Tantalum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

タンタル市場レポートは、製品 (金属、炭化物、粉末、合金、その他の形態)、純度 (純度 99.95% 未満および 99.95% 超)、用途 (コンデンサー、半導体、エンジン タービン ブレード、化学処理装置など)、および地域 (アジア太平洋、北米、ヨーロッパ、南米、中東およびアフリカ) 別にセグメント化されています。

The Tantalum Market Report is Segmented by Product (Metal, Carbide, Powder, Alloys, Other Forms), Purity (Less Than 99. 95% Purity and More Than 99. 95% Purity), Application (Capacitors, Semiconductors, Engine Turbine Blades, Chemical Processing Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

| 出版 | Mordor Intelligence |

| 出版年月 | 2026年02月 |

| ページ数 | 120 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-1408614086 |

タンタル市場は、2025年の3キロトンから2026年には3.15キロトンに成長し、2031年には4.02キロトンに達すると予測されています。この成長軌道は、耐食性、生体適合性、そして高い誘電強度という比類のない組み合わせを持つタンタルの特性を反映しており、コンデンサ、スパッタリングターゲット、超合金、そしてインプラント型医療機器など、幅広い用途で需要の底堅さを維持しています。電子機器の小型化の進展、5G導入の加速、そして航空宇宙エンジンの安定した生産ペースは、依然として需要喚起の主要な要因となっています。同時に、紛争鉱物規制への対応とスポット価格の変動に対する懸念が続く中、オーストラリアとジンバブエのリチウムペグマタイト鉱山からの共同生産は、構造的な供給リスクを軽減しています。航空宇宙および医療技術の OEM は、市場の不透明な取引環境にもかかわらず、調達を安定させる長期契約をサポートしながら、価格よりも供給の安定性を優先し続けています。

セグメント分析

- 粉末は、コンデンサの陽極およびスパッタリングターゲットの消費急増に牽引され、2025年にはタンタル市場の36.10%を占めました。このサブセグメントは、小型化により粒度分布の狭さと比静電容量の向上が求められることから、2031年まで年平均成長率5.43%で成長すると予測されています。金属ビレット、ワイヤー、シートは粉末に次ぐシェアですが、鍛造形状が必須となる化学処理装置や航空宇宙の高温部部品には依然として不可欠です。超硬合金は、2,000HVを超える硬度を重視する切削工具や耐摩耗鋼板メーカーに供給され、合金添加物はジェットエンジン用超合金の基盤となっています。

- 積層造形への移行は、並行成長の道を開きつつあります。レーザー粉末床溶融結合法(LPF)向けに最適化された球状粉末は、医療用インプラントにおいて複雑な格子形状を可能にします。主要な粉末サプライヤーは、酸素含有量200ppm未満でD50値が3µm付近となるよう、微粒化ラインを拡張しています。これは、整形外科用ケージや頭蓋顔面メッシュの仕様に最適な範囲です。厳格なフォームファクター管理により、予測期間中、粉末はタンタル市場の中心であり続けるでしょう。

- タンタル市場レポートは、製品(金属、炭化物、粉末、合金、その他)、純度(純度99.95%未満および99.95%超)、用途(コンデンサ、半導体、エンジンタービンブレード、化学処理装置など)、および地域(アジア太平洋、北米、欧州、南米、中東およびアフリカ)別にセグメント化されています。市場予測は数量(トン)で提供されます。

