Semiconductor Applications In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

ヘルスケアにおける半導体アプリケーションは、アプリケーション (医療用画像、民生用医療用電子機器、医療機器など)、コンポーネント (集積回路、オプトエレクトロニクス、センサーなど)、テクノロジーノード (28 Nm 未満、28~65 Nm、65 Nm 以上)、および地域 (北米、南米、ヨーロッパ、アジア太平洋など) 別にセグメント化されています。

The Semiconductor Applications in Healthcare Market Report is Segmented by Application (Medical Imaging, Consumer Medical Electronics, Medical Instruments, and More), Component (Integrated Circuits, Optoelectronics, Sensors, and More), Technology Node (Less Than 28 Nm, 28–65 Nm, Above 65 Nm), and Geography (North America, South America, Europe, Asia-Pacific, and More).

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 127 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-1423914239 |

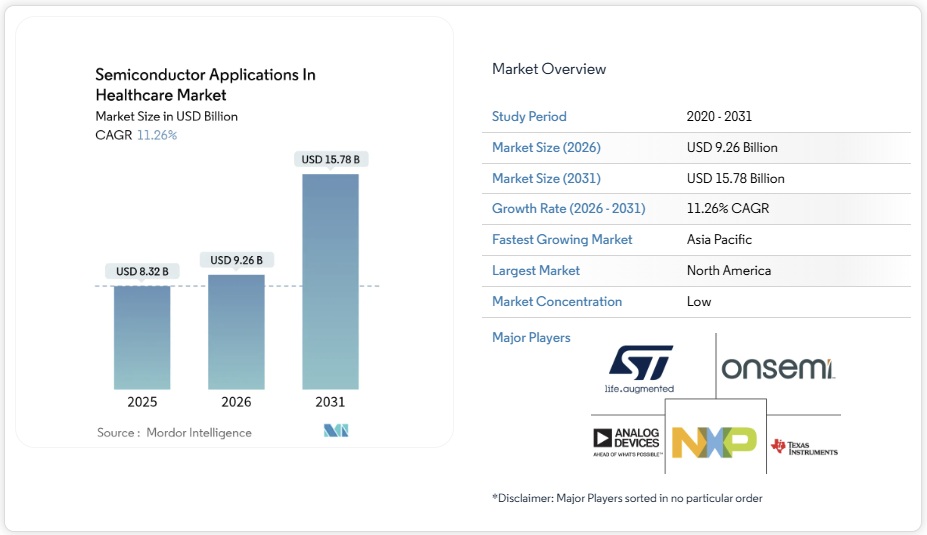

ヘルスケアにおける半導体アプリケーションの市場規模は、2026年には92億6,000万米ドルに達すると推定されています。これは、2025年の83億2,000万米ドルから増加し、2031年には157億8,000万米ドルに達すると予測されており、2026年から2031年にかけて年平均成長率(CAGR)11.26%で成長します。急速な成長は、人工知能(AI)イメージング、埋め込み型バイオMEMS、ラボオンチップ診断など、中央集中型の検査室から検査を移行する病院への投資に起因しています。この成長は、超低消費電力のシステムオンチップ(SoC)とセキュアエレメントデバイスがネットワークエッジで患者データを取得、処理、保護するコネクテッドケアへの決定的な推進を反映しています。高度なパッケージング、生体適合性材料、長期ライフサイクルの製品サポートを組み合わせることができるチップメーカーは、臨床医が長年にわたって確実に動作する認定ハードウェアを求める中、汎用ベンダーを凌駕する立場にあります。最後に、国家半導体インセンティブ プログラムにより、供給基盤が再編され、医療用に検証されたシリコンのリード タイムが短縮され、単一地域の生産拠点への依存が減少しています。

