2 Stakeholders

2.3 Data Sources

2.3.1 Primary Sources

2.3.2 Secondary Sources

2.4 Market Estimation

2.4.1 Bottom-Up Approach

2.4.2 Top-Down Approach

2.5 Forecasting Methodology

3 Executive Summary

4 Introduction

4.1 Overview

4.2 Key Industry Trends

5 Global Data Center Construction Market

5.1 Market Overview

5.2 Market Performance

5.3 Impact of COVID-19

5.4 Market Forecast

6 Market Breakup by Construction Type

6.1 Electrical Construction

6.1.1 Market Trends

6.1.2 Market Breakup by Component Type

6.1.3 Market Forecast

6.2 Mechanical Construction

6.2.1 Market Trends

6.2.2 Market Breakup by Component Type

6.2.3 Market Forecast

7 Market Breakup by Data Center Type

7.1 Mid-Size Data Centers

7.1.1 Market Trends

7.1.2 Market Forecast

7.2 Enterprise Data Centers

7.2.1 Market Trends

7.2.2 Market Forecast

7.3 Large Data Centers

7.3.1 Market Trends

7.3.2 Market Forecast

8 Market Breakup by Tier Standards

8.1 Tier I & II

8.1.1 Market Trends

8.1.2 Market Forecast

8.2 Tier III

8.2.1 Market Trends

8.2.2 Market Forecast

8.3 Tier IV

8.3.1 Market Trends

8.3.2 Market Forecast

9 Market Breakup by Vertical

9.1 Public Sector

9.1.1 Market Trends

9.1.2 Market Forecast

9.2 Oil & Energy

9.2.1 Market Trends

9.2.2 Market Forecast

9.3 Media & Entertainment

9.3.1 Market Trends

9.3.2 Market Forecast

9.4 IT & Telecommunication

9.4.1 Market Trends

9.4.2 Market Forecast

9.5 Banking, Financial Services and Insurance (BFSI)

9.5.1 Market Trends

9.5.2 Market Forecast

9.6 Healthcare

9.6.1 Market Trends

9.6.2 Market Forecast

9.7 Retail

9.7.1 Market Trends

9.7.2 Market Forecast

9.8 Others

9.8.1 Market Trends

9.8.2 Market Forecast

10 Market Breakup by Region

10.1 North America

10.1.1 United States

10.1.1.1 Market Trends

10.1.1.2 Market Forecast

10.1.2 Canada

10.1.2.1 Market Trends

10.1.2.2 Market Forecast

10.2 Asia Pacific

10.2.1 China

10.2.1.1 Market Trends

10.2.1.2 Market Forecast

10.2.2 Japan

10.2.2.1 Market Trends

10.2.2.2 Market Forecast

10.2.3 India

10.2.3.1 Market Trends

10.2.3.2 Market Forecast

10.2.4 South Korea

10.2.4.1 Market Trends

10.2.4.2 Market Forecast

10.2.5 Australia

10.2.5.1 Market Trends

10.2.5.2 Market Forecast

10.2.6 Indonesia

10.2.6.1 Market Trends

10.2.6.2 Market Forecast

10.2.7 Others

10.2.7.1 Market Trends

10.2.7.2 Market Forecast

10.3 Europe

10.3.1 Germany

10.3.1.1 Market Trends

10.3.1.2 Market Forecast

10.3.2 France

10.3.2.1 Market Trends

10.3.2.2 Market Forecast

10.3.3 United Kingdom

10.3.3.1 Market Trends

10.3.3.2 Market Forecast

10.3.4 Italy

10.3.4.1 Market Trends

10.3.4.2 Market Forecast

10.3.5 Spain

10.3.5.1 Market Trends

10.3.5.2 Market Forecast

10.3.6 Russia

10.3.6.1 Market Trends

10.3.6.2 Market Forecast

10.3.7 Others

10.3.7.1 Market Trends

10.3.7.2 Market Forecast

10.4 Latin America

10.4.1 Brazil

10.4.1.1 Market Trends

10.4.1.2 Market Forecast

10.4.2 Mexico

10.4.2.1 Market Trends

10.4.2.2 Market Forecast

10.4.3 Others

10.4.3.1 Market Trends

10.4.3.2 Market Forecast

10.5 Middle East and Africa

10.5.1 Turkey

10.5.1.1 Market Trends

10.5.1.2 Market Forecast

10.5.2 Saudi Arabia

10.5.2.1 Market Trends

10.5.2.2 Market Forecast

10.5.3 Others

10.5.3.1 Market Trends

10.5.3.2 Market Forecast

11 SWOT Analysis

11.1 Overview

11.2 Strengths

11.3 Weaknesses

11.4 Opportunities

11.5 Threats

12 Value Chain Analysis

13 Porters Five Forces Analysis