Tantalum Market Analysis

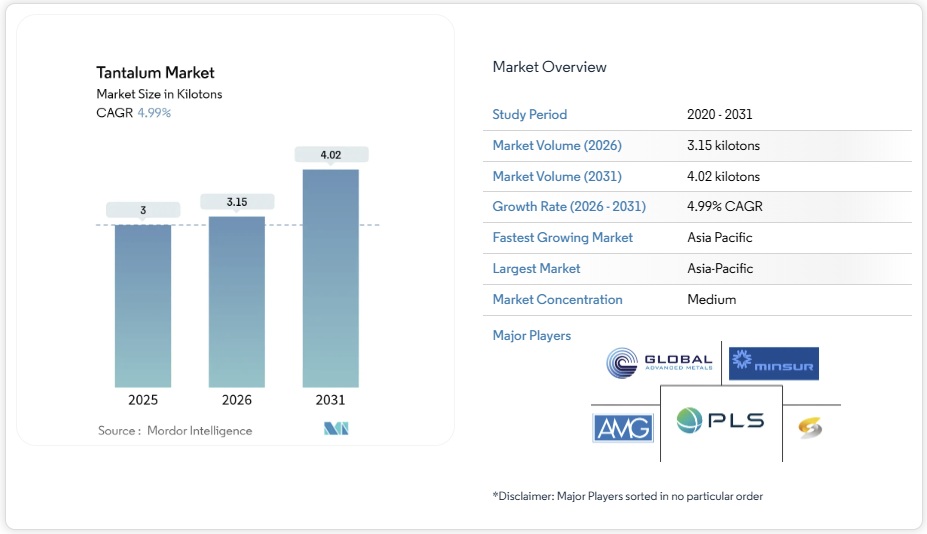

The Tantalum market is expected to grow from 3 kilotons in 2025 to 3.15 kilotons in 2026 and is forecast to reach 4.02 kilotons by 2031 at 4.99% CAGR over 2026-2031. This growth trajectory reflects the metal’s unmatched combination of corrosion resistance, biocompatibility, and high dielectric strength that keeps demand resilient across capacitors, sputtering targets, super-alloys, and implantable medical devices. Robust electronics miniaturization, accelerating 5G deployment, and steady aerospace engine build rates remain primary demand catalysts. Parallelly, co-production from lithium pegmatite mines in Australia and Zimbabwe is easing structural supply risk even as concerns over conflict-mineral compliance and spot-price volatility persist. OEMs in aerospace and medical technology continue to prioritize security of supply over price, supporting long-term contracts that stabilize procurement despite the market’s opaque trading environment.

Global Tantalum Market Trends and Insights

Surging Demand for Miniaturised Tantalum Capacitors in 5G-Enabled Devices

5G infrastructure densification and handset upgrades are accelerating procurement of solid tantalum chip capacitors that can maintain capacitance stability under high-frequency switching. Component makers report that tantalum capacitors provide superior volumetric efficiency and lower equivalent series resistance than multi-layer ceramic types, features critical for space-constrained power-management circuits in flagship smartphones and small-cell base stations. Reliability across –55 °C to +175 °C temperature excursions makes tantalum devices the preferred choice for telecommunications OEMs keen to avoid field failures. Packaging road-maps now target case sizes as low as 0201, a node where powder-engineered anodes deliver high CV (capacitance–voltage) ratios without sacrificing mechanical integrity. The tantalum market benefits directly as device miniaturization lifts grams-per-unit usage despite broader material-lightweighting trends.

Demand for Tantalum Sputtering Targets in Advanced Semiconductor Nodes

Sub-7 nm logic and DRAM production flow-sheets specify tantalum and tantalum nitride diffusion-barrier layers that prevent copper migration while preserving low line resistance. Extreme ultraviolet lithography raises purity thresholds to 99.999%+, narrowing the supplier base to refiners with ultra-high-vacuum metallurgy capabilities. Long-term offtake agreements signed by leading Asian foundries in 2025 underscore how strategic this precursor has become in maintaining wafer yield. Equipment upgrades in South Korea, Taiwan, and mainland China are therefore translating into steady volumes for high-purity powder producers. Supply tightness remains a possibility whenever geopolitical disruptions affect concentrate flows from Central Africa, reinforcing the tantalum market’s tendency to price security at a premium.

Conflict-Mineral Compliance Costs and Supply Disruptions

Stringent due-diligence mandates under U.S. and EU regulations oblige downstream manufacturers to trace concentrate back to conflict-free smelters, adding audit and certification fees that lift finished-component costs by as much as one-quarter. Artisanal production from Central Africa still provides a significant share of global supply, and periodic border closures or security incidents can interrupt flows with little notice. As a result, capacitor and super-alloy suppliers hold larger safety stocks and favor multi-year take-or-pay contracts that lock in volumes even if spot prices ease.