セグメント分析

- 医用画像処理は2025年の売上高の35.22%を占め、ヘルスケアにおける半導体アプリケーション市場の中核的な価値創造者としての役割を明確に示した。この分野では、CT(コンピューター断層撮影)、MRI(磁気共鳴画像)、超音波診断コンソールに、高解像度デジタイザ、フィールドプログラマブルゲートアレイ、AIアクセラレータを組み合わせたマルチダイモジュールが組み込まれている。スペクトルCTや光子計数CTへの移行に伴い処理需要が高まり、OEM各社は4GB/秒を超えるデータレートに対応するHBM対応SoCの採用を迫られている。一方、ハンドヘルド超音波診断システムは、シングルチップ統合技術を活用し、救急現場でのポイントオブケア診断を実現している。予測モデルによると、医療市場における半導体アプリケーションにおいて、医用画像処理は2031年までに12.06%のCAGRを維持すると予測されている。

- 補完的な成長は、消費者向け医療用電子機器から生まれています。インターネット接続型の血圧計、血糖値モニター、心電図パッチには、セキュアな無線機能と省電力マイクロコントローラーが統合されています。病院がネットワーク化されたバイタルサインハブを標準化し、そこから電子カルテにデータをストリーミングするようになったため、診断用患者モニタリング機器や治療機器も着実に成長しています。医療機器は依然として安定しているものの、それほど大きな変動はなく、精度と長寿命のために実績のある65nm以降のアナログノードが優位となるラボオートメーション分野に集中しています。

- ヘルスケアにおける半導体アプリケーション市場レポートは、アプリケーション(医療用画像、民生用医療電子機器、医療機器など)、コンポーネント(集積回路、オプトエレクトロニクス、センサーなど)、技術ノード(28Nm未満、28~65Nm、65Nm超)、地域(北米、南米、欧州、アジア太平洋地域など)別にセグメント化されています。市場予測は金額(米ドル)で提供されます。

Semiconductor Applications In Healthcare Market Analysis

The semiconductor applications in the healthcare market size in 2026 is estimated at USD 9.26 billion, growing from 2025 value of USD 8.32 billion with 2031 projections showing USD 15.78 billion, growing at 11.26% CAGR over 2026-2031. Rapid gains stem from hospital investments in artificial-intelligence imaging, implantable bio-MEMS, and lab-on-chip diagnostics that shift testing away from centralized laboratories. Growth also reflects a decisive push toward connected care, where ultra-low-power system-on-chips (SoCs) and secure element devices capture, process, and protect patient data at the network edge. Chipmakers able to combine advanced packaging, biocompatible materials, and long-lifecycle product support are positioned to outpace general-purpose vendors as clinicians demand certified hardware that runs reliably for years. Finally, national semiconductor incentive programs are reshaping the supply base, shortening lead times for medically validated silicon and reducing dependence on single-region production hubs.

Global Semiconductor Applications In Healthcare Market Trends and Insights

Proliferation of Connected Medical Devices and IoT

Global hospital and home-care ecosystems now deploy smart monitors, infusion pumps, and ambient-assisted living tools that continuously log vital signs. These systems rely on wireless SoCs that merge Bluetooth LE, Wi-Fi 6, or 5G radios with sensor interfaces and encrypted storage while consuming microwatts during sleep cycles. Long-life coin-cell operation reinforces demand for energy-harvesting PMICs, prompting suppliers to co-optimize radio stacks and power domains. Device fleets also incorporate hardware root-of-trust modules, allowing clinicians to authenticate firmware updates. As reimbursement frameworks shift toward outcome-based models, providers are increasingly favoring edge-processed data that reduces latency and network congestion, thereby expanding the addressable silicon content per device.

Growing Adoption of AI-Enabled Imaging Systems

Radiology suites are transitioning from retrospective image reads to real-time decision support delivered on-console. Photon-counting CT scanners offer higher spectral resolution, thereby increasing the raw data volume and necessitating on-board accelerator arrays capable of executing image reconstruction and deep-learning algorithms in milliseconds. Semiconductor designers address this by pairing high-bandwidth HBM stacks with low-geometry logic dies within 2.5-D interposers, thereby boosting throughput while maintaining compact footprints. In parallel, compound-semiconductor detectors using gallium arsenide or perovskite materials deliver sharper contrast at lower radiation doses, creating back-end demand for specialized analog front-ends and high-voltage drivers.