13.1 Overview

13.2 Bargaining Power of Buyers

13.3 Bargaining Power of Suppliers

13.4 Degree of Competition

13.5 Threat of New Entrants

13.6 Threat of Substitutes

14 Price Analysis

15 Competitive Landscape

15.1 Market Structure

15.2 Key Players

15.3 Profiles of Key Players

15.3.1 AECOM

15.3.1.1 Company Overview

15.3.1.2 Product Portfolio

15.3.1.3 Financials

15.3.1.4 SWOT Analysis

15.3.2 Clark Construction Group, LLC

15.3.2.1 Company Overview

15.3.2.2 Product Portfolio

15.3.2.3 Financials

15.3.2.4 SWOT Analysis

15.3.3 Collen Construction

15.3.3.1 Company Overview

15.3.3.2 Product Portfolio

15.3.3.3 Financials

15.3.3.4 SWOT Analysis

15.3.4 Corgan

15.3.4.1 Company Overview

15.3.4.2 Product Portfolio

15.3.4.3 Financials

15.3.4.4 SWOT Analysis

15.3.5 DPR Construction

15.3.5.1 Company Overview

15.3.5.2 Product Portfolio

15.3.5.3 SWOT Analysis

15.3.6 Holder Construction Group, LLC

15.3.6.1 Company Overview

15.3.6.2 Product Portfolio

15.3.7 ISG

15.3.7.1 Company Overview

15.3.7.2 Product Portfolio

15.3.7.3 Financials

15.3.7.4 SWOT Analysis

15.3.8 Jacobs Solutions Inc.

15.3.8.1 Company Overview

15.3.8.2 Product Portfolio

15.3.8.3 Financials

15.3.8.4 SWOT Analysis

15.3.9 Linesight

15.3.9.1 Company Overview

15.3.9.2 Product Portfolio

15.3.9.3 Financials

15.3.9.4 SWOT Analysis

15.3.10 Mercury Engineering

15.3.10.1 Company Overview

15.3.10.2 Product Portfolio

15.3.10.3 Financials

15.3.10.4 SWOT Analysis

15.3.11 PCL Constructors Inc

15.3.11.1 Company Overview

15.3.11.2 Product Portfolio

15.3.11.3 Financials

15.3.11.4 SWOT Analysis

15.3.12 Turner Construction Company

15.3.12.1 Company Overview

15.3.12.2 Product Portfolio

15.3.12.3 Financials

15.3.12.4 SWOT Analysis

List of Tables

Table 1: Global: Data Center Construction Market: Key Industry Highlights, 2025 and 2034

Table 2: Global: Data Center Construction Market Forecast: Breakup by Construction Type (in Million USD), 2026-2034

Table 3: Global: Data Center Construction Market Forecast: Breakup by Data Center Type (in Million USD), 2026-2034

Table 4: Global: Data Center Construction Market Forecast: Breakup by Tier Standards (in Million USD), 2026-2034

Table 5: Global: Data Center Construction Market Forecast: Breakup by Vertical (in Million USD), 2026-2034

Table 6: Global: Data Center Construction Market Forecast: Breakup by Region (in Million USD), 2026-2034

Table 7: Global: Data Center Construction Market: Competitive Structure

Table 8: Global: Data Center Construction Market: Key Players

List of Figures

Figure 1: Global: Data Center Construction Market: Major Drivers and Challenges

Figure 2: Global: Data Center Construction Market: Sales Value (in Billion USD), 2020-2025

Figure 3: Global: Data Center Construction Market Forecast: Sales Value (in Billion USD), 2026-2034

Figure 4: Global: Data Center Construction Market: Breakup by Construction Type (in %), 2025

Figure 5: Global: Data Center Construction Market: Breakup by Data Center Type (in %), 2025

Figure 6: Global: Data Center Construction Market: Breakup by Tier Standards (in %), 2025

Figure 7: Global: Data Center Construction Market: Breakup by Vertical (in %), 2025

Figure 8: Global: Data Center Construction Market: Breakup by Region (in %), 2025

Figure 9: Global: Data Center Construction (Electrical Construction) Market: Sales Value (in Million USD), 2020 & 2025