Other drivers and restraints analyzed in the detailed report include:

- Rising Production of Super-Alloy Jet-Engine Components

- Co-Production with Lithium Hard-Rock Mines Enhancing Supply Security

- Niobium Capacitors Replacing Tantalum in ADAS Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder accounted for 36.10% of the tantalum market share in 2025, propelled by surging capacitor anode and sputtering-target consumption. This sub-segment is forecast to post a 5.43% CAGR through 2031 as miniaturization pushes demand for tighter particle-size distributions and higher specific capacitance. Metal billet, wire, and sheet collectively trail powder but remain essential for chemical-processing equipment and aerospace hot-zone components where wrought form factors are mandatory. Carbide grades serve cutting-tool and wear-plate manufacturers who value hardness exceeding 2,000 HV, while alloy additions underpin jet-engine super-alloys.

The shift toward additive manufacturing is opening a parallel growth lane: spherical powder optimized for laser powder-bed fusion enables complex lattice geometries in medical implants. Key powder suppliers scale atomization lines to deliver D50 values near 3 µm with oxygen content below 200 ppm, a specification sweet spot for orthopedic cages and craniofacial meshes. Tight form-factor control will keep powder at the epicenter of the tantalum market during the forecast horizon.

The Tantalum Market Report is Segmented by Product (Metal, Carbide, Powder, Alloys, Other Forms), Purity (Less Than 99. 95% Purity and More Than 99. 95% Purity), Application (Capacitors, Semiconductors, Engine Turbine Blades, Chemical Processing Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific dominated with 46.50% of global consumption in 2025, and the region is forecast to post a 5.93% CAGR through 2031. China, Japan, and South Korea concentrate capacitor assembly lines, memory-chip fabs, and display-panel plants that absorb powder and sputtering targets. Taiwan’s logic-foundry expansion amplifies ultra-high-purity demand, while Korean memory producers leverage domestic research programs to trial tantalum-based MIM (metal-insulator-metal) capacitors in DDR6 modules. Australia’s rise as a co-product supplier strengthens regional supply security, reducing over-reliance on African concentrates and bolstering value-chain resilience.

North America remains a strategic end-use region anchored by aerospace, defense, and medical device verticals. Although primary mine output is limited to Canada’s Tanco operation, a robust secondary recovery network processes super-alloy scrap and electronic waste, feeding powder and alloy circuits. U.S. procurement policies that prioritize conflict-free sourcing sustain price premiums yet secure volume for jet-engine OEMs and cardiac-rhythm-management manufacturers.

Europe exhibits a mature yet stable demand curve, characterized by high engineering standards and stringent environmental regulations. Germany’s Tier-1 automotive suppliers drive capacitor off-take for advanced driver-assistance modules, while French nuclear-equipment firms specify tantalum linings for rad-waste systems. The European Union’s conflict-minerals directive tightens compliance budgets, but recycling mandates embedded in the circular economy framework gradually offset virgin-material needs. Eastern European capacitor plants offer cost-competitive assembly yet still adhere to region-wide traceability requirements.

List of Companies Covered in this Report:

- AMG

- Advanced MaterialsTM, LLC

- CNMC Ningxia Orient Group Co., Ltd

- Energy Transition Minerals Ltd

- F&X Electro-Materials Limited

- Global Advanced Metals Pty Ltd

- Inframat

- Jiujiang Nonferrous Metals Smelting Co., Ltd

- JX Advanced Metals Corporation

- Lorad Chemical Corporation

- Materion Corporation

- Minsur

- Mitsui Mining & Smelting Co., Ltd.

- MPIL

- Pilbara Minerals Limited

- SAJAN OVERSEAS

- Star Earth Minerals Pvt Ltd.