High Upgrade Costs for Legacy Medical Equipment

Many hospitals continue operating MRI scanners, bedside monitors, and infusion pumps purchased a decade ago, leaving limited capital for semiconductor-intensive upgrades. Original equipment manufacturers (OEMs), therefore, face pressure to release drop-in boards rather than entirely new systems, which slows the penetration of next-generation AI processors. Funding gaps are most acute in small private clinics and emerging economies, where reimbursements lag and procurement cycles extend well beyond Western averages. To counter the barrier, suppliers bundle financing packages and usage-based service models that amortize silicon costs over multi-year maintenance contracts.

Other drivers and restraints analyzed in the detailed report include:

- Rising Chronic-Disease Burden Driving Remote Monitoring

- Government Incentives for Healthcare-Specific Fabs

- Stringent Regulatory Approval Cycles for Chip Changes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical imaging contributed 35.22% of 2025 revenue, underscoring its role as the core value generator for the semiconductor applications in the healthcare market. Within this arena, computed tomography, magnetic resonance imaging, and ultrasound consoles incorporate multi-die modules that combine high-resolution digitizers, field-programmable gate arrays, and AI accelerators. The migration toward spectral and photon-counting CT elevates processing demand, prompting OEMs to specify HBM-enabled SoCs that manage data rates exceeding 4 GB/s. Meanwhile, handheld ultrasound systems leverage single-chip integration to deliver point-of-care diagnostics in emergency settings. Forecast models indicate medical imaging will sustain a 12.06% CAGR in the semiconductor applications in the healthcare market by 2031.

Complementary growth stems from consumer medical electronics, where connected blood-pressure cuffs, glucose monitors, and ECG patches integrate secure radios and power-efficient microcontrollers. Diagnostic patient monitoring and therapy equipment also expand steadily as hospitals standardize on networked vital-sign hubs that stream data into electronic health records. Medical instruments remain a stable but less dynamic category, concentrating on laboratory automation that favors tried-and-tested 65 nm and above analog nodes for precision and longevity.

The Semiconductor Applications in Healthcare Market Report is Segmented by Application (Medical Imaging, Consumer Medical Electronics, Medical Instruments, and More), Component (Integrated Circuits, Optoelectronics, Sensors, and More), Technology Node (Less Than 28 Nm, 28–65 Nm, Above 65 Nm), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains its leadership position, with 32.74% revenue in 2025, driven by a mature healthcare payer ecosystem that can reimburse premium diagnostics. Federal incentives have accelerated domestic analog and mixed-signal wafer starts, reducing lead times for FDA-cleared components. Academic-medical partnerships centered in California, Massachusetts, and Texas sustain a continuous pipeline of neuromodulation and implantable sensor prototypes that transition swiftly into clinical trials. However, export-control considerations on certain high-bandwidth AI accelerators introduce planning complexity for multinational OEMs shipping imaging consoles worldwide.

The Asia-Pacific region posts the fastest trajectory at a 13.08% CAGR, fueled by large-scale public investments in hospital infrastructure across China, India, and Southeast Asia. Shenzhen-based fabs specializing in medical-grade ASIC production now offer turnkey ISO 13485 assembly services, shortening design cycles for regional device startups. In India, government digital-health campaigns are spurring demand for cost-optimized SoCs that integrate Bluetooth LE and power-efficient RISC-V cores, enabling vital-sign collection in rural clinics. Japanese manufacturers emphasize precision and materials innovation; recent transitions to 8-inch SiC wafers support high-voltage supplies inside MRI gradient amplifiers.

Europe maintains a strong regulatory voice through its Medical Device Regulation, which shapes the requirements for component traceability and post-market surveillance. The EU Chips Act earmarks grants for packaging plants that adopt solvent-free die-attach chemistries to comply with impending PFAS restrictions. Pan-European purchasing consortiums increasingly weigh suppliers’ renewable-energy footprints, encouraging chipmakers to document carbon-reduction roadmaps. While overall growth trails that of the Asia-Pacific region, Europe’s emphasis on sustainability and data-protection compliance ensures consistent high-value orders for secure processing and encryption silicon.

