Digital Signage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Digital Signage Market Report is Segmented by Type (Video Wall, Video Screen, Kiosk, and More), Component (Hardware, Software, and Services), Deployment (On-Premise, Cloud-Based, and Hybrid), Screen Size (Below 32", 32"-52", and More), Location (In-store/Indoor, and Outdoor), End-Use Industry (Retail, Transportation, Hospitality, Corporate, and More), and Geography.

デジタルサイネージ市場レポートは、タイプ (ビデオウォール、ビデオスクリーン、キオスクなど)、コンポーネント (ハードウェア、ソフトウェア、サービス)、展開 (オンプレミス、クラウドベース、ハイブリッド)、画面サイズ (32 インチ未満、32 インチ~ 52 インチなど)、場所 (店内/屋内、屋外)、最終用途産業 (小売、輸送、接客業、企業など)、および地域別にセグメント化されています。

| 出版 | Mordor Intelligence |

| 出版年月 | 2025年07月 |

| ページ数 | 120 |

| 価格 | 記載以外のライセンスについてはお問合せください |

| シングルユーザ | USD 4,750 |

| 種別 | 英文調査報告書 |

| 商品番号 | SMR-1233512335 |

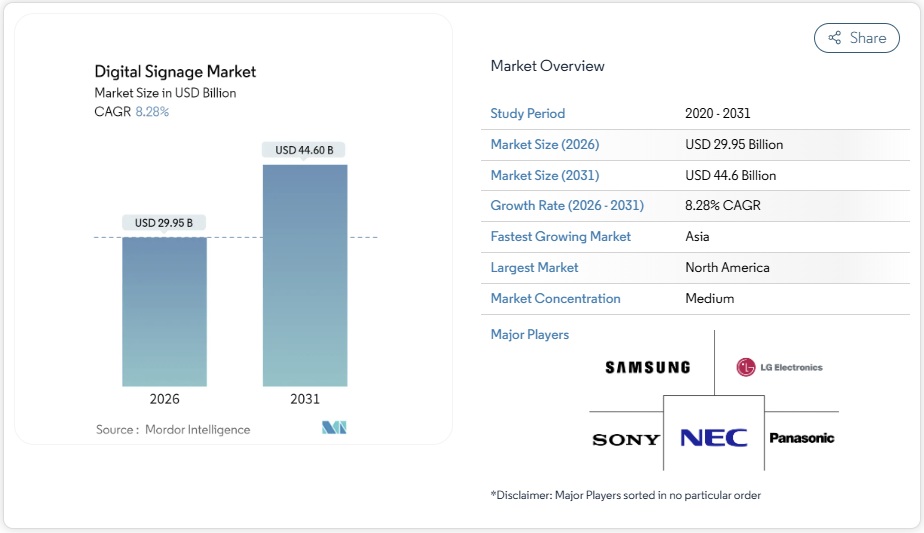

デジタルサイネージ市場規模は2025年に276億6,000万米ドルに達し、2030年には413億9,000万米ドルに達し、年平均成長率(CAGR)8.39%で成長すると予測されています。AI駆動型コンテンツエンジン、5G対応エッジネットワーク、省電力のマイクロLEDスクリーンの着実な普及が、この市場拡大を支えています。大企業は、ハイブリッドワークプレイス全体のコミュニケーションを統合するためにコネクテッドディスプレイを活用しており、市当局はスマートシティインフラにインタラクティブボードを組み込み、モビリティと公共安全の取り組みを効率化しています。小売業者は、オーディエンス分析プラットフォームが店内スクリーンを収益を生み出すリテールメディア資産へと変革するにつれ、投資を強化しています。同時に、交通機関はサービス品質を向上させるリアルタイムの旅客情報システムを導入しています。

セグメント分析

- ビデオウォールは、コントロールルームや旗艦店の店舗における没入感あふれる演出により、2024年の収益シェアの28.1%を占め、市場を牽引しました。デジタルサイネージ市場は、ブランドシアターや企業のタウンホールイベントにおいて、その規模の大きさが引き続き支持されています。また、フランチャイズ店がシンプルなコンテンツ交換を重視しているため、クイックサービスレストランのデジタルポスターの需要も堅調に推移しています。