- Taki Chemical Co., Ltd

- Tantalex Lithium Resources

- Ulba Metallurgical Plant

- Ximei Resources Holding Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Table of Contents

1 Introduction

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

4.1 Market Overview

4.2 Market Drivers

4.2.1 Surging demand for miniaturised tantalum capacitors in 5G-enabled devices

4.2.2 Demand for tantalum sputtering targets in advanced semiconductor nodes

4.2.3 Rising production of super-alloy jet-engine components

4.2.4 Co-production with lithium hard-rock mines enhancing supply security

4.2.5 Medical-grade tantalum coatings for neuro-implants

4.3 Market Restraints

4.3.1 Conflict-mineral compliance costs and supply disruptions

4.3.2 High spot-price volatility in an opaque trading market

4.3.3 Niobium capacitors replacing tantalum in ADAS systems

4.4 Value Chain Analysis

4.5 Regulatory Policy Analysis

4.6 Technological Snapshot

4.7 Porter’s Five Forces

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Buyers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes

4.7.5 Competitive Rivalry

4.8 Price Index

4.9 Import-Export Trends

5 Market Size and Growth Forecasts (Volume)

5.1 By Product

5.1.1 Metal

5.1.2 Carbide

5.1.3 Powder

5.1.4 Alloys

5.1.5 Other Forms

5.2 By Purity

5.2.1 Less than 99.95% Purity

5.2.2 More than 99.95% Purity

5.3 By Application

5.3.1 Capacitors

5.3.2 Semiconductors

5.3.3 Engine Turbine Blades

5.3.4 Chemical Processing Equipment

5.3.5 Medical Equipment

5.3.6 Other Applications

5.4 By Geography

5.4.1 Production Analysis

5.4.1.1 United States

5.4.1.2 Australia

5.4.1.3 Brazil

5.4.1.4 China

5.4.1.5 Congo

5.4.1.6 Ethiopia

5.4.1.7 Nigeria

5.4.1.8 Rwanda

5.4.1.9 Other Countries

5.4.2 Consumption Analysis

5.4.2.1 Asia-Pacific

5.4.2.1.1 China

5.4.2.1.2 India

5.4.2.1.3 Japan

5.4.2.1.4 South Korea

5.4.2.1.5 Rest of Asia-Pacific

5.4.2.2 North America

5.4.2.2.1 United States

5.4.2.2.2 Canada

5.4.2.2.3 Mexico

5.4.2.3 Europe

5.4.2.3.1 Germany

5.4.2.3.2 United Kingdom

5.4.2.3.3 Italy

5.4.2.3.4 France

5.4.2.3.5 Rest of Europe

5.4.2.4 South America

5.4.2.4.1 Brazil

5.4.2.4.2 Argentina

5.4.2.4.3 Rest of South America

5.4.2.5 Middle-East and Africa

5.4.2.5.1 Saudi Arabia

5.4.2.5.2 South Africa

5.4.2.5.3 Rest of Middle-East and Africa

6 Competitive Landscape

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share (%)/Ranking Analysis

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

6.4.1 AMG

6.4.2 Advanced MaterialsTM, LLC

6.4.3 CNMC Ningxia Orient Group Co., Ltd

6.4.4 Energy Transition Minerals Ltd

6.4.5 F&X Electro-Materials Limited

6.4.6 Global Advanced Metals Pty Ltd

6.4.7 Inframat

6.4.8 Jiujiang Nonferrous Metals Smelting Co., Ltd

6.4.9 JX Advanced Metals Corporation

6.4.10 Lorad Chemical Corporation

6.4.11 Materion Corporation

6.4.12 Minsur

6.4.13 Mitsui Mining & Smelting Co., Ltd.

6.4.14 MPIL

6.4.15 Pilbara Minerals Limited

6.4.16 SAJAN OVERSEAS

6.4.17 Star Earth Minerals Pvt Ltd.

6.4.18 Taki Chemical Co., Ltd

6.4.19 Tantalex Lithium Resources

6.4.20 Ulba Metallurgical Plant

6.4.21 Ximei Resources Holding Limited

7 Market Opportunities and Future Outlook

7.1 White-space and Unmet-Need Assessment