List of Companies Covered in this Report:

- Analog Devices Inc.

- ams Osram AG

- Broadcom Inc.

- Dialog Semiconductor Ltd.

- Infineon Technologies AG

- Mediatek Inc.

- Microchip Technology Inc.

- Micron Technology Inc.

- Nordic Semiconductor ASA

- NXP Semiconductors N.V.

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Rohm Semiconductor

- Samsung Electronics Co. Ltd.

- Sensirion AG

- Skyworks Solutions Inc.

- STMicroelectronics N.V.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Zilog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

4.1 Market Overview

4.2 Market Drivers

4.2.1 Proliferation of connected medical devices and IoT

4.2.2 Growing adoption of AI-enabled imaging systems

4.2.3 Rising chronic-disease burden driving remote monitoring

4.2.4 Government incentives for healthcare-specific fabs

4.2.5 Implantable bio-MEMS with on-chip power

4.2.6 Lab-on-chip diagnostics reducing central-lab dependence

4.3 Market Restraints

4.3.1 High upgrade costs for legacy medical equipment

4.3.2 Stringent regulatory approval cycles for chip changes

4.3.3 Thermal issues in miniaturised wearable/implantables

4.3.4 Supply-chain concentration in specialist substrates

4.4 Industry Value Chain Analysis

4.5 Regulatory Landscape

4.6 Technological Outlook

4.7 Porter’s Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Buyers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes

4.7.5 Intensity of Competitive Rivalry

4.8 Assessment of Impact of Key Macro Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

5.1 By Application

5.1.1 Medical Imaging

5.1.2 Consumer Medical Electronics

5.1.3 Diagnostic Patient Monitoring and Therapy

5.1.4 Medical Instruments

5.2 By Component

5.2.1 Integrated Circuits

5.2.1.1 Analog

5.2.1.2 Logic

5.2.1.3 Memory

5.2.1.4 Micro-components

5.2.2 Optoelectronics

5.2.3 Sensors

5.2.4 Discrete Components

5.2.5 Research Institutes

5.3 By Technology Node

5.3.1 Less than 28 nm

5.3.2 28–65 nm

5.3.3 Above 65 nm

5.4 By Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Mexico

5.4.2 South America

5.4.2.1 Brazil

5.4.2.2 Argentina

5.4.2.3 Rest of South America

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 Russia

5.4.3.7 Rest of Europe

5.4.4 Asia-Pacific

5.4.4.1 China

5.4.4.2 Japan

5.4.4.3 India

5.4.4.4 South Korea

5.4.4.5 South-East Asia

5.4.4.6 Rest of Asia-Pacific

5.4.5 Middle East

5.4.6 Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

6.4.1 Analog Devices Inc.

6.4.2 ams Osram AG

6.4.3 Broadcom Inc.

6.4.4 Dialog Semiconductor Ltd.

6.4.5 Infineon Technologies AG

6.4.6 Mediatek Inc.

6.4.7 Microchip Technology Inc.

6.4.8 Micron Technology Inc.

6.4.9 Nordic Semiconductor ASA

6.4.10 NXP Semiconductors N.V.

6.4.11 ON Semiconductor Corp.

6.4.12 Qualcomm Inc.

6.4.13 Renesas Electronics Corp.

6.4.14 Rohm Semiconductor

6.4.15 Samsung Electronics Co. Ltd.

6.4.16 Sensirion AG

6.4.17 Skyworks Solutions Inc.

6.4.18 STMicroelectronics N.V.

6.4.19 Taiwan Semiconductor Manufacturing Co. Ltd.

6.4.20 Texas Instruments Inc.

6.4.21 Toshiba Electronic Devices & Storage Corp.

6.4.22 Vishay Intertechnology Inc.

6.4.23 Zilog Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

7.1 White-space and Unmet-Need Assessment