Figure 10: Global: Data Center Construction Market (Electrical Construction): Breakup by Component Type (in %), 2025

Figure 11: Global: Data Center Construction (Electrical Construction) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 12: Global: Data Center Construction (Mechanical Construction) Market: Sales Value (in Million USD), 2020 & 2025

Figure 13: Global: Data Center Construction Market (Mechanical Construction): Breakup by Component Type (in %), 2025

Figure 14: Global: Data Center Construction (Mechanical Construction) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 15: Global: Data Center Construction (Mid-Size Data Centers) Market: Sales Value (in Million USD), 2020 & 2025

Figure 16: Global: Data Center Construction (Mid-Size Data Centers) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 17: Global: Data Center Construction (Enterprise Data Centers) Market: Sales Value (in Million USD), 2020 & 2025

Figure 18: Global: Data Center Construction (Enterprise Data Centers) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 19: Global: Data Center Construction (Large Data Centers) Market: Sales Value (in Million USD), 2020 & 2025

Figure 20: Global: Data Center Construction (Large Data Centers) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 21: Global: Data Center Construction (Tier I & II) Market: Sales Value (in Million USD), 2020 & 2025

Figure 22: Global: Data Center Construction (Tier I & II) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 23: Global: Data Center Construction (Tier III) Market: Sales Value (in Million USD), 2020 & 2025

Figure 24: Global: Data Center Construction (Tier III) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 25: Global: Data Center Construction (Tier IV) Market: Sales Value (in Million USD), 2020 & 2025

Figure 26: Global: Data Center Construction (Tier IV) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 27: Global: Data Center Construction (Public Sector) Market: Sales Value (in Million USD), 2020 & 2025

Figure 28: Global: Data Center Construction (Public Sector) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 29: Global: Data Center Construction (Oil & Energy) Market: Sales Value (in Million USD), 2020 & 2025

Figure 30: Global: Data Center Construction (Oil & Energy) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 31: Global: Data Center Construction (Media & Entertainment) Market: Sales Value (in Million USD), 2020 & 2025

Figure 32: Global: Data Center Construction (Media & Entertainment) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 33: Global: Data Center Construction (IT & Telecommunication) Market: Sales Value (in Million USD), 2020 & 2025

Figure 34: Global: Data Center Construction (IT & Telecommunication) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 35: Global: Data Center Construction (BFSI) Market: Sales Value (in Million USD), 2020 & 2025

Figure 36: Global: Data Center Construction (BFSI) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 37: Global: Data Center Construction (Healthcare) Market: Sales Value (in Million USD), 2020 & 2025

Figure 38: Global: Data Center Construction (Healthcare) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 39: Global: Data Center Construction (Retail) Market: Sales Value (in Million USD), 2020 & 2025

Figure 40: Global: Data Center Construction (Retail) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 41: Global: Data Center Construction (Other Verticals) Market: Sales Value (in Million USD), 2020 & 2025

Figure 42: Global: Data Center Construction (Other Verticals) Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 43: North America: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 44: North America: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 45: United States: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 46: United States: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 47: Canada: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 48: Canada: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 49: Asia Pacific: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 50: Asia Pacific: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 51: China: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 52: China: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 53: Japan: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 54: Japan: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 55: India: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 56: India: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 57: South Korea: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 58: South Korea: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 59: Australia: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 60: Australia: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 61: Indonesia: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 62: Indonesia: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 63: Others: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 64: Others: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 65: Europe: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 66: Europe: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 67: Germany: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 68: Germany: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 69: France: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 70: France: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 71: United Kingdom: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 72: United Kingdom: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 73: Italy: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 74: Italy: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 75: Spain: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 76: Spain: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 77: Russia: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 78: Russia: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 79: Others: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 80: Others: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 81: Latin America: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 82: Latin America: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 83: Brazil: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 84: Brazil: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 85: Mexico: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 86: Mexico: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 87: Others: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 88: Others: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 89: Middle East and Africa: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 90: Middle East and Africa: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 91: Turkey: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 92: Turkey: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 93: Saudi Arabia: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 94: Saudi Arabia: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 95: Others: Data Center Construction Market: Sales Value (in Million USD), 2020 & 2025

Figure 96: Others: Data Center Construction Market Forecast: Sales Value (in Million USD), 2026-2034

Figure 97: Global: Data Center Construction Industry: SWOT Analysis

Figure 98: Global: Data Center Construction Industry: Value Chain Analysis

Figure 99: Global: Data Center Construction Industry: Porter’s Five Forces Analysis