- しかし、キオスクは、消費者がセルフチェックアウト、道案内、そしてレスポンシブタッチスクリーンでのロイヤルティ登録を利用するようになり、2030年までのCAGRが9.2%と最も高い成長が見込まれます。デジタルサイネージ市場の小売業者は、レジ時に追加オプションを推奨し、チケットのサイズを微調整するAIモジュールを導入しています。透明LCD筐体は、高級店や自動車ショールームでニッチな市場を開拓し、商品の視認性とデータオーバーレイを融合させています。メーカーは現在、交通機関のコンコース向けに、マルチパネルビデオウォールとキオスクのインタラクションを融合させたハイブリッドリグの実験を進めています。

- ハードウェア部品は2024年の売上高の60.7%を占め、LEDタイル、メディアプレーヤー、マウントキットなど、デジタルサイネージ市場の基盤であり続けています。ピクセルコストの低下により、4~5年ごとの更新サイクルにおける設備投資は管理可能な範囲にとどまっています。

- ソフトウェア収益は、コンテンツオーケストレーションと分析がROIの向上に繋がることに企業が気づき、年平均成長率(CAGR)10.5%の二桁成長を遂げています。クラウドダッシュボードはリモート診断を通じてフリートの稼働率を確保し、AIスケジューラーはキャンペーンの関連性を高めます。ベンダーはProof-of-Play台帳を統合することで、広告主が露出を監査できるようにし、デジタルサイネージ市場への信頼を高めています。

- デジタルサイネージ市場レポートは、タイプ(ビデオウォール、ビデオスクリーン、キオスクなど)、コンポーネント(ハードウェア、ソフトウェア、サービス)、導入形態(オンプレミス、クラウドベース、ハイブリッド)、画面サイズ(32インチ未満、32インチ~52インチなど)、設置場所(店舗内/屋内、屋外)、最終用途産業(小売、運輸、ホテル、企業など)、および地域別にセグメント化されています。市場予測は金額(米ドル)で提供されます。

Digital Signage Market Analysis

The digital signage market size stands at USD 27.66 billion in 2025 and is forecast to reach USD 41.39 billion by 2030, reflecting an 8.39% CAGR. Consistent uptake of AI-driven content engines, 5G-enabled edge networks and energy-frugal MicroLED screens underpins this expansion. Large enterprises are using connected displays to unify communications across hybrid workplaces, while city authorities weave interactive boards into smart-city infrastructure to streamline mobility and public safety initiatives. Retailers intensify investment as audience-analytics platforms transform in-store screens into revenue-generating retail-media assets. At the same time, transportation operators deploy real-time passenger information systems that raise service quality.

Global Digital Signage Market Trends and Insights

AI-powered audience analytics boosting dynamic content personalisation

Retailers now replace one-size-fits-all loops with AI engines that adjust messaging in real time when shoppers approach. Computer-vision modules gauge age bracket, gender and engagement length, then trigger creative variants that can lift conversion by as much as 30%. Chains in the United States, United Kingdom, Germany and France link these insights with loyalty-app data to enrich omnichannel campaigns. Agencies pay premium CPMs for such precise exposure, turning store networks into high-margin media channels. Compliance with GDPR shapes rollout pace in Europe, yet vendors embed privacy-by-design workflows that anonymise video frames locally before analysis. These factors keep the digital signage market on a solid medium-term growth path.

5G + edge computing enabling real-time outdoor streaming

Transit authorities in Tokyo, Seoul, Singapore and Sydney use millimetre-wave 5G backbones to push ultra-low-latency video and emergency alerts to outdoor LED boards. On-device edge servers pre-cache high-resolution clips, cutting data transit cost and letting campaigns switch instantly when foot-traffic sensors spike. Studies for Asian transport hubs show productivity gains from 52% to 245% and cost savings up to 90% when 5G replaces legacy fibre. As more metros activate standalone 5G cores, the digital signage market receives an immediate uplift.

Fragmented CMS standards complicating multi-vendor interoperability

Global retailers often juggle screens from several brands yet find no common protocol for scheduling or analytics. The International Telecommunication Union warns that the lack of interoperability slows deployments and raises total ownership cost. Many firms therefore lock into single-vendor ecosystems, limiting competitive bids. Industry alliances are drafting APIs, but diverging roadmaps among vendors keep progress slow. This reality curbs near-term scalability for the digital signage market.

Other drivers and restraints analyzed in the detailed report include:

- EU corporate sustainability mandates accelerating energy-efficient displays

- Post-pandemic hybrid work models driving cloud dashboards

- Cyber-security vulnerabilities spotlighted by ransomware on transit displays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video walls dominated 2024 revenue with 28.1% share due to their immersive impact in control rooms and flagship retail settings. The digital signage market continues to favour their scale for brand theatre and corporate town-hall events. Demand also stays steady for digital posters in quick-serve restaurants because franchisees value simple content swaps.

Kiosks, however, offer the fastest 9.2% CAGR to 2030 as shoppers embrace self-checkout, wayfinding and loyalty enrollment on responsive touchscreens. Retailers in the digital signage market deploy AI modules that recommend add-ons at check-out, nudging ticket size. Transparent LCD enclosures carve a niche in luxury stores and automotive showrooms, merging product visibility with data overlays. Manufacturers now experiment with hybrid rigs that fuse multi-panel video walls and kiosk interaction for transit concourses.

Hardware parts generated 60.7% of 2024 turnover and remain foundational to the digital signage market, covering LED tiles, media players and mounting kits. Falling pixel costs keep capex manageable for refresh cycles every four-to-five years.

Software revenue is growing at a double-digit 10.5% CAGR as companies discover that content orchestration and analytics drive ROI. Cloud dashboards secure fleet uptime through remote diagnostics, while AI schedulers improve campaign relevance. Vendors integrate proof-of-play ledgers so advertisers can audit exposures, raising confidence in the digital signage market.

The Digital Signage Market Report is Segmented by Type (Video Wall, Video Screen, Kiosk, and More), Component (Hardware, Software, and Services), Deployment (On-Premise, Cloud-Based, and Hybrid), Screen Size (Below 32″, 32″-52″, and More), Location (In-store/Indoor, and Outdoor), End-Use Industry (Retail, Transportation, Hospitality, Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 33.4% 2024 income, anchored by United States corporate refurbishments that turned lobbies into digital-first showcases. Canadian retailers accelerate checkout modernisation, keeping regional demand steady. The digital signage market here benefits from mature cloud infrastructure that reduces deployment friction.

Asia-Pacific is on an 8.5% CAGR trajectory, propelled by China’s city cluster projects, Japan’s technology export push, India’s mall boom and Southeast Asia’s tourism recovery. An integrated supply chain for panels and ICs lowers unit costs, giving regional buyers price latitude that boosts the digital signage market’s penetration.

Europe records stable gains supported by ecodesign mandates and high purchasing power. Historic-district signage caps add compliance effort, yet German and Nordic corporates adopt energy-class A displays, offsetting tourist-zone pauses. Eastern European airports compete for hub status through immersive wayfinding walls, expanding the digital signage market eastward.

List of Companies Covered in this Report:

- NEC Display Solutions Ltd.

- LG Display Co. Ltd.

- Samsung Electronics Co. Ltd.

- Panasonic Corporation

- Sony Group Corporation

- Stratacache

- Planar Systems Inc.

- Hitachi Ltd.

- Barco NV

- Goodview

- Cisco Systems Inc.

- Scala Inc.

- Broadsign International LLC

- Appspace Inc.

- BrightSign LLC

- Mvix Inc.

- Christie Digital Systems USA Inc.

- Daktronics Inc.

- Leyard Optoelectronic Co. Ltd.

- Unilumin Group Co. Ltd.

- JCDecaux SA

- E Ink Holdings Inc.

- Clear Channel Outdoor Holdings Inc.

- Sharp